Imagine waking up one day and realizing that everything around you—your home, roads, bridges, and even your favorite shopping mall—relies heavily on one industry: cement. It's one of those things we don't think about much, but without it, modern infrastructure wouldn't exist. The good news? The cement sector in India is on the verge of a major growth spurt, and if you’re curious about why this is happening, stick around. We’ll break it down in simple terms so you can understand why cement might just be the unsung hero of the economy in the coming years.

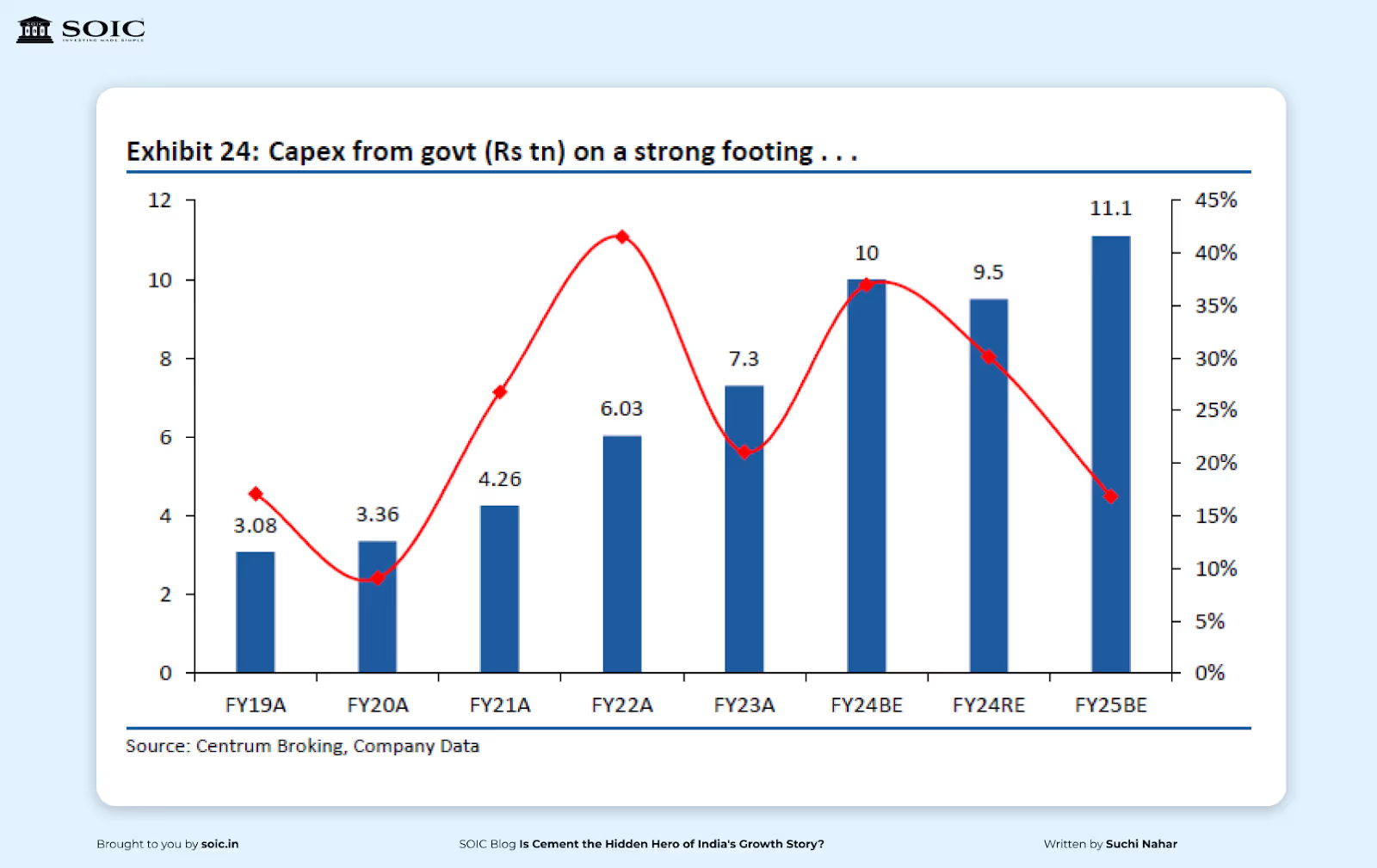

Infrastructure is a key enabler in helping India become a US $26 trillion economy. Investments in building and upgrading physical infrastructure, especially in synergy with the ease of doing business initiatives, remain pivotal to increasing efficiency and costs. Prime Minister Mr. Narendra Modi also recently reiterated that infrastructure is a crucial pillar to ensure good governance across sectors.

The Cement Manufacturers’ Association (CMA) has expressed its support for the Union Budget 2025-26, which was presented by Finance Minister Nirmala Sitharaman. The CMA commends the budget’s emphasis on infrastructure development, housing, and economic growth. It reaffirms the government's commitment to advancing rural and urban development, generating employment, and promoting sustainable investments, thereby positioning India for long-term economic resilience.

The 2025-26 Budget sets the stage for a future-ready cement industry aligned with India’s vision of ‘Viksit Bharat 2047.’ The allocation of ₹1.5 lakh crore in 50-year interest-free loans for states, along with ₹20,000 crore earmarked for innovation, is expected to accelerate advancements in green cement technology, sustainability, and digital transformation within the sector.

This budget fosters a harmonious relationship with nature, encourages infrastructure modernization, and presents opportunities for all. However, it has resulted in a scenario where larger companies in the cement industry are benefiting, while smaller firms find it increasingly difficult to survive. Currently, India’s cement industry is undergoing rapid consolidation, with smaller players either merging with larger companies or struggling to stay afloat due to aggressive pricing strategies employed by the larger firms. Despite this competitive pressure, the recent boom in infrastructure development has allowed cement volumes to remain stable.

Big cement manufacturers are expanding quickly, both inorganic and organic. Even capital expenditures are increasing despite the underutilization of current capacities due to competition for market share. The cement industry is seeing volume growth due to an increase in infra projects ahead of the elections. The industry typically sees a demand slowdown post-election.

