Indian weddings are lavish affairs that include a variety of rituals and expenditures. The industry spurs consumption in categories like jewellery & apparel and indirectly benefits autos & electronics. With an average Indian spending twice as much on weddings as on education, the US$130 billion Indian wedding industry generates enormous economic activity.

Despite political efforts to curtail them, the splendor of Indian luxury weddings continues to shine in distant locales. As an economic powerhouse, India hosts 8-10 million weddings annually, making it the world's largest wedding destination. The wedding industry, nearly twice the size of its US counterpart, significantly boosts key consumption sectors, valued at approximately $130 billion.

Every year, India hosts about 10 million weddings. India is the world's second-largest wedding industry. According to a report published by the Economist, the wedding industry is the fourth-largest industry in India, recording a huge spending of US$ 130 billion per year. Its substantial scale provides employment opportunities for millions.

Supported by campaigns such as Prime Minister Narendra Modi's drive to "Wed in India," the sector is expected to see more than 42 lakh weddings between January 15, 2024, and July 15, 2024, with an estimated cost of US$ 66.4 billion (Rs. 5,50,000 crore).

Over 4 lakh weddings are anticipated to take place in Delhi alone, adding to the industry's economic impact with an estimated US$ 18.1 billion (Rs. 1,50,000 crore) in revenue. This time frame not only represents the industry's recovery from pandemic-related downturns but also highlights its significance as a key economic engine.

The Indian wedding industry is well-positioned to expand and change in the wake of these developments, becoming an important part of the country's economic structure. Prime Minister Narendra Modi initiated a campaign like 'Make in India,' termed 'Wed in India.' This initiative encourages affluent industrialists to organize at least one destination wedding per year in Uttarakhand, aiming to position the state as a notable wedding destination.

Due to small-scale operations and vendors' limited online presence, the Indian wedding industry has historically been characterized by its lack of organization. However, it has shown significant resilience and growth potential.

This multibillion-dollar industry, which has historically relied on offline planners, friends, and personal networks, has been fragmented, lacking dominant market players and having a small digital footprint. However, according to a report published by Business Outreach, the industry is recovering, showcasing an impressive annual growth rate of 7-8%, and is projected to reach a market size of US$ 75 billion in the 2023-24 wedding season.

This growth is driven by factors such as rising consumer spending power and the expansion of the luxury market segment, alongside a demographic trend that sees a substantial portion of the population entering marriageable age within the next five years.

Indians spend a lot of money on weddings, which may be out of proportion to their income or wealth in a society that values values otherwise. Furthermore, the propensity to overspend is evident across all economic classes. The average wedding costs $15k, which is a multiple of household income or per capita. Remarkably, the average Indian couple spends about twice as much on weddings as they do on education (from pre-primary to graduation), whereas in nations like the US, the spending is less than half.

Particularly for the elite: Exotic domestic and foreign locales, opulent lodgings, exquisite cuisine prepared by Michelin-starred chefs, and performances by famous people and professional artists—luxury Indian weddings must be experienced to fully comprehend. Interestingly, there have been efforts by politicians to curb lavish weddings at different points in the past!

Luxury weddings in India are typically held in exotic domestic or international destinations. Guest counts on average range between 300 and 500 people. The trends in destinations, wedding apparel, and experiences are often influenced by weddings of high-profile Bollywood celebrities and industrialists.

The average expenditure for luxury weddings falls within the range of Rs 20mn to Rs 30mn (~US$200k to ~US$400k USD), with the higher end of the luxury wedding spectrum often exceeding these figures by several multiples. This budget encompasses expenses for hosting 5 to 6 functions/events, luxurious accommodations at top-tier hotels, lavish catering, decor, and entertainment (expenses related to jewellery, wedding attire, and airfare are not included in these estimates).

