.avif)

Packaging is everywhere—it’s the backbone of modern trade, commerce, and consumption. Everything we buy, from groceries to electronics, must be packaged for both customer presentation and safety. Think about receiving a smartphone without its protective box or milk without its carton. Product longevity, usability, and safety are ensured by packaging. It serves as more than just a container; it allows industries to function and connects producers and consumers.

In the food and beverage sector, for example, packaging maintains perishables fresh during transportation, shields goods from damage, and enhances the e-commerce unboxing experience. Another sector where sterility and precise packaging can mean the difference between life and death is the pharmaceutical industry. Packaging is not only a functional need; it is also a marketing tool, a sustainability concern, and a dynamic industry.

This blog discusses how companies progress up the value chain, the cyclical nature of the packaging industry, and the reasons why raw material cycles significantly affect profitability. Whether you are an investor trying to identify patterns or just interested in this ubiquitous sector, this is your resource for learning about how packaging affects economies, businesses, and our daily lives.

The packaging industry operates through a systematic value chain that ensures raw materials transform into products that meet the specific needs of end consumers. Here’s a detailed breakdown:

The value chain starts with suppliers of raw materials such as plastic resins, aluminum, paper, and specialty films.

Key materials include:

* Polyethylene Terephthalate (PET): Used in rigid packaging.

* Biaxially Oriented Polypropylene (BOPP): For films in food and FMCG packaging.

* High-Density Polyethylene (HDPE): Used for industrial applications.

* Polypropylene (PP): is valued for its versatility and resistance against chemicals and heat.