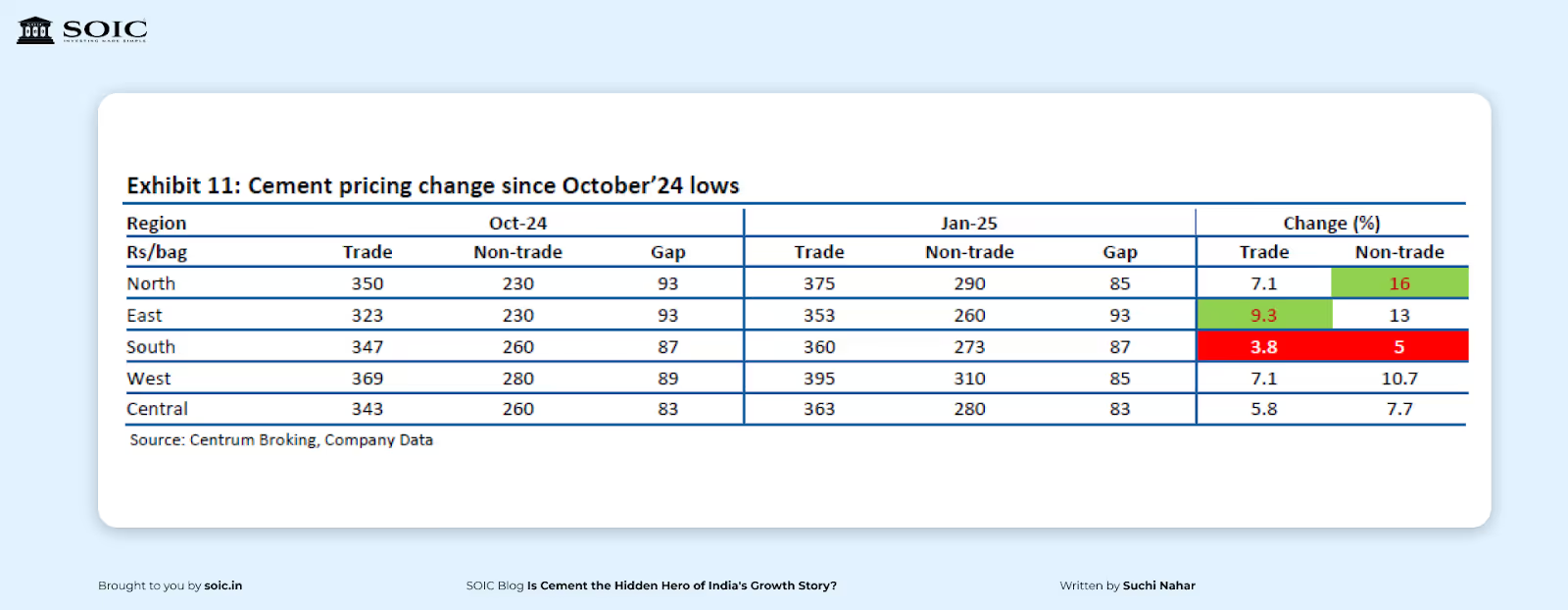

The average cement prices in India’s Trade segment rose by 6% in January 2025 compared to the lows in October 2024. Non-trade prices increased by approximately 10-15%, with the East and North regions leading the hikes, while the South has not yet seen significant changes.

Over the past three years, the gap between Trade and Non-trade prices has widened due to weak demand and increased competition, impacting overall industry realizations. Previous attempts to raise prices often resulted in rollbacks or higher discounts.

However, in the last 2-3 months, Non-trade prices have surged, suggesting a potential return of pricing power. Prices have increased by Rs. 40 per bag in the North and Rs. 30 per bag in the East, with Central and West regions seeing a rise of Rs. 20 per bag. This has narrowed the price gap between Trade and Non-trade segments from Rs. 100 to Rs. 80-90 per bag.

December has historically been weak for cement prices. Over the past decade, December has seen price hikes only twice whereas over the past six years, December has generally witnessed price declines on a MoM basis.

However, despite some improvement in prices in November 2024, December also saw decent gains, which is believed will be beneficial for better price realizations and the same also indicates a return of pricing power.

Since December 2022, fuel and freight costs—which make up almost 50% of revenue—have decreased. In Q4FY23, the price of imported coal decreased by nearly 20%, and pet coke, which was priced at over USD 200 per tonne in Q3FY23, is now less than USD 180 per tonne.

Cement manufacturers typically maintain 50-60 days of fuel inventory. A reduction in the price of coal and pet coke is anticipated to cause the average energy cost to drop by about USD 1/tonne in Q4FY23 and another USD 3/tonne in Q1FY24.