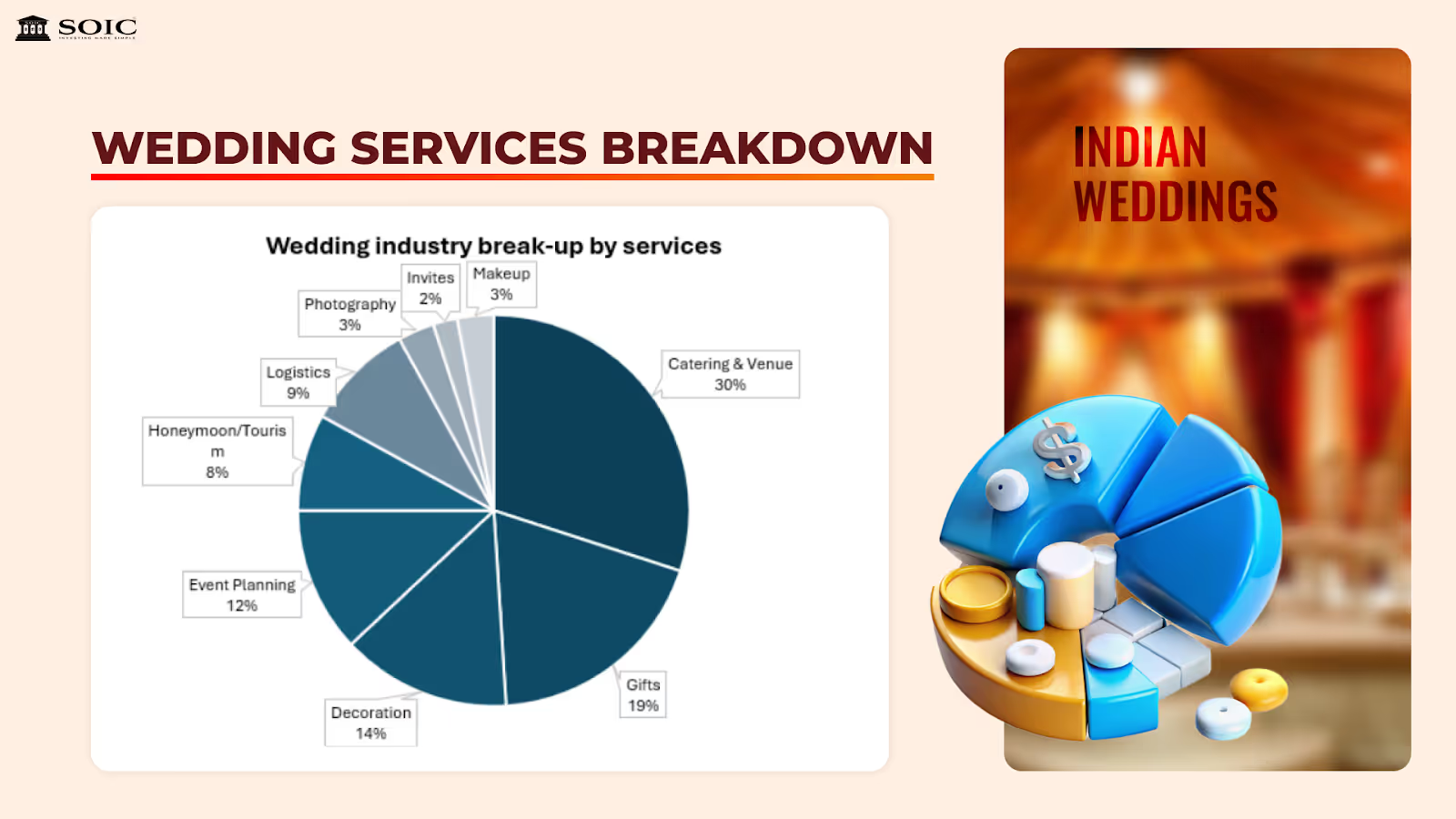

Two distinct peak periods are observed here: November to mid-December and mid-January to July which is often referred to as the 'Wedding Season' in India. Economic activity across India surges during the wedding season, especially during the first peak period, which also coincides with the festive period in India, and sector beneficiaries track this closely.

Growing categories with the emerging trend of destination weddings, stay-and-travel is another large expenditure in a wedding, given the large number of guests involved, many of which are outstation guests. Further, with the growing trend for destination weddings, demand for hotels and travel has grown further, in our understanding. Leading hotel chains such as IHCL, EIH, and Chalet Hotels and airline companies such as Indigo, SpiceJet, etc. are key among listed companies.

The traditional marriage landscape has been transforming in India with an increasing number of Indian couples choosing to get married at exotic domestic and international destinations. Factors contributing to this include increasing household incomes, wedding planners assisting with the planning and execution, increased availability of wedding service vendors at new locations, and the influence of celebrity destination weddings on social media.

According to the 2023-24 wedding industry report by WedMeGood, which surveyed over 2,400 brides and grooms (primarily in urban India), 21% of the surveyed couples had destination weddings, up from 18% in 2022. Popular domestic destinations include Goa, Udaipur, Jaipur, Kerala, and Uttarakhand, while popular international destinations include Thailand, Bali, Italy, and Dubai, to name a few.

Overview of popular domestic wedding destinations India offers an abundance of options for destination weddings, from the palaces and heritage properties of Udaipur and Jaipur in Rajasthan to the beaches of Goa and backwaters of Kerala, as well as destinations such as Uttarakhand, which feature the backdrop of the Himalayas. Additionally, these locations include excellent connectivity via road, air, and rail and an abundance of experienced wedding service vendors. Government of India's continued focus to make India a preferred destination wedding hub.

There is also an opportunity for large organized players to gain market share as they build capabilities to cater to regional preferences. Several companies, such as Titan, Kalyan Jewellers, Vedant Fashions, ABFRL, etc. are well-placed from this shift to become organized players in a growing market.

