Will India's Textile Industry Weave Its Way to Global Dominance?

Growing up in a family deeply rooted in the textile business, I was always fascinated by how this industry operated. It was a symphony of processes, from spinning the common fiber into yarn, dying it into vivid colors, weaving it into fabric, and then turning it into finished clothing. It was more than just making clothes. Every stage was a different universe, full of possibilities and difficulties.

As a child, I would watch the rhythmic hum of machines in our family’s factory and marvel at the sheer scale of what we were a part of. Yet, what intrigued me the most was how vast and diverse the textile industry is. Every stage of this journey—whether spinning yarn or designing finished garments—represents a unique business opportunity. Over time, I realized that India, with its rich textile heritage and growing global footprint, is at the cusp of unparalleled growth in this sector.

The textile industry has long been a cornerstone of global commerce, weaving together a diverse array of raw materials, manufacturing processes, and consumer demands. In recent years, this industry has experienced significant transformation, driven by evolving consumer preferences, technological advancements, and global economic trends.

Globally, fiscal year 2024 began with serious worries about a number of issues, such as war, inflation, recession, supply chains, and labor markets; however, the year has had far less of an impact than anticipated. Most major economies saw a decrease in inflation, a largely averted recession, a significant reduction in supply chain disruption, and historically tight labor markets.