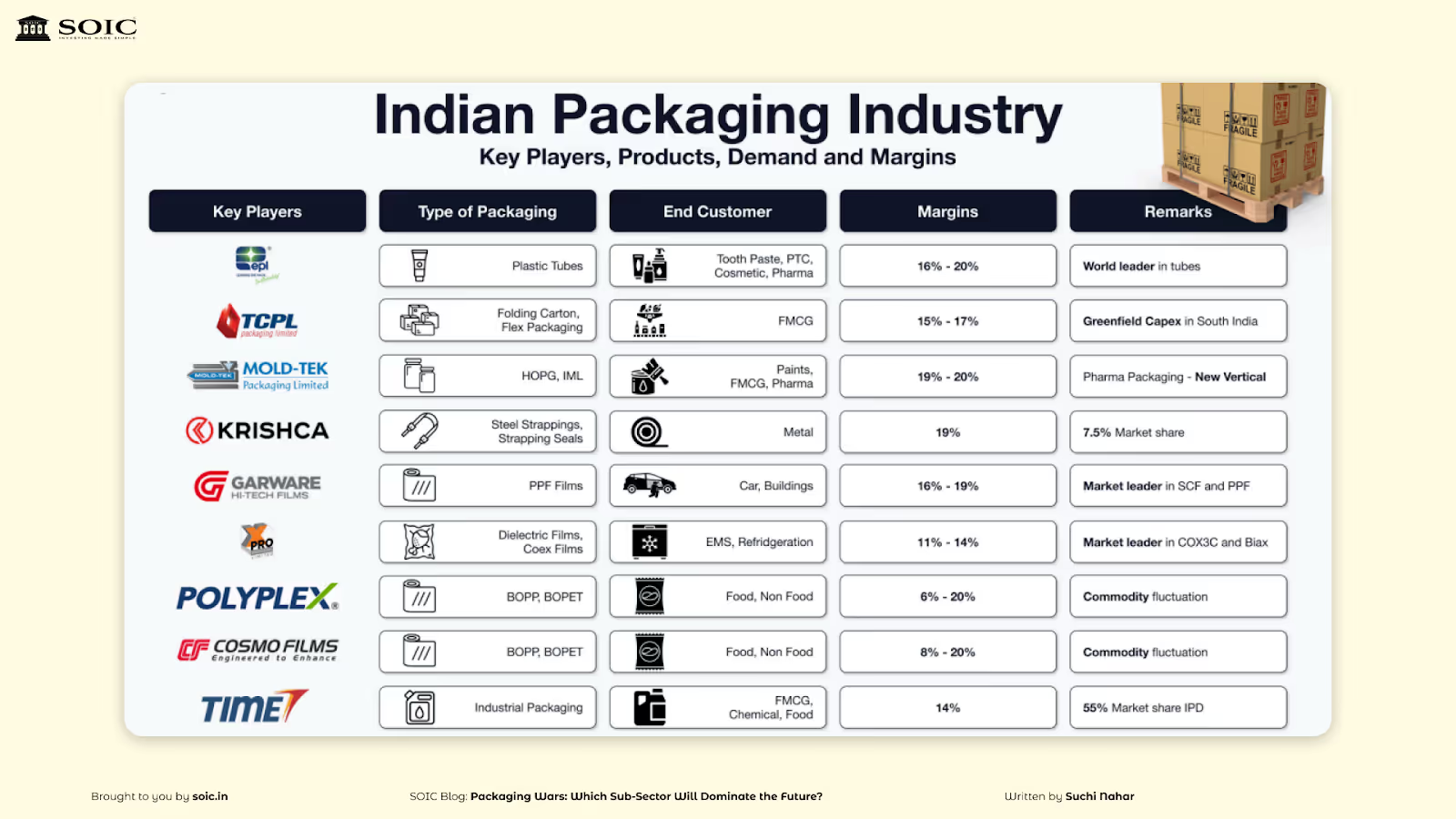

Notable suppliers: Reliance Industries, GAIL, and Indian Oil for polymers; Ballarpur Industries and ITC for paperboard.

Converters transform raw materials into semi-finished or finished packaging products. This stage includes:

Company examples:

These players cater to different end-use industries with tailored solutions:

The packaging industry is often termed the backbone of multiple sectors like FMCG, pharma, electronics, and industrial goods. In this blog, we will explore the detailed value chain of the packaging industry, examine the role of prominent companies, and delve into margins, market trends, and business opportunities.