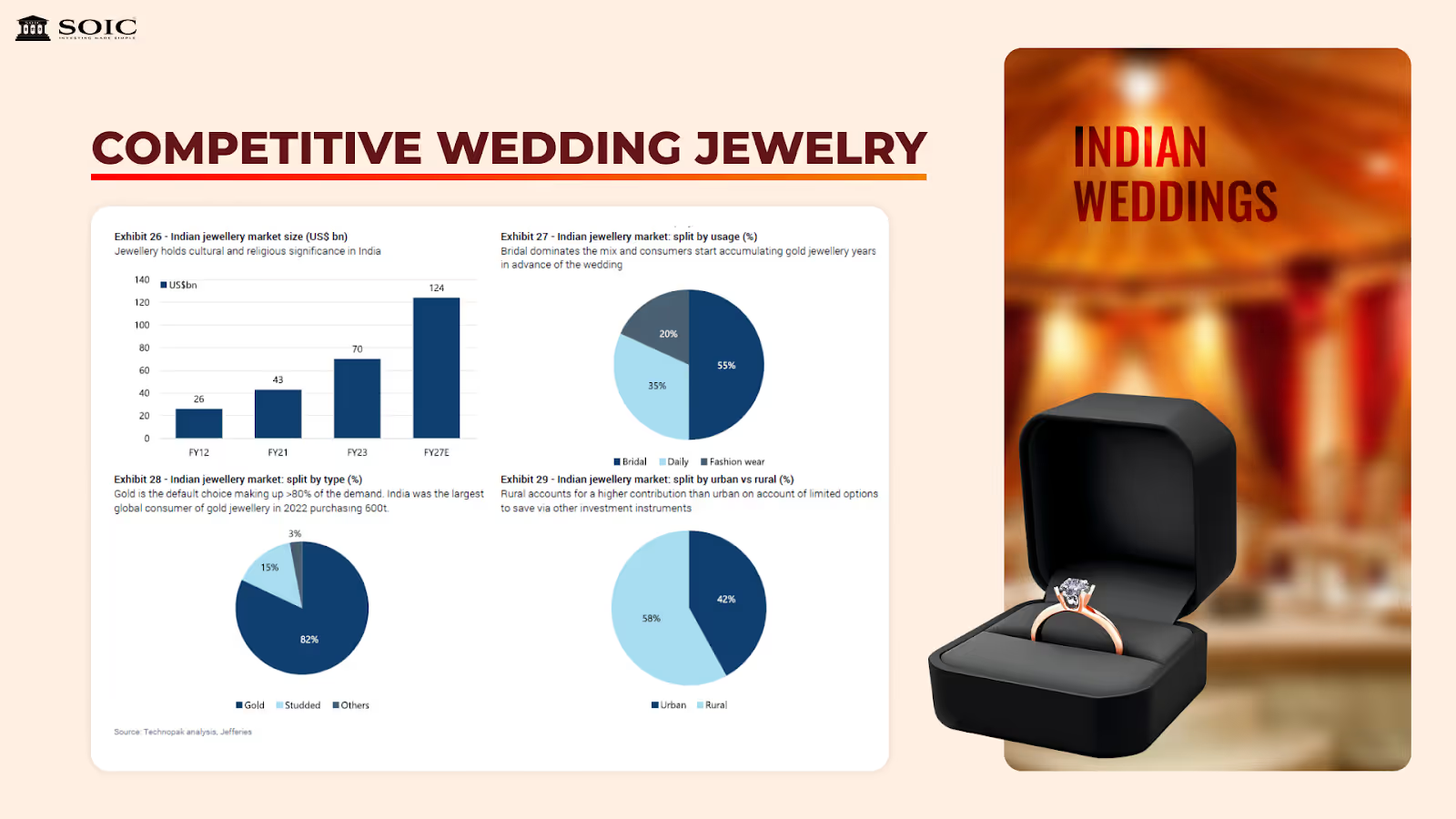

Jewellery holds a position of immense importance in Indian weddings due to its profound cultural and religious significance. It often represents the largest purchase category during these celebrations. Within the jewellery industry, weddings serve as a crucial demand driver, accounting for 50% to 55% of the total market by weight. Wedding jewellery is the predominant segment, followed by daily wear at 35% and fashion wear at 20%. Organized jewellery retail, which constituted about 6% of the market in 2007, has grown to approximately 37%, benefiting major Indian retailers like Titan (Tanishq), Kalyan Jewellers, and Senco Gold.

Compared to daily wear or fashion jewellery, jewellery bought during the wedding is largely plain gold jewellery which has lower margins. This segment also has much higher competitive intensity, greater sensitivity towards making charges, and hence a greater share of unorganized and regional players. Further, regional preference plays a key role, with designs varying across states.

The wedding sets of brides in south Indian states on an average are significantly heavier than that of non-south states. Even states with comparable per capita income from south and non-south regions have stark differences when it comes to jewellery purchase patterns.

Over the last few years, organized players have increased focus on the wedding jewellery segment despite its lower margins, given its large opportunity size. Players such as Titan have introduced region-specific wedding collections to better compete with local players.