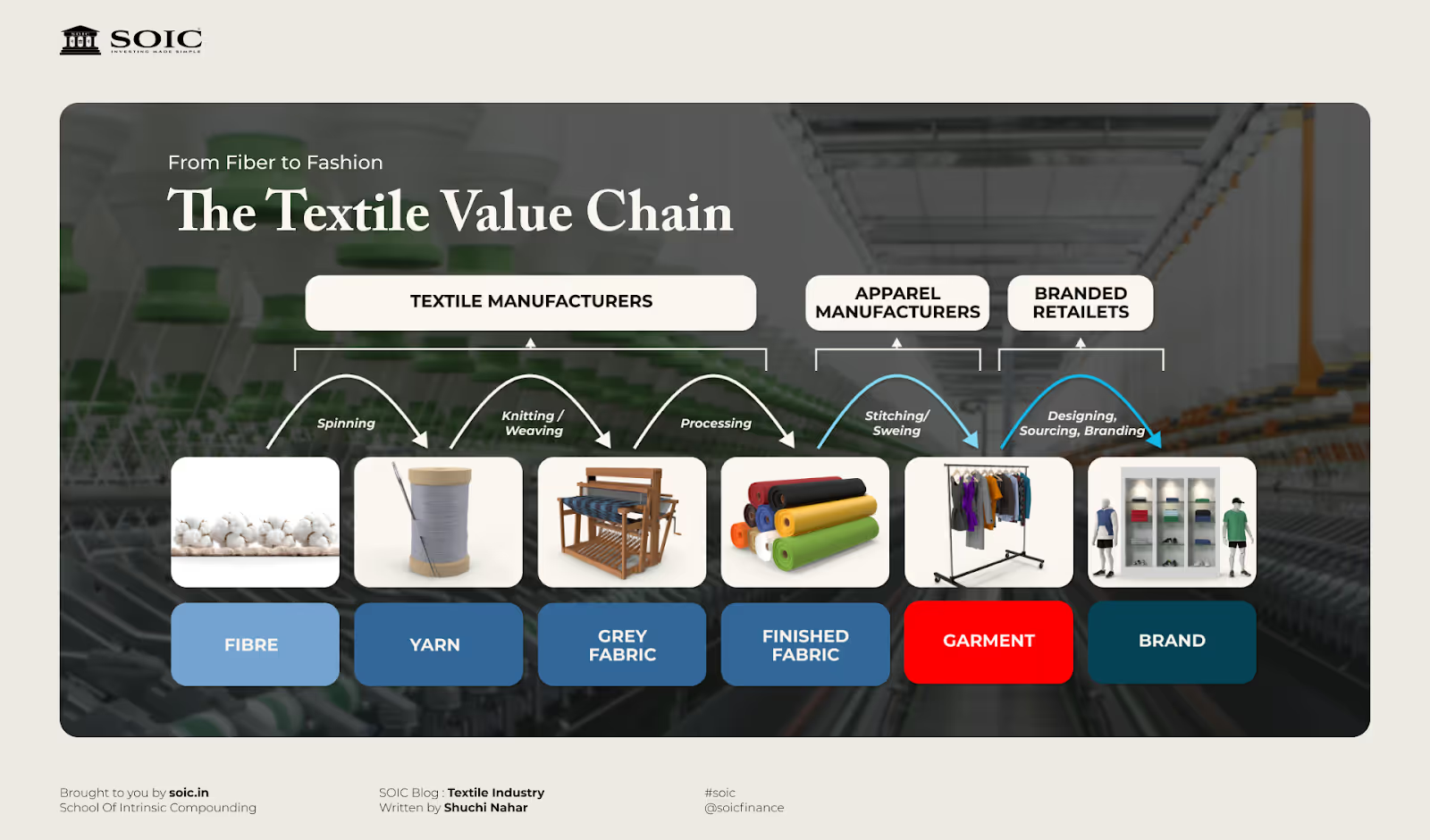

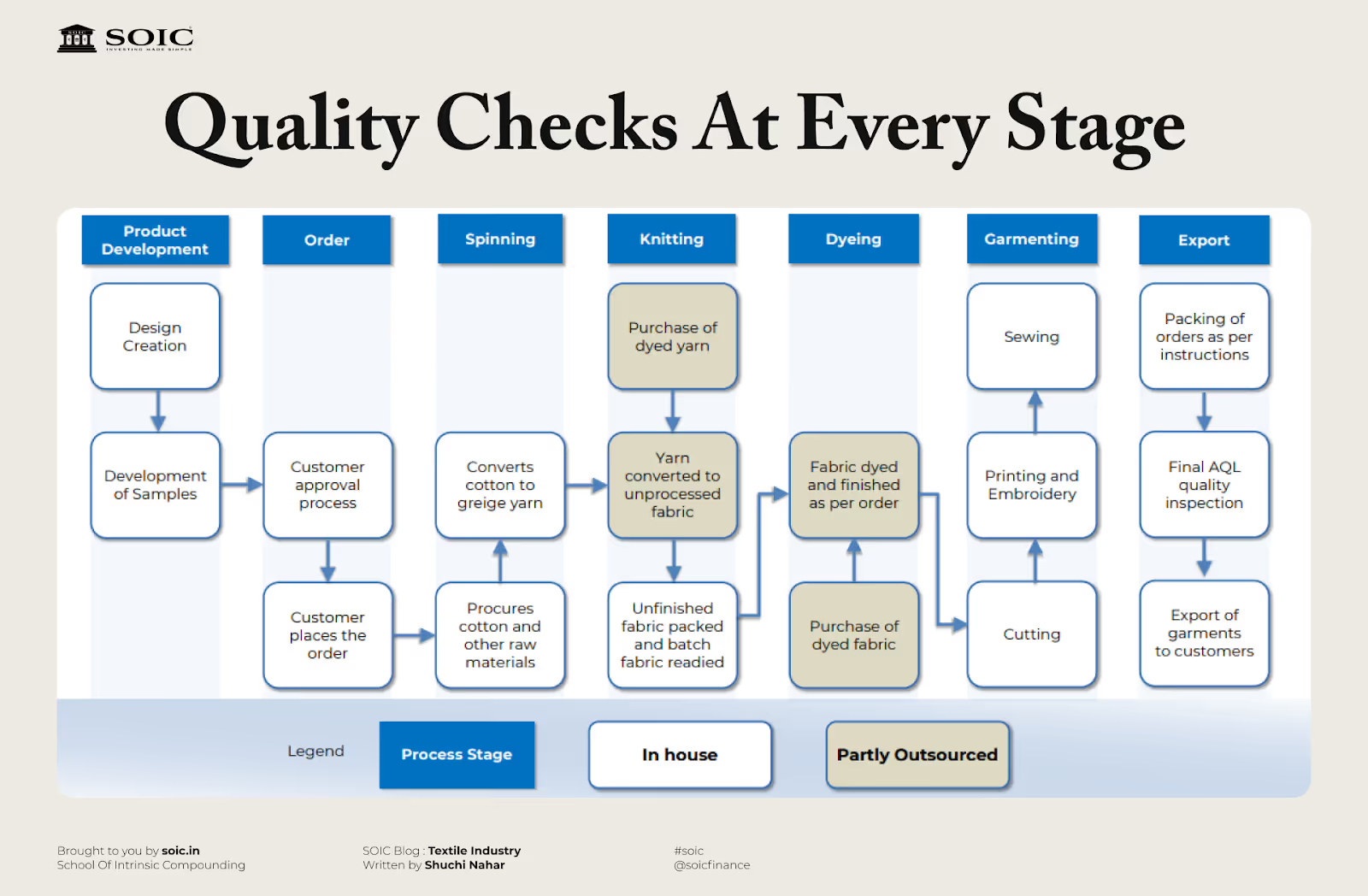

The textile industry comprises a comprehensive value chain that transforms raw fibers into finished products.

Major brands are shifting towards eco-friendly practices. Polyester, accounting for 53% of global fiber consumption, is being transformed into recyclable and sustainable variants, driven by commitments from brands like Nike and Adidas.

India’s “5Fs” strategy—Farmer, Fiber, Fabric, Fashion, and Foreign Markets—supports the textile ecosystem. Incentives like the PLI scheme and upcoming Free Trade Agreements (FTAs) with the UK and Europe aim to enhance global competitiveness.

The "Bangladesh+1" strategy is redirecting orders from politically unstable regions to India. However, India faces challenges like Bangladesh's preferential tariff advantages in EU markets.

Man-made fibers like polyester and viscose are outpacing natural fibers due to their sustainability and versatility.

Applications in automotive, healthcare, and defense are driving demand. Companies like Arvind Ltd are making significant strides in this segment.

India commands 52% of the US home textiles market, with companies like Welspun Living and Indo Count Industries scaling their capacities.

B2B platforms are enabling smaller players to access global markets, further democratizing the industry.

The industrial textiles market is likely to increase at an 8% CAGR from US$ 2 billion in 2020 to US$ 3.3 billion in 2027. The overall Indian textiles market is expected to be worth more than US$ 209 billion by 2029.

a. Growth Opportunity

India’s textile and apparel industry is expected to grow at 9% CAGR, reaching $350 billion by FY30, with exports clocking a 16% CAGR to $100 billion. The market for Indian textiles and apparel is projected to grow at a 10% CAGR to reach US$ 350 billion by 2030. Moreover, India is the world's 3rd largest exporter of Textiles and Apparel. India ranks among the top five global exporters in several textile categories, with exports expected to reach US$100 billion.