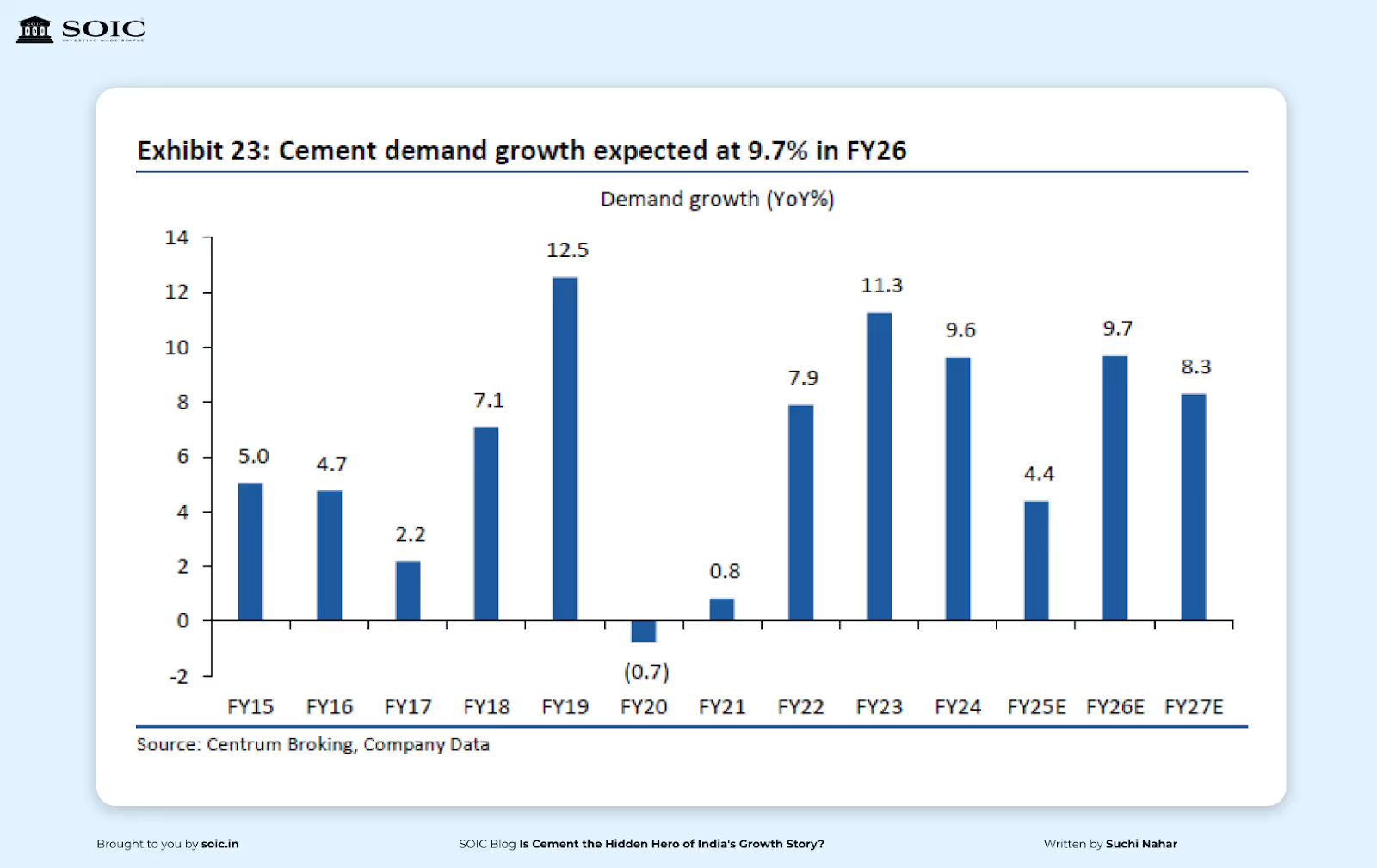

It is expected 9.7% growth in demand in FY26 on the back of higher government capex, improved rural spending, and robust urban residential construction. Demand during FY25 was impacted by general elections and lower government capex, believe that pent-up demand from both government infra and rural segment should drive strong demand growth in FY26.

Cement demand momentum has been strong post-COVID. The industry has witnessed good demand growth in the last three years. Key reasons for better demand have been:

1. Increased government spending

2. Post-COVID recovery in demand and

3. Pick-up in urban and commercial real estate markets

Rural demand is expected to be better owing to good monsoon, better reservoir levels, and increased MSP

Monsoon this year was 7.6% above its long-period average. Good monsoon has led to better reservoir levels in the country. The live storage in 155 reservoirs is at 125% of the live storage of the corresponding period of last year and 117% of normal storage levels.

The improvement in rural cash flows is backed by healthy monsoon, better kharif output and high reservoir levels, which will boost rural consumption in Q4FY25/Q1FY26, which will drive cement demand from the rural segment. Additionally, MSP for Wheat and Paddy has been increased at a healthy rate, which will further aid in increasing farm cash flows and consequently rural consumption.

Supply growth continues unabated, but clinker capacity addition is to be lower.