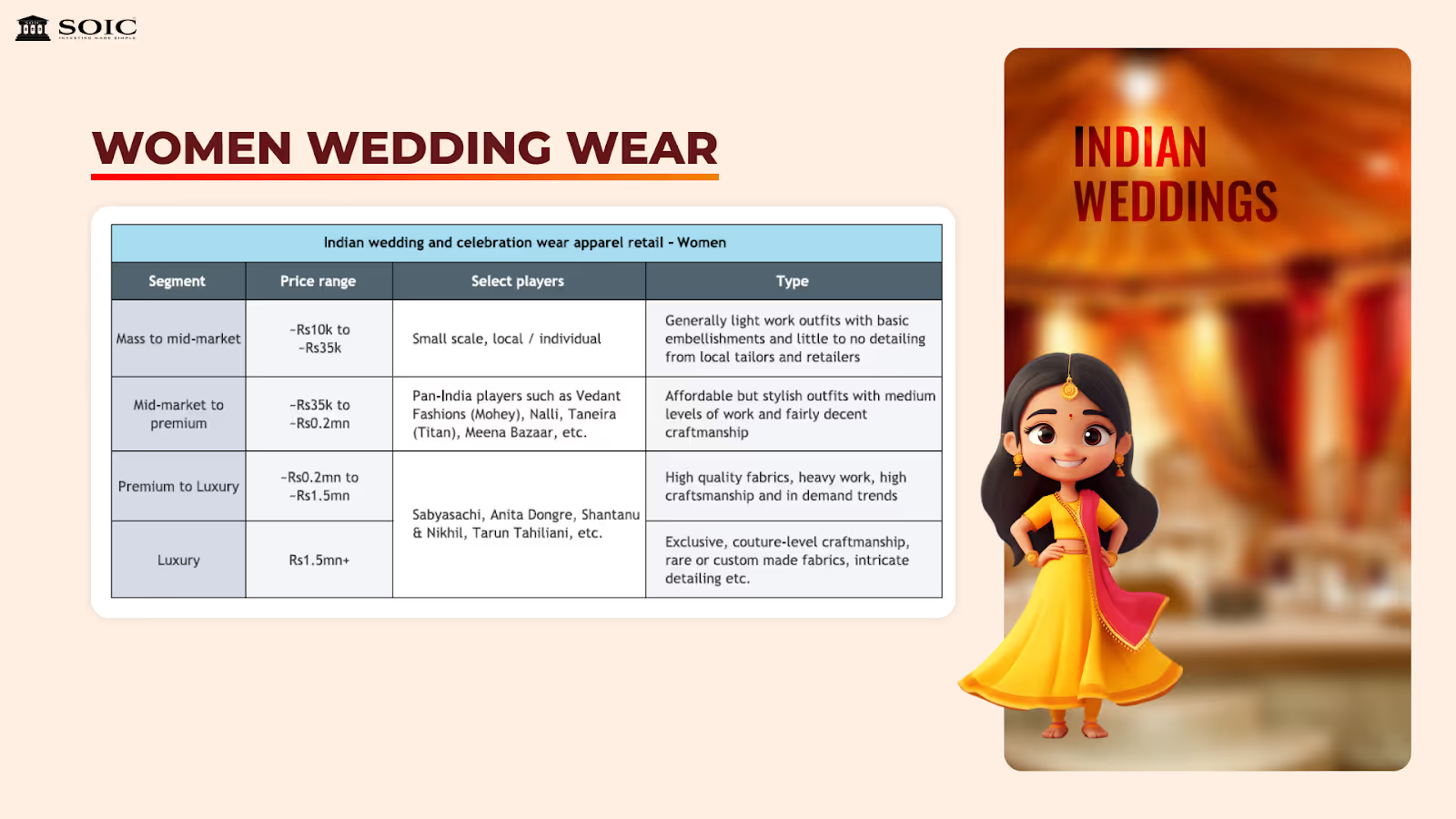

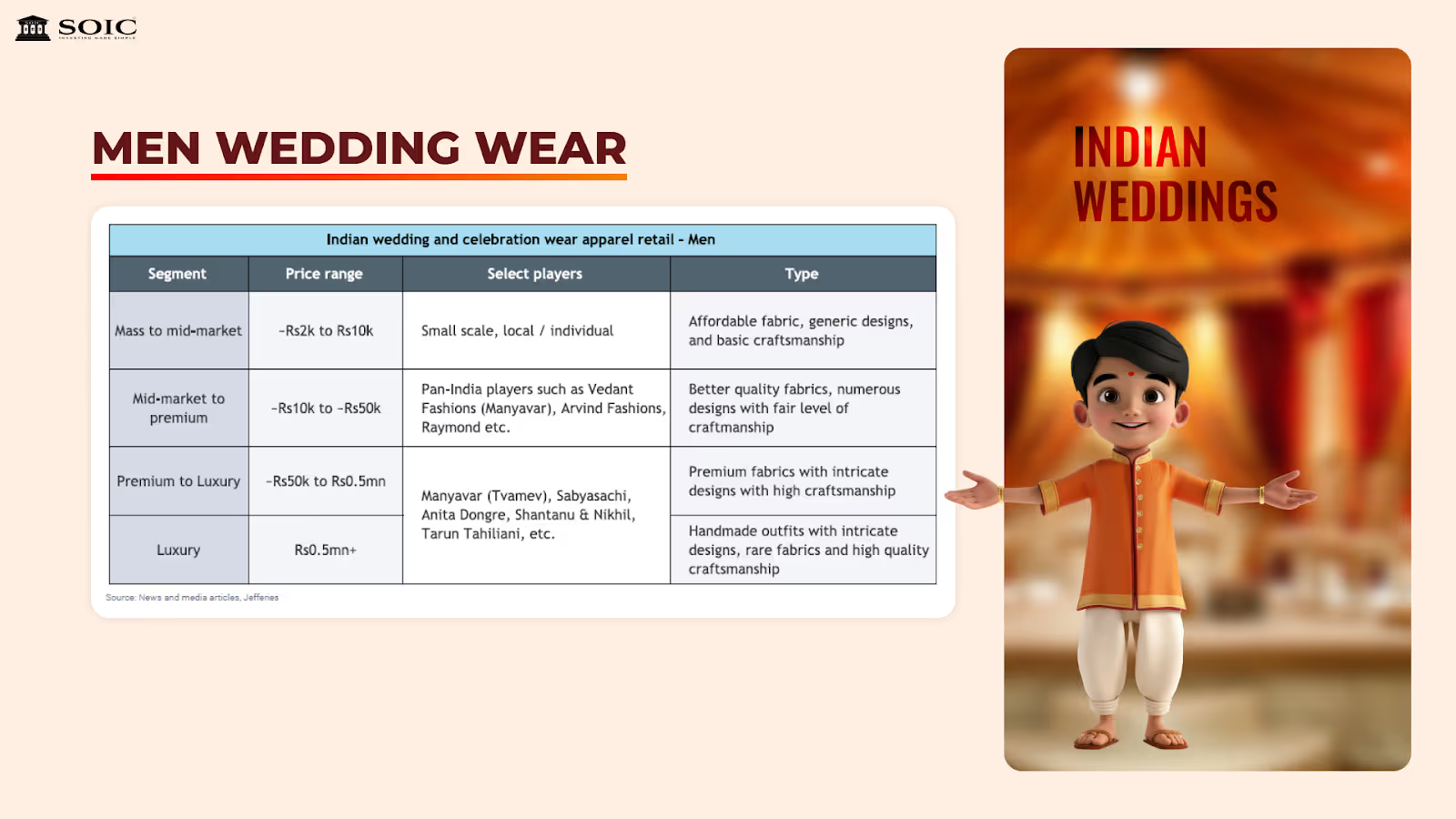

Of the US$84bn apparel retail market, ~11% is led by wedding and celebration wear, the bulk of which are driven by the former. This includes apparel not only for the bride and groom but also for the families, friends, and even the guests. Women’s wear dominates, accounting for nearly 70%–75% of the total Indian wedding and celebration wear market.

Similar to wedding jewellery, bridal wear preferences differ by region and religion and include intricate lehengas to elegant sarees. In the premium and luxury segments, outfits are typically handmade, crafted with rare fabrics and lavish embellishments, and showcase intricate craftsmanship. Premium and luxury segment bridal lehengas are curated as per the frame and size of the bride and often take over months to create. Bridal lehengas with heavy, intricate work can even weigh over 10 kgs in some cases.

In the premium and luxury segments, outfits are typically handmade with high-quality craftsmanship using rare fabrics and are catered to by individual designers. Based on our industry interactions, most of the artisans (known as kaarigars in India) who specialize in wedding and celebration wear hail from Farrukhabad in the Northern State of Uttar Pradesh and Kolkata, in the Eastern state of West Bengal.