The textiles and apparel industry contributes 2.3% to the country’s GDP, 13% to industrial production and 12% to exports. The textile industry in India is predicted to double its contribution to the GDP, rising from 2.3% to approximately 5% by the end of this decade.

b. Focus Areas

c. Long-Term Vision

India’s shift towards MMF and value-added products (VAP) is pivotal. By leveraging technology, sustainability, and geopolitical shifts, the industry is poised for robust growth.

The global cotton yarn market is slated to post ~4% CAGR from USD 86.11bn in 2024 to USD 117.79 bn by 2032 (according to Fortune Business Insights). The demand for cotton yarn is expected to rise by 12-14% in volume terms in India.

Typically, India exports 25-35% of its cotton yarn production and consumes the remaining domestically. Even though India cultivates ~39% of the world's cotton area, with ~31.9mn hectares of land under cotton production, the country lags in yield and ranks 33rd globally, producing 441 kg/hectare of cotton.

This is far lower than the global average of 769 kg/hectare and lags leading producers such as China (1,950 kg/ha) and Brazil (1,845 kg/ha). China aces globally in cotton production at ~5.6mn tonnes, with India at a close ~5.5mn tonnes. Together, China and India are the world’s largest cotton consumers at ~7.8mn tonnes and ~5.39mn tonnes, respectively. India's cotton to non-cotton fiber mix stands at 60:40, compared with the rest of the world at 30:70; this highlights huge growth potential in the non-cotton fiber space.

The US and Brazil lead cotton exports at ~2.68mn tonnes and ~2.48mn tonnes, respectively. China and Bangladesh are the largest buyers of cotton at ~2.4mn tonnes and ~1.71mn tonnes, respectively.

The textile industry encompasses a broad range of players, each occupying distinct segments of the value chain. These companies operate in different capacities, focusing on specific parts of the production and distribution process. Let’s break down the types of players and analyze the economics of each segment.