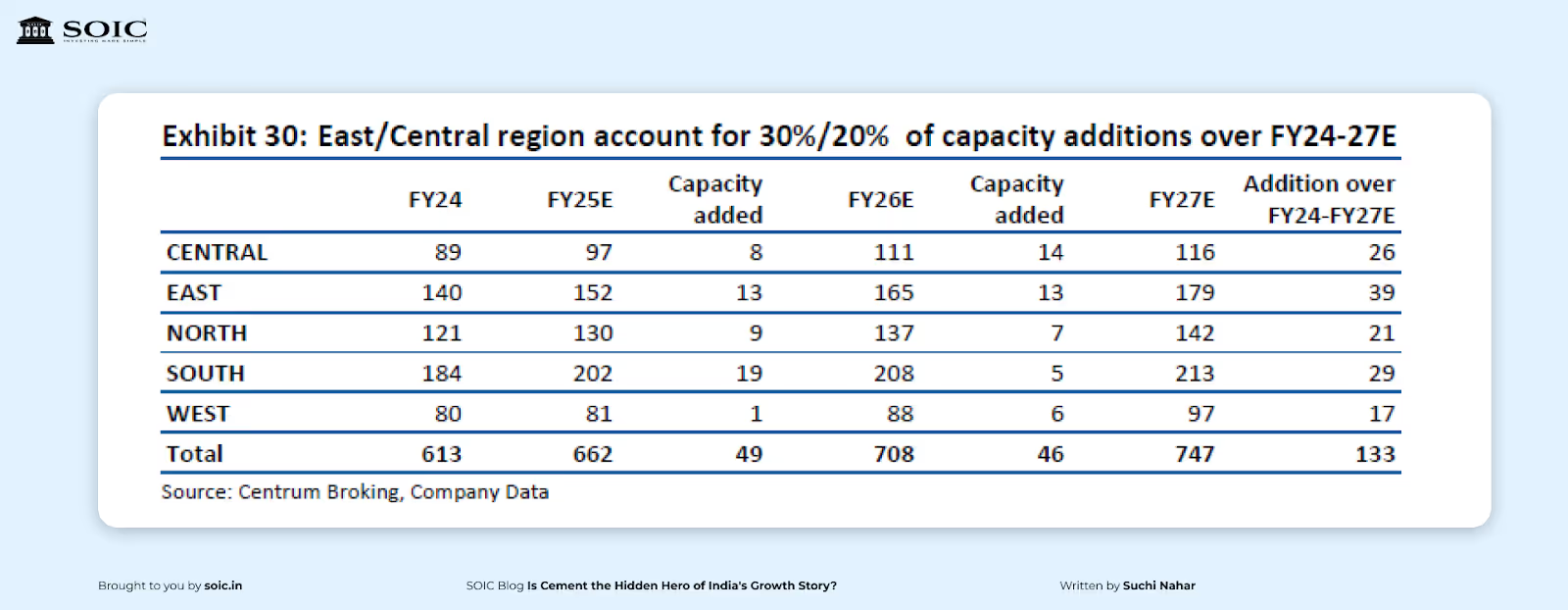

The capacity addition of 133mn mt over FY24-FY27 based on announced capex programs of cement companies. While few capacities might be delayed, overall capacity addition is likely to be higher than incremental demand. The improved medium-term demand outlook and the drive to capture greater market share have sparked a wave of capacity expansion announcements, particularly among major cement manufacturers.

Over FY24-FY27, East and Central regions are expected to add 39mn mt/26mn mt of capacity, accounting for 30%/20% of total capacity addition. The capacity additions in these regions are fuelled by better demand prospects as the per capita cement consumption in these regions is the lowest in the country.