Similar to jewellery, the wedding-related apparel industry is also largely unorganized given the preference for customization, deep cultural nuances, and a fragmented supply chain. However, this is also changing gradually as more organized players are entering the category given its strong growth prospects.

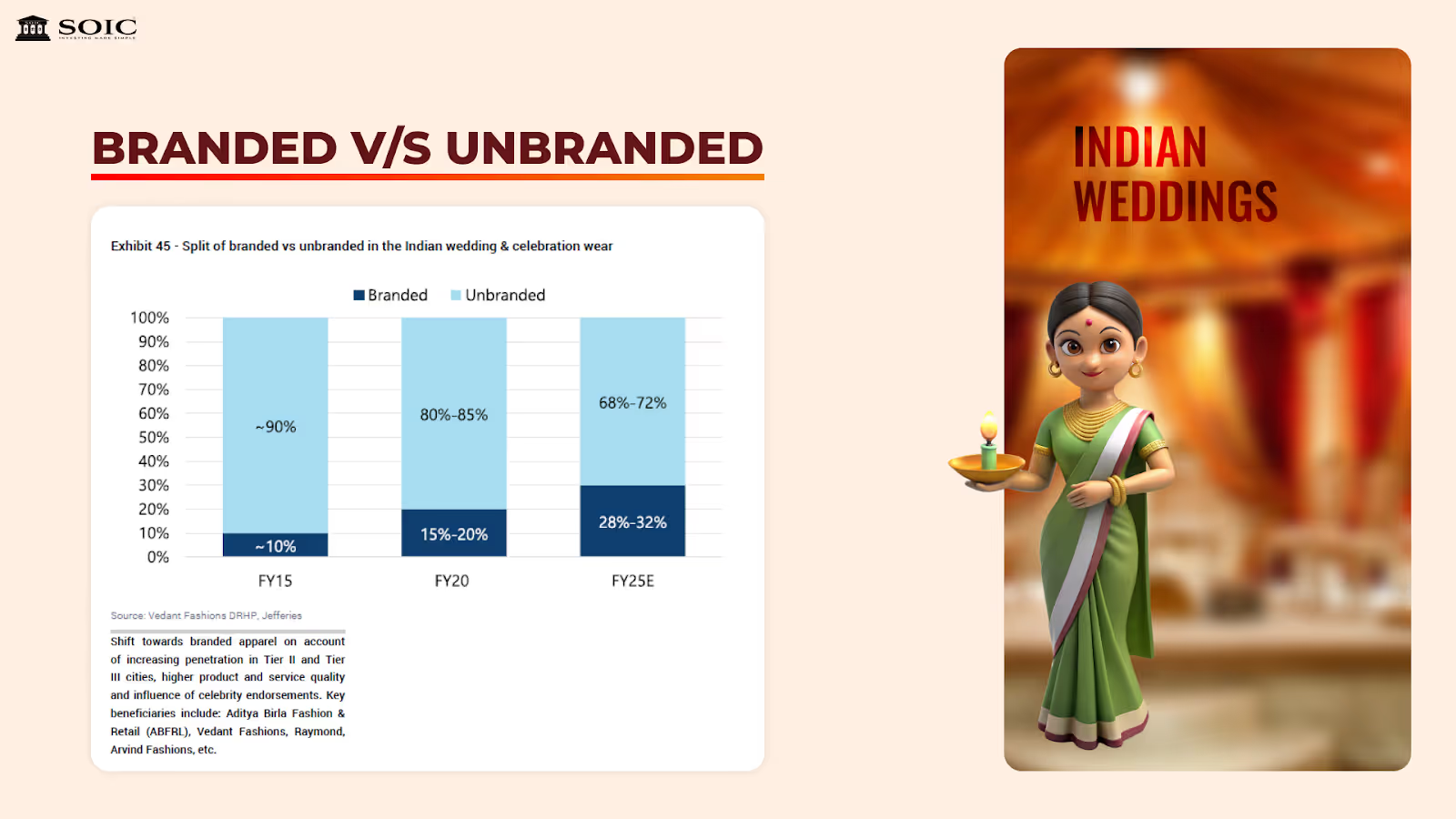

The industry has been witnessing a shift towards branded apparel on account of incremental penetration in Tier II and Tier III cities alongside Tier I/metros, higher product and service quality, and the influence of celebrity endorsements. Key beneficiaries of the trend include Vedant Fashions, Aditya Birla Fashion & Retail, Raymond, etc.