These businesses operate at the very start of the value chain and are cyclical. The production of yarn spreads and cotton are the main activities. Global demand-supply dynamics and the cost of raw materials have a significant impact on this segment's operations.

Examples:

Textiles are sourced by this segment for major international brands. It is an asset-light model with high ROCE, making it a lucrative business.

Economics:

3. Companies Focused on Garmenting

Manufacturing clothing and accessories for international brands, businesses in this sector concentrate on the forward portion of the textile value chain. These companies serve both export and domestic markets, especially major international retailers.

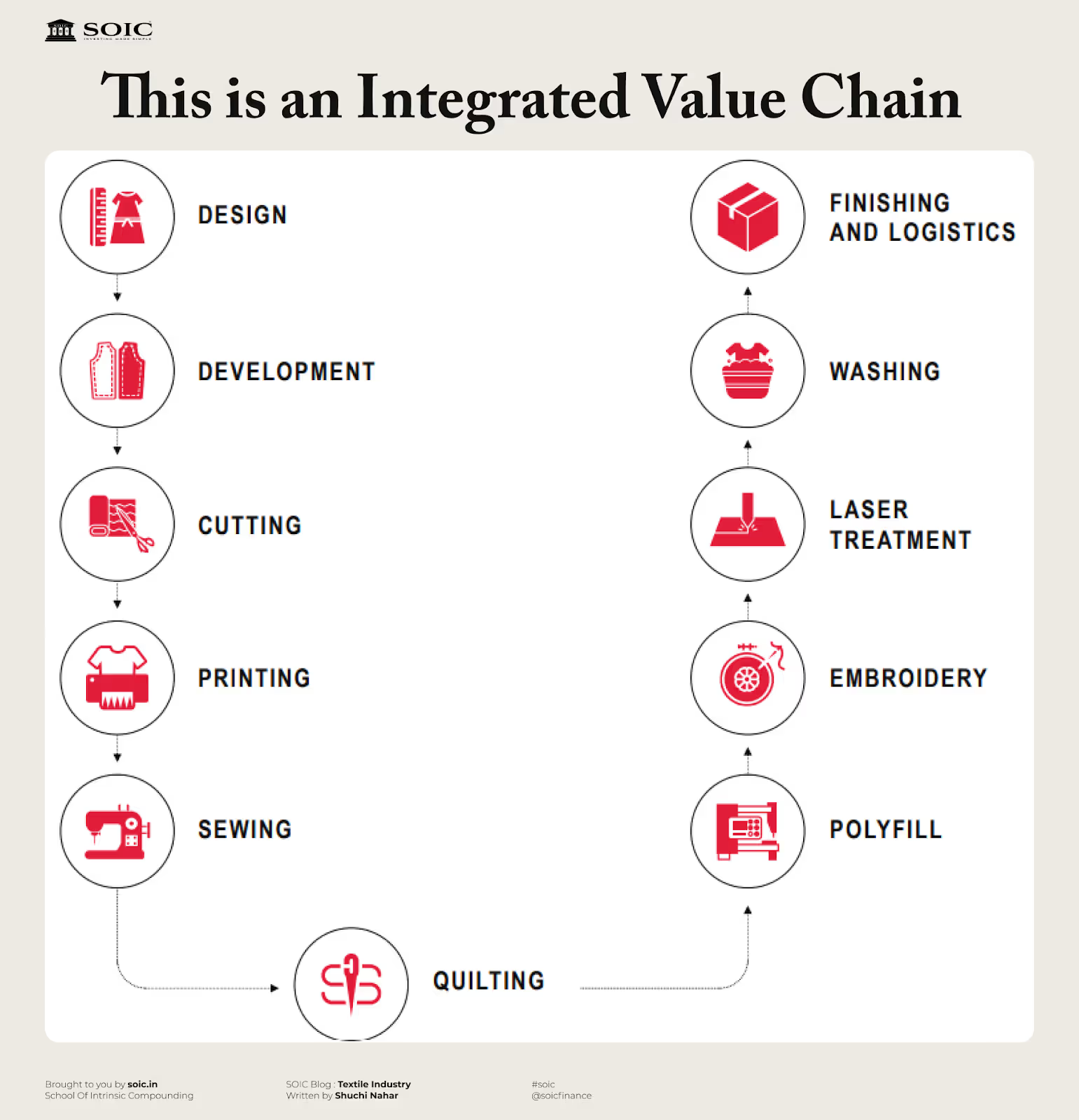

This is an Integrated Value Chain

Nature of Business:

Key Characteristics:

Examples:

Economics:

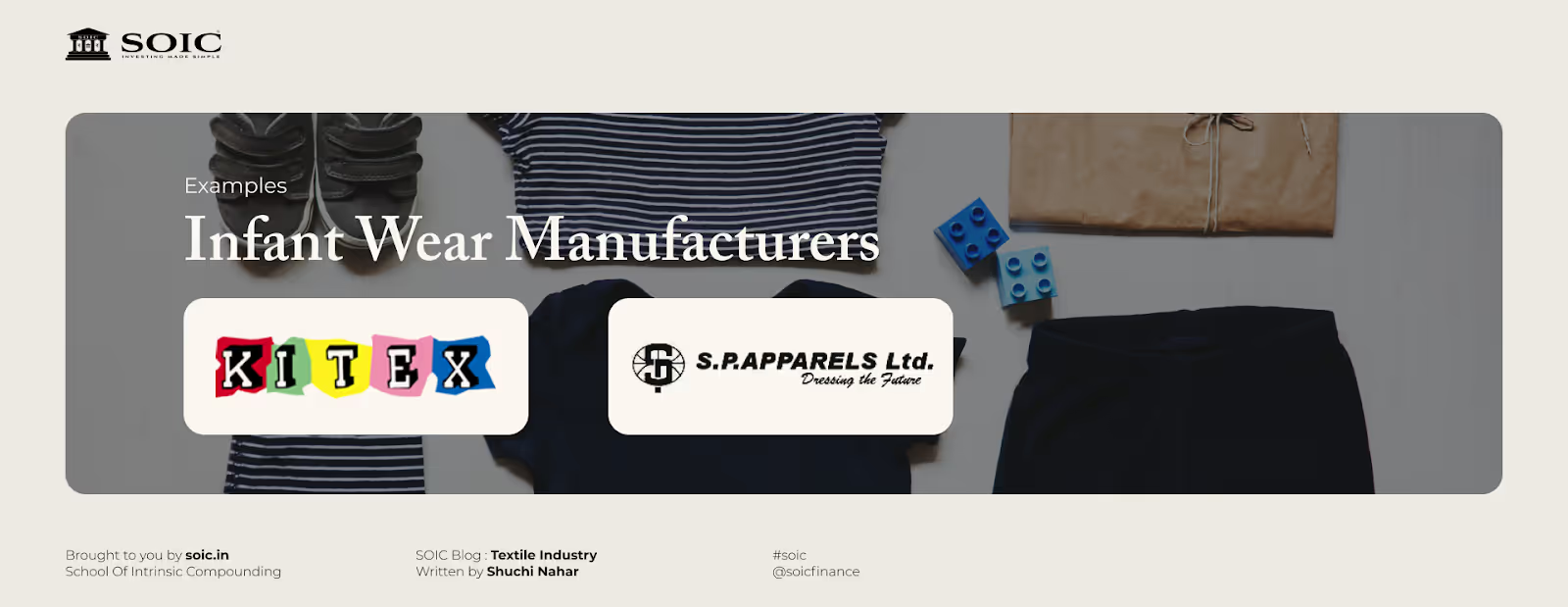

4. Infant Wear Manufacturers

The production of infant wear is a specialized but highly competitive industry because of the stringent regulatory approvals needed, particularly in the US and European markets. Businesses in this sector gain from a devoted clientele and expanding markets.

Complete Integration enables Quality Consistency and Timely Delivery (e.g. SP Apparels)

Nature of Business:

Key Characteristics:

Example:

Economics:

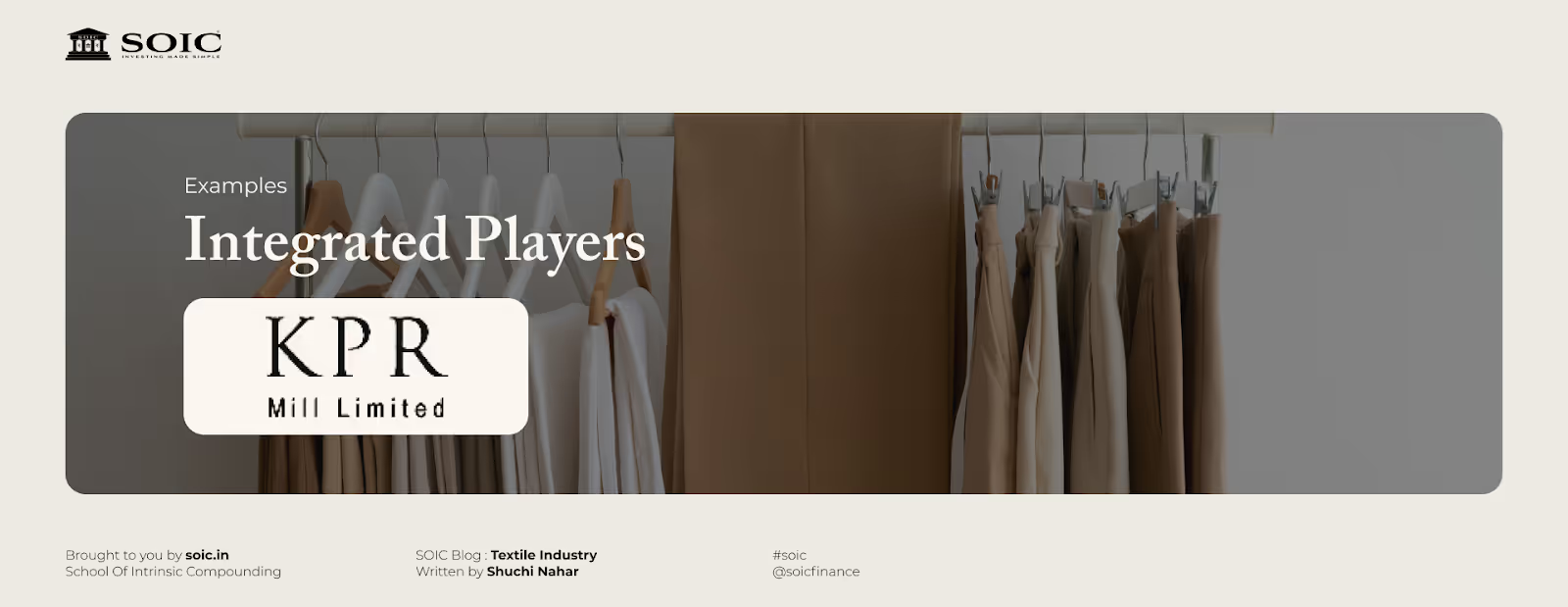

5. Integrated Players

At every stage of the textile value chain, integrated players hold a dominant position. Through their spinning, weaving, and processing activities, they maintain efficiency and quality control.

Nature of Business:

Key Characteristics:

Economics:

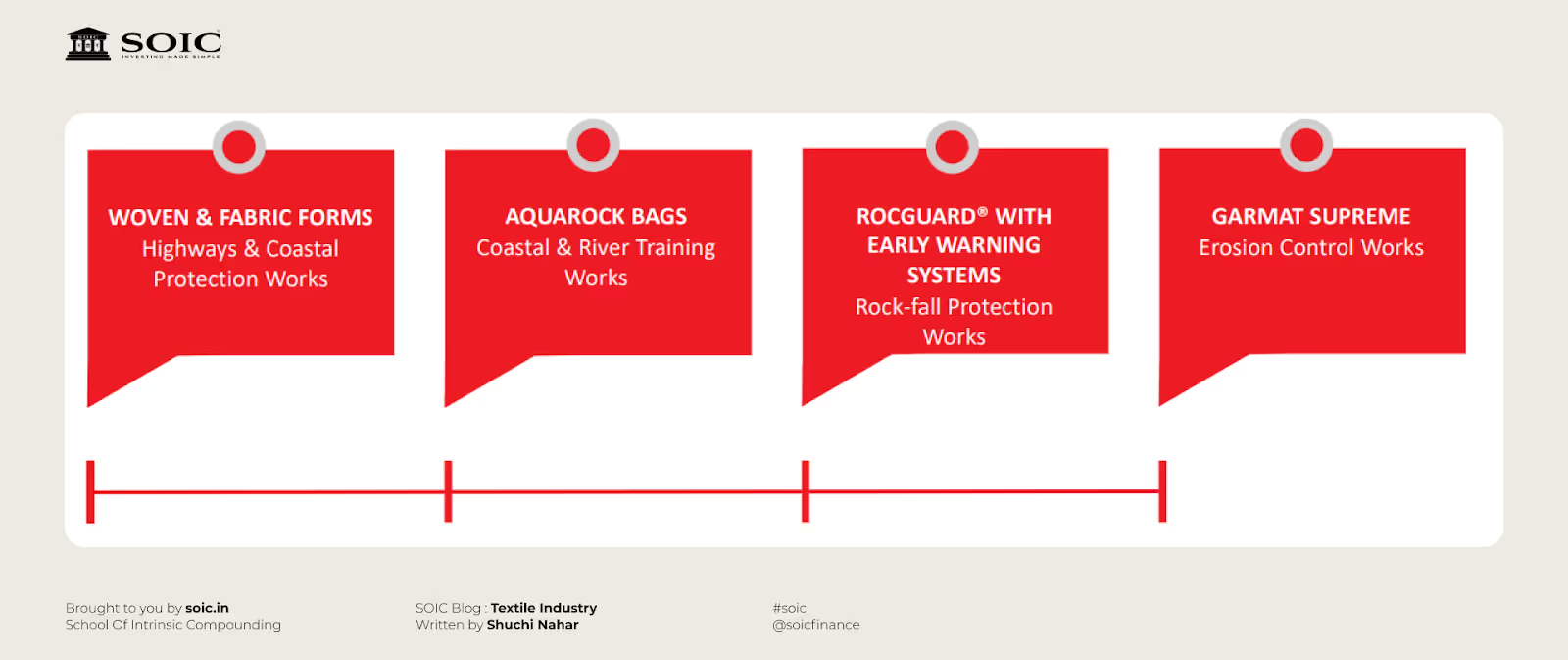

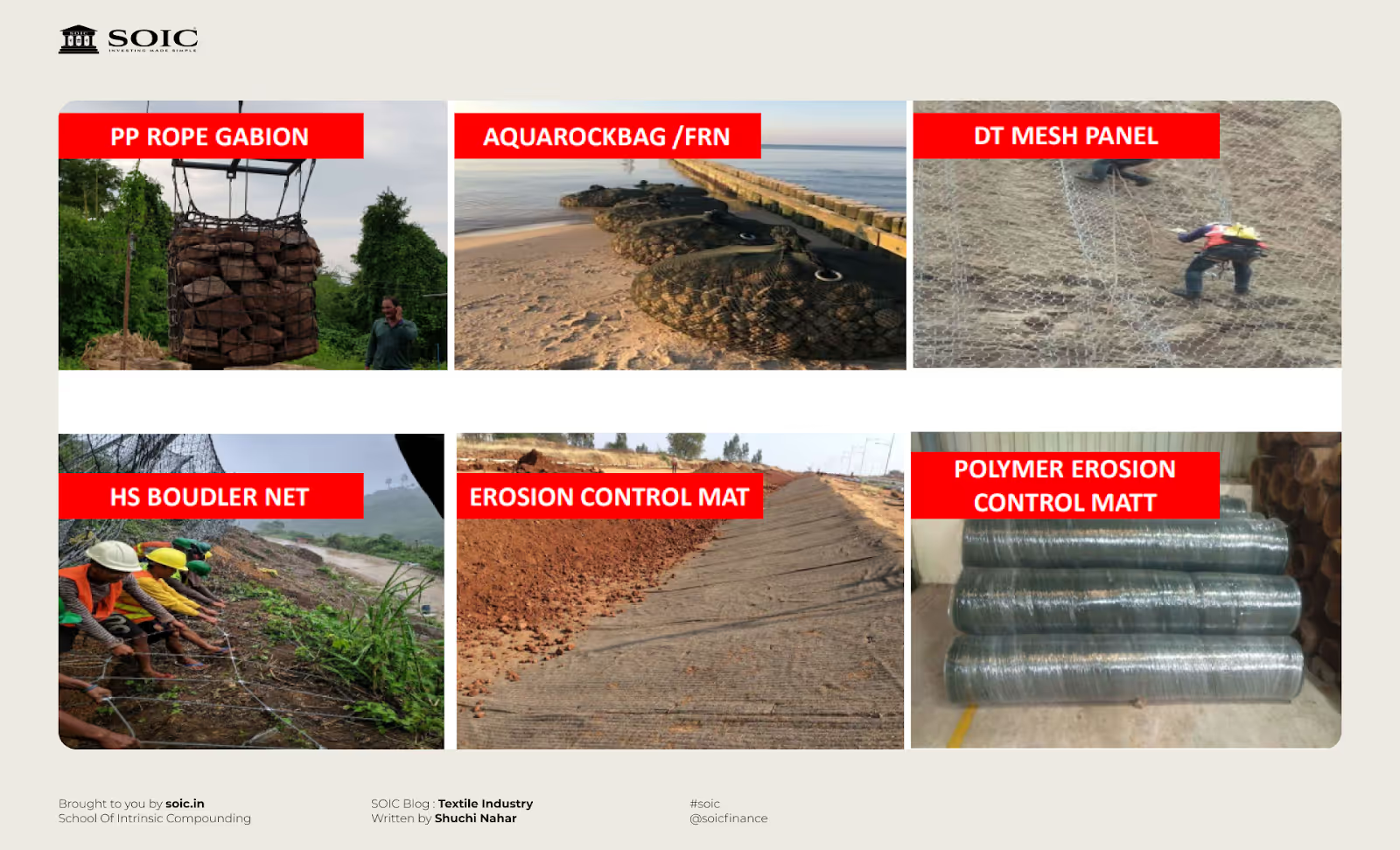

6. Technical Textiles

Technical textiles represent a growing, non-traditional segment within the textile industry. These products include items like army uniforms, geotextiles, fishing nets, and synthetic fabrics. It is an entry barrier-rich segment with high growth potential.

The Indian Technical Textile market has a huge potential of a 10% growth rate, increased penetration level of 9-10% and is the 5th largest technical textiles market in the world. India’s sportech industry is estimated around US$ 1.17 million in 2022-23.

Nature of Business:

Key Characteristics:

Examples:

Economics:

7. Home Textiles

Products like pillowcases, towels, and bed linens are the main focus of this subsegment. Due to cost advantages and international quality standards, Indian businesses in this sector are overtaking their Chinese rivals for market share.

India’s home textile industry is expected to expand at a CAGR of 8.9% during 2023-32 and reach US$ 23.32 billion in 2032 from US$ 10.78 billion in 2023.

Nature of Business:

Key Characteristics:

Examples:

Economics:

India’s textile industry is poised for incredible growth, thanks to several factors:

The future of the Indian textiles industry appears promising, driven by strong domestic consumption and export demand. India is implementing several major initiatives to enhance its technical textile sector. Increased demand for technical textiles, particularly in the form of PPE suits and equipment due to the pandemic, has further bolstered this growth. The government is actively supporting the industry through funding and machinery sponsorship.