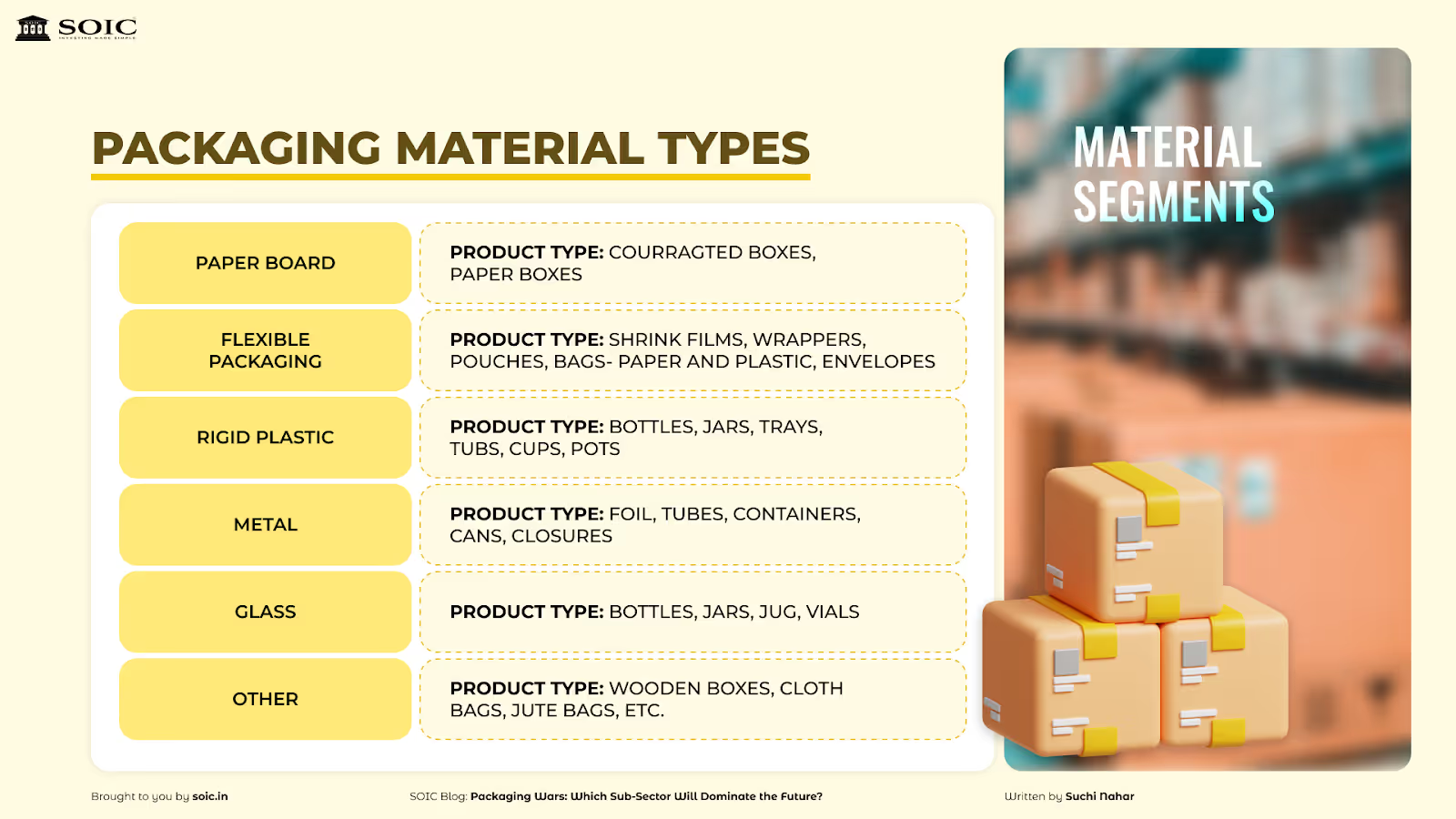

Rigid packaging includes containers, tubes, and caps that provide structural integrity.

Key Highlights:

Flexible packaging caters to a wider range of consumer goods due to its cost efficiency and adaptability.

Key Highlights:

This segment serves B2B industries, where durability and functionality are critical.

Key Highlights:

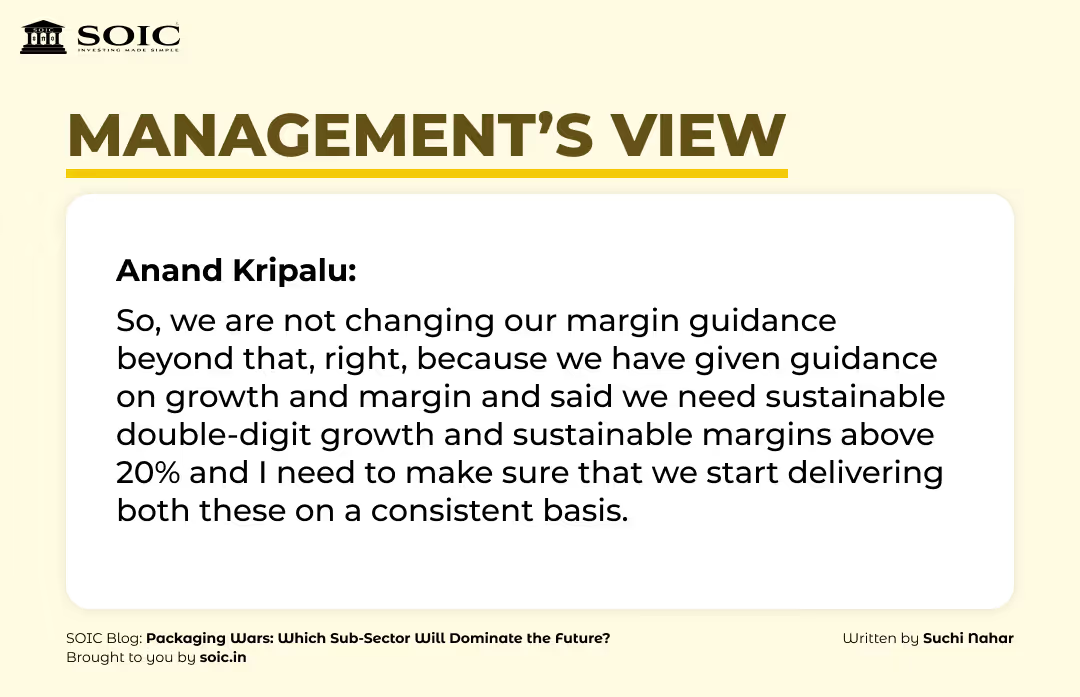

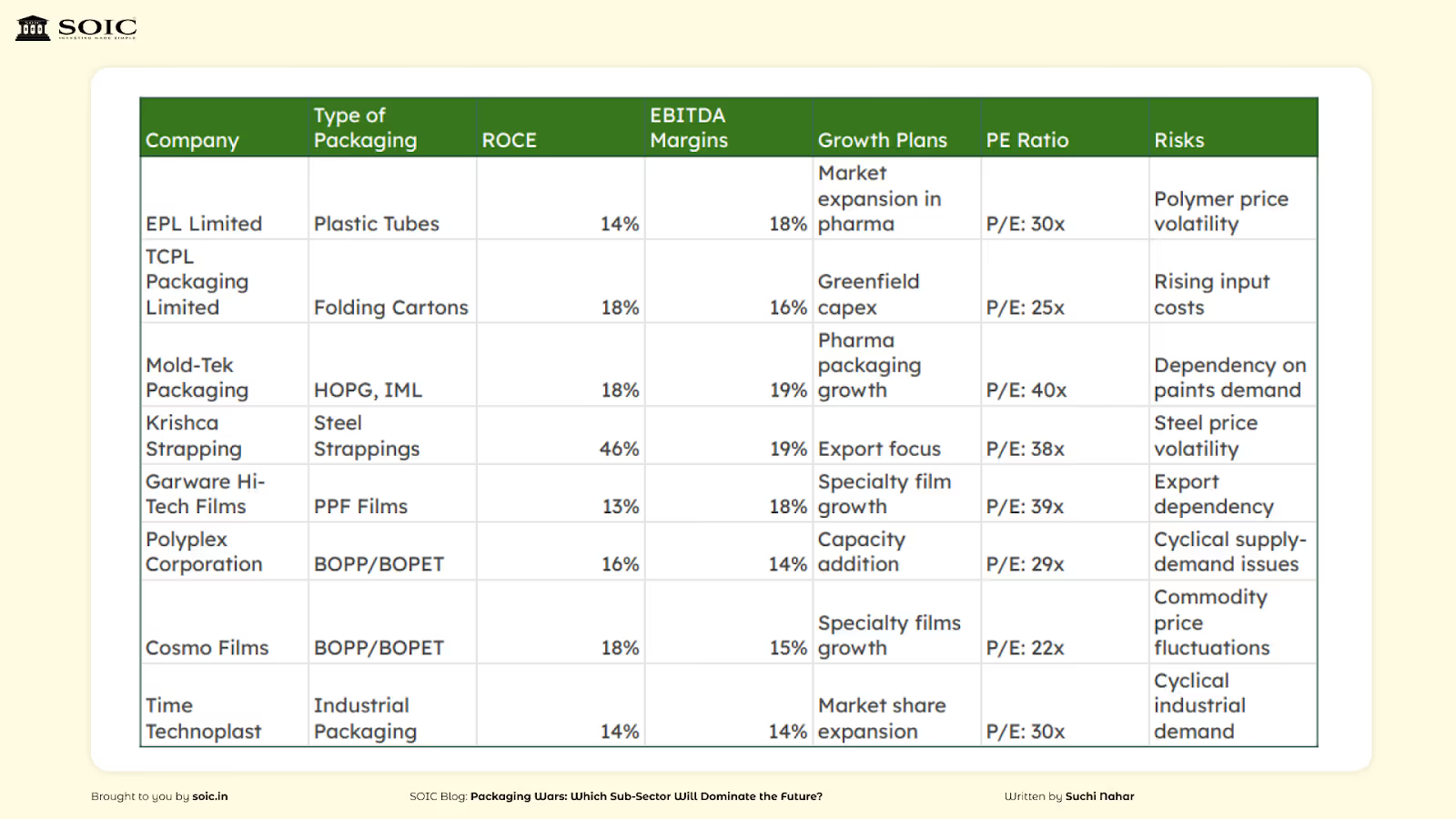

The packaging industry has traditionally been cyclical, characterized by 2-3 years of downturn followed by 2-3 years of growth. Historically, the ideal time to explore investment opportunities in this sector is when companies are trading at high P/E ratios, often signaling a market peak.