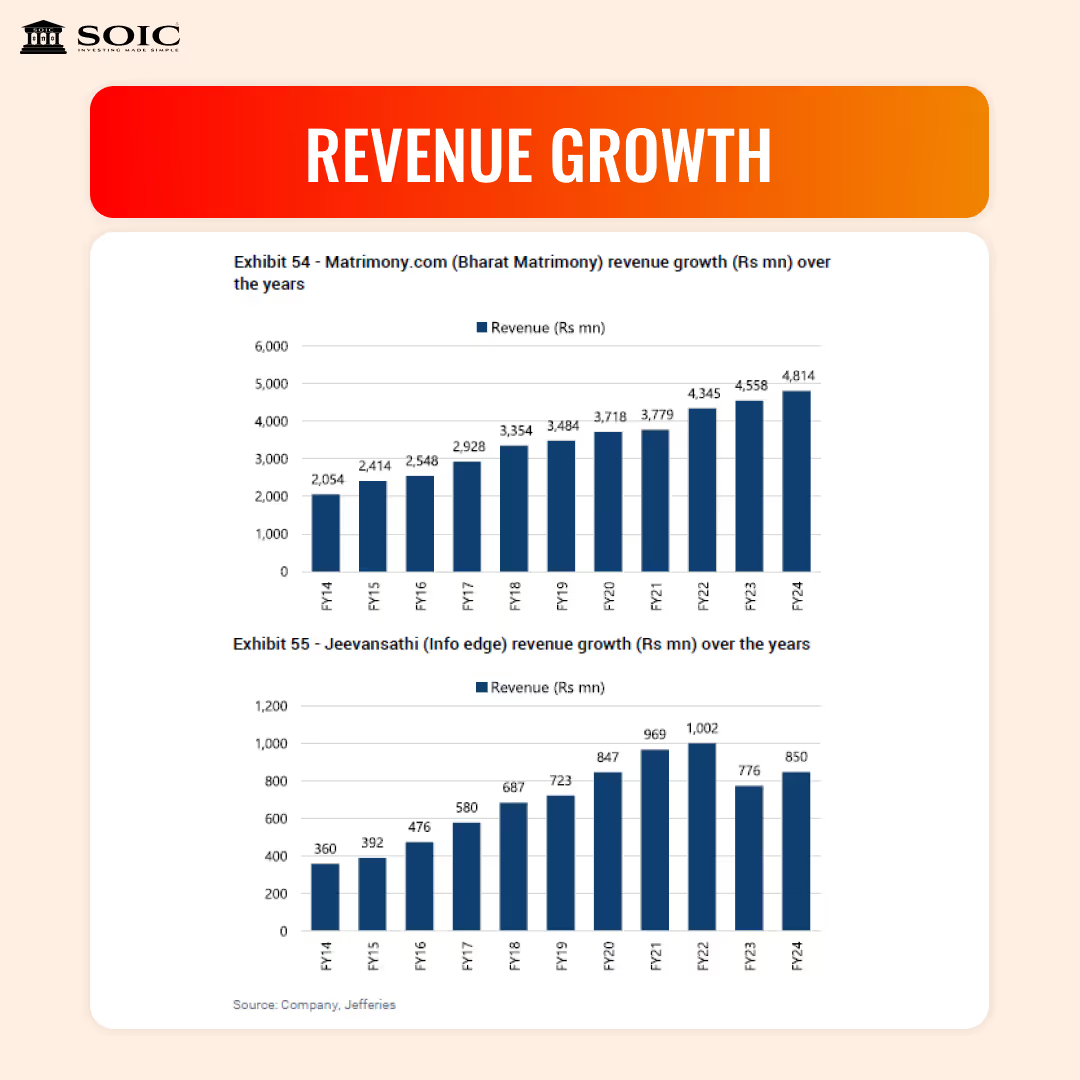

Matchmaking is an industry, predominantly unique to Asian countries and especially to those where arranged marriages are still the dominant construct. Based on a 2018 survey of over 160k households, conducted by The Lok Foundation & Oxford University, over 90% of Indian marriages are arranged, and this percentage has remained consistent across decades and remains fairly consistent across education levels.

The match-making process is initiated with prospective brides and grooms being connected via the parents, familial social network, or via specialized matchmakers/marriage brokers. Potential brides and grooms are matched based on several factors, including but not limited to, financial background, expected education levels, professional background, social class, customs, etc. Post which not only the couple but also the families need to swipe right on the match.