Leading players in the sector are focusing on sustainability by manufacturing textiles made from natural, recyclable materials. As consumerism and disposable incomes rise, the retail sector has experienced rapid growth over the past decade, bolstered by the entry of several international brands such as Marks & Spencer, Guess, and Next into the Indian market. The growth of the textiles sector will be fueled by increasing household income, a growing population, and rising demand from industries such as housing, hospitality, and healthcare.

The technical textiles market for automotive applications is projected to grow from $2.4 billion in 2020 to $3.7 billion by 2027. The textile industry is diverse, with each segment presenting unique dynamics and return profiles.

Companies must navigate cyclical challenges, leverage their strengths, and adapt to changing market demands to succeed. Among these segments, integrated players and technical textiles stand out due to their high margins and return on capital employed (ROCE), while sourcing companies demonstrate how asset-light models can yield impressive returns.

As the industry evolves, the focus on sustainability, innovation, and value-added products will shape its future trajectory. The textile industry is at a transformative crossroads. With the right combination of innovation, sustainability, and strategic investments, it has the potential to reclaim its position as a global leader. As India addresses challenges and seizes opportunities—such as the Bangladesh+1 strategy—it is poised to create a brighter future for this longstanding industry.

Please share your thoughts, feedback, and learnings in the comments section below. We’d like to hear what you think.

Disclaimer: The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

%20(1).avif)

0 Comments