At present, the industry appears to be approaching its peak, though it hasn’t been fully realized yet. This suggests that companies in the BOPP and BOPET segments could become more attractive investment options in the coming year as the cycle potentially begins to turn downward again.

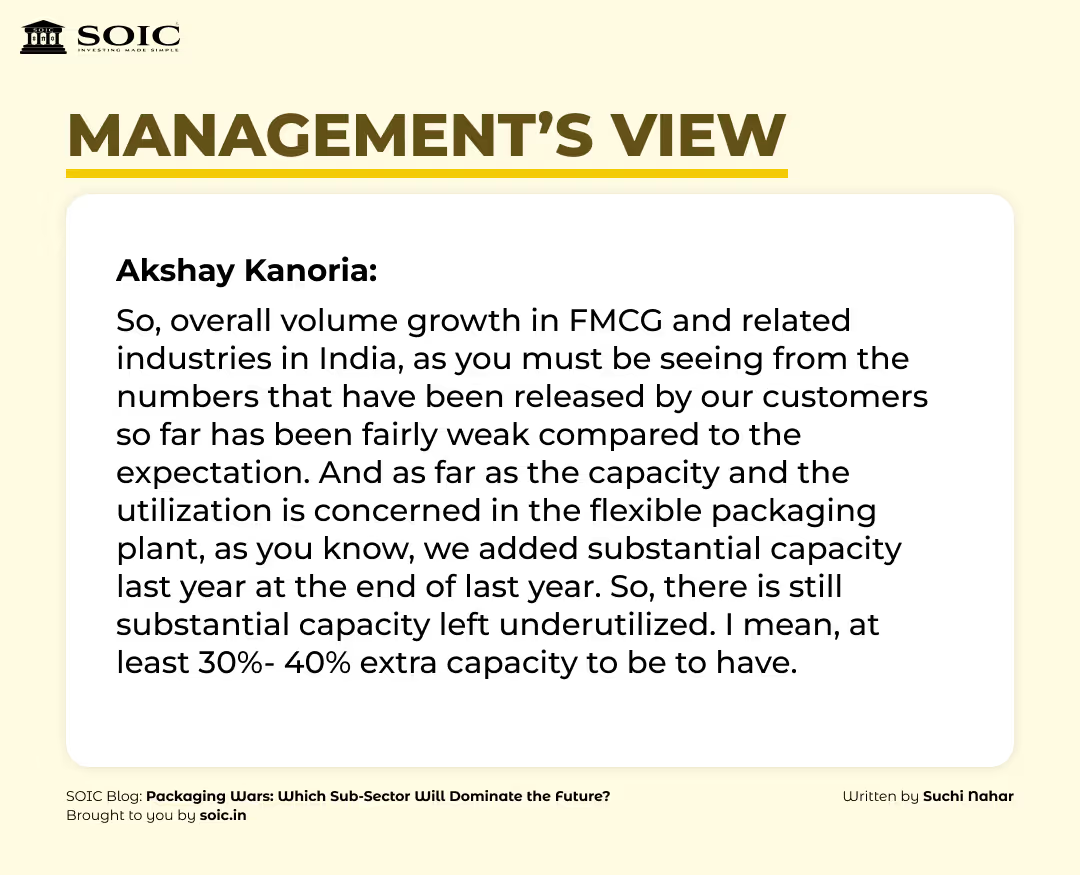

The packaging industry presents a wide range of opportunities across various sub-segments, each accompanied by its own set of risks. For example, companies that produce BOPP and BOPET films are cyclical and significantly impacted by supply and demand dynamics, making them appealing during times of low valuations.

In contrast, specialty packaging—such as pharmaceutical tubes and in-mold labeling (IML)—can offer consistent growth due to high-margin products.

It is crucial to understand the end-user industries and growth drivers for each company. Companies that are moving up the value chain or expanding into high-growth areas, like Mold-Tek with its focus on pharmaceuticals or Cosmo Films with its specialty films, can provide better returns on capital employed (ROCE) and more stable margins.

Which packaging sub-segment do you find most intriguing—commodity films like BOPP/BOPET or niche areas like pharma and industrial packaging? Let us know your thoughts!

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

0 Comments