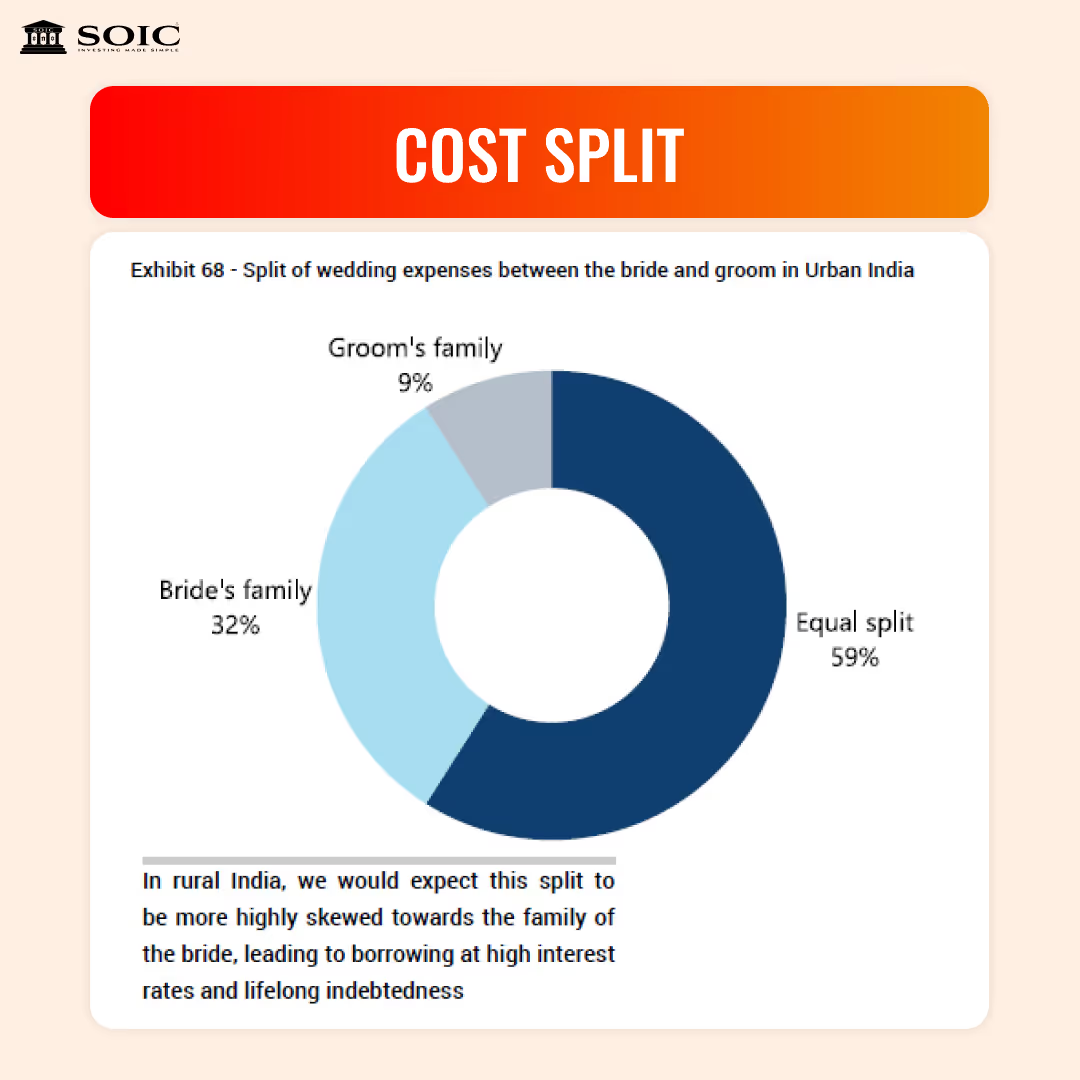

The responsibility of financing weddings in India has traditionally fallen on the families of the bride and groom, a practice deeply embedded in cultural traditions and societal norms. Recognizing the significant financial obligation, families often start saving for wedding expenses many years in advance. In recent years, however, a noticeable shift in this financing structure has emerged. While family contributions continue to play a major role, there is a growing trend of couples contributing a larger portion from their own savings.

The growing use of bank and lending platform loans rather than the more conventional option of borrowing from friends or family in the event that expenses surpass the budget is another significant trend in the wedding industry. Depending on the borrower's credit history, these loans have higher interest rates, usually between 10% and 36% annually. Due to higher funding costs and lower customer quality, NBFCs typically charge higher interest rates on personal loans than banks.

Based on a press release by digital lending platform, IndiaLends, ~20% of the applications received from Indians aged 20-30 years in 2018-19 were for financing weddings; additionally, the same platform surveyed over 1,200 millennials in 2023, and of those surveyed who planned to self-fund their wedding, over 26% would consider taking a personal loan to finance their wedding.

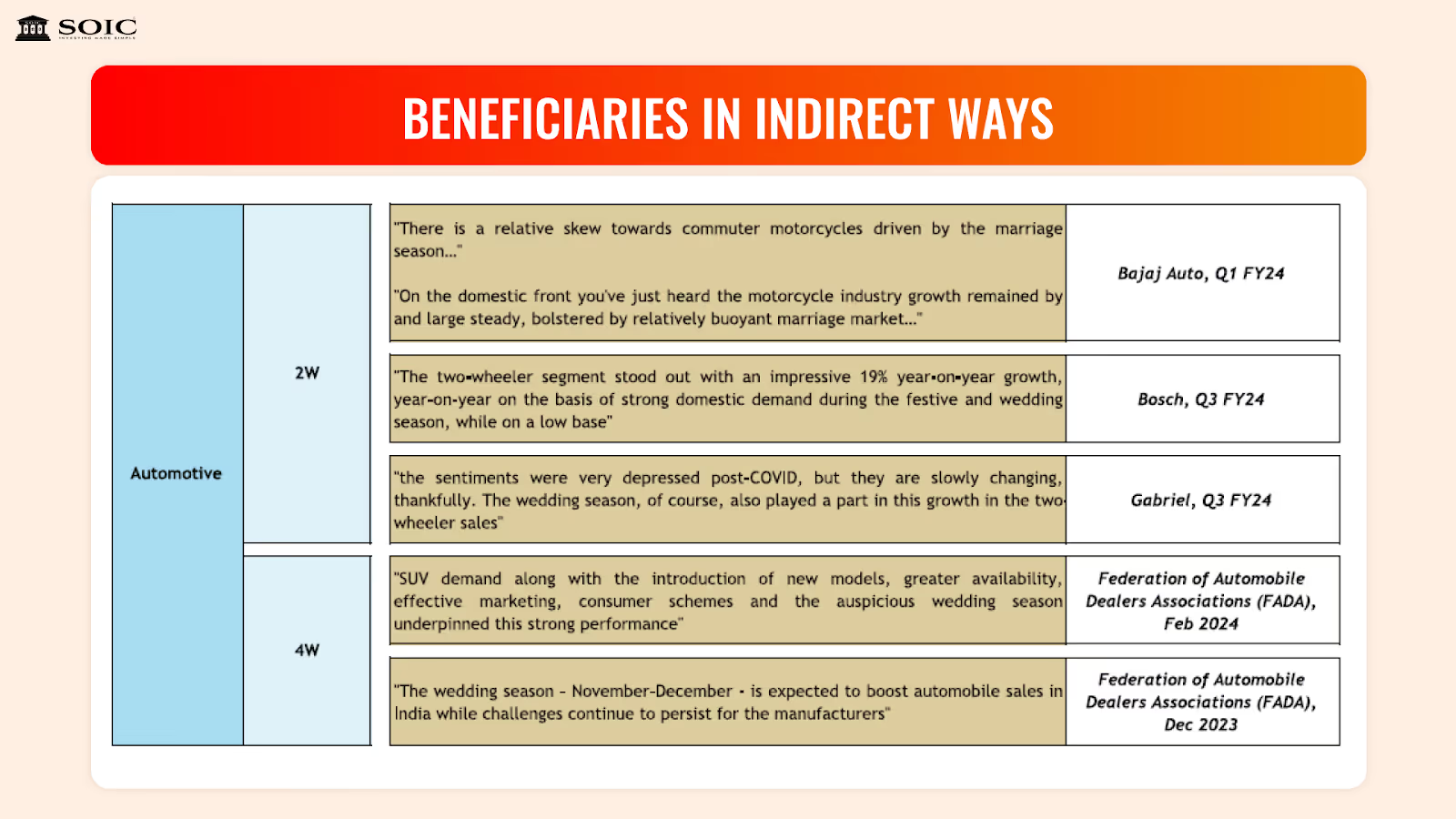

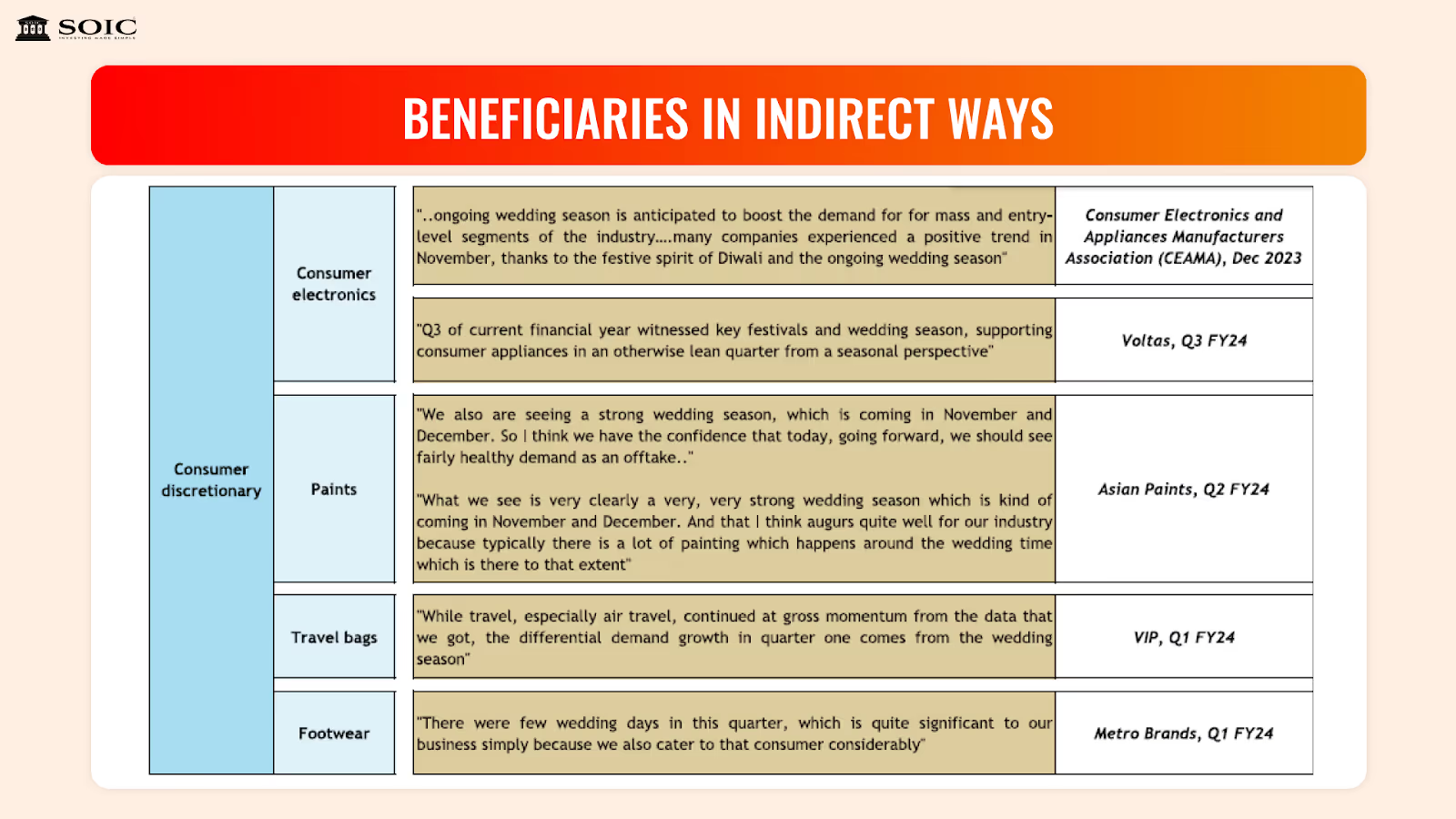

The Indian wedding industry also indirectly fuels various sectors beyond the immediate, such as jewellery, apparel, catering services, etc. Some key indirect sector beneficiaries, such as automotive and consumer discretionary, also experience an increased demand around the wedding season.

Families often purchase cars and two-wheelers not only as wedding gifts but also to accommodate growing family sizes post the wedding. Similarly, consumer electronics such as high-end televisions, smartphones, and home appliances see a surge in sales, driven by gifting traditions and the need to upgrade household amenities during and post weddings.

Additionally, home improvement sector beneficiaries such as paint manufacturers also witness a surge in demand as families invest in renovating homes. Although the exact economic impact on these sectors is challenging to quantify directly, industry players meticulously track wedding trends to align marketing strategies and inventory management.

Overall, the Indian wedding industry's economic impact is undeniable. It not only generates substantial revenue and creates employment opportunities but also plays a crucial role in driving the growth of allied sectors, contributing significantly to the nation's economic well-being.

The industry’s fragmented nature, especially in sectors like jewellery and apparel, presents opportunities for organized players to capture market share, particularly in Tier II and Tier III cities. The seasonal nature of Indian weddings, with peaks in November-December and January-July, aligns with festive periods, amplifying demand in these months.

In summary, the Indian wedding industry not only provides substantial direct and indirect employment but also continues to grow as disposable incomes rise and consumers increasingly opt for organized service providers across its various segments.

The Indian wedding industry, a tapestry of tradition, luxury, and cultural richness, is a powerhouse driving not only economic growth but also social dynamics in India. From opulent celebrations to destination weddings, the sector has rapidly evolved, embracing digital innovations and growing organized players who now shape its multi-billion-dollar landscape.

As rising incomes, celebrity influences, and government campaigns fuel the demand for unforgettable wedding experiences, the industry stands poised to continue its expansion. With 'Wed in India' initiatives and a renewed focus on luxury, India’s wedding sector remains a significant economic engine, creating jobs, supporting ancillary industries, and maintaining its unique blend of tradition and modernity. This vibrant industry, deeply woven into the cultural fabric of India, is not just about ceremonies – it is about legacy, aspirations, and an unyielding commitment to celebrating love on a grand scale.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

.avif)

0 Comments