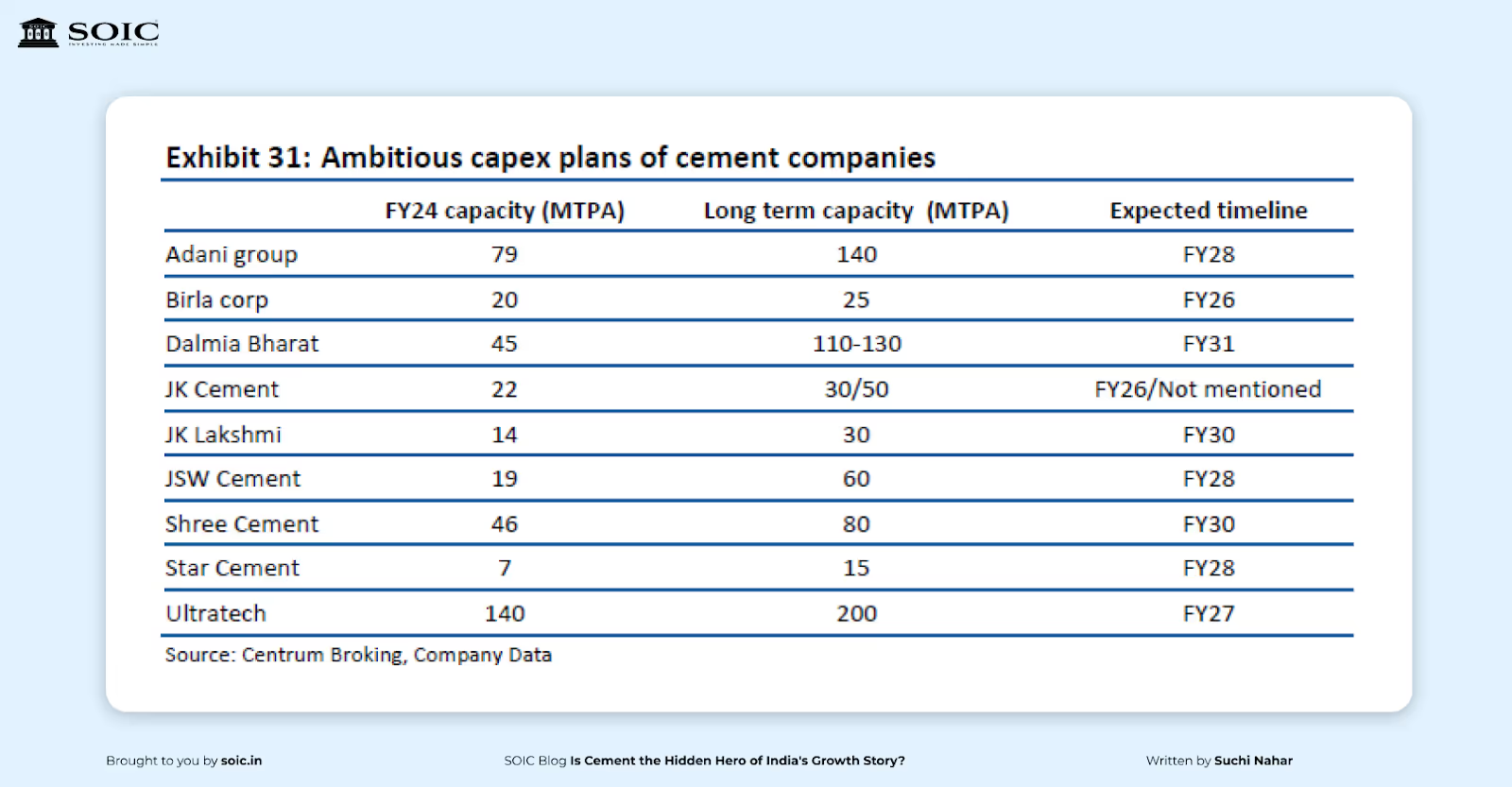

Most leading cement companies have set themselves ambitious capacity growth targets and expect to deliver better-than-industry volume growth. If that adds up all the capex targets of just the top companies in the medium to long term, Companies are looking at the addition of ~310-340mn mt capacity over the next six years.

This massive capacity expansion plan is unfolding even as the industry’s capacity utilization has stayed below 70%. From FY24 it is expected to see a capacity utilization of 69.8%, backed by an uptick in cement demand. The industry’s capacity utilization is expected to come down in the next five years as new capacities come online and demand drops.

The Adani Group, the new owners of ACC and Ambuja Cements, has unveiled plans to double the combined entities’ capacity from the current 70 MT to 140 MT over the next five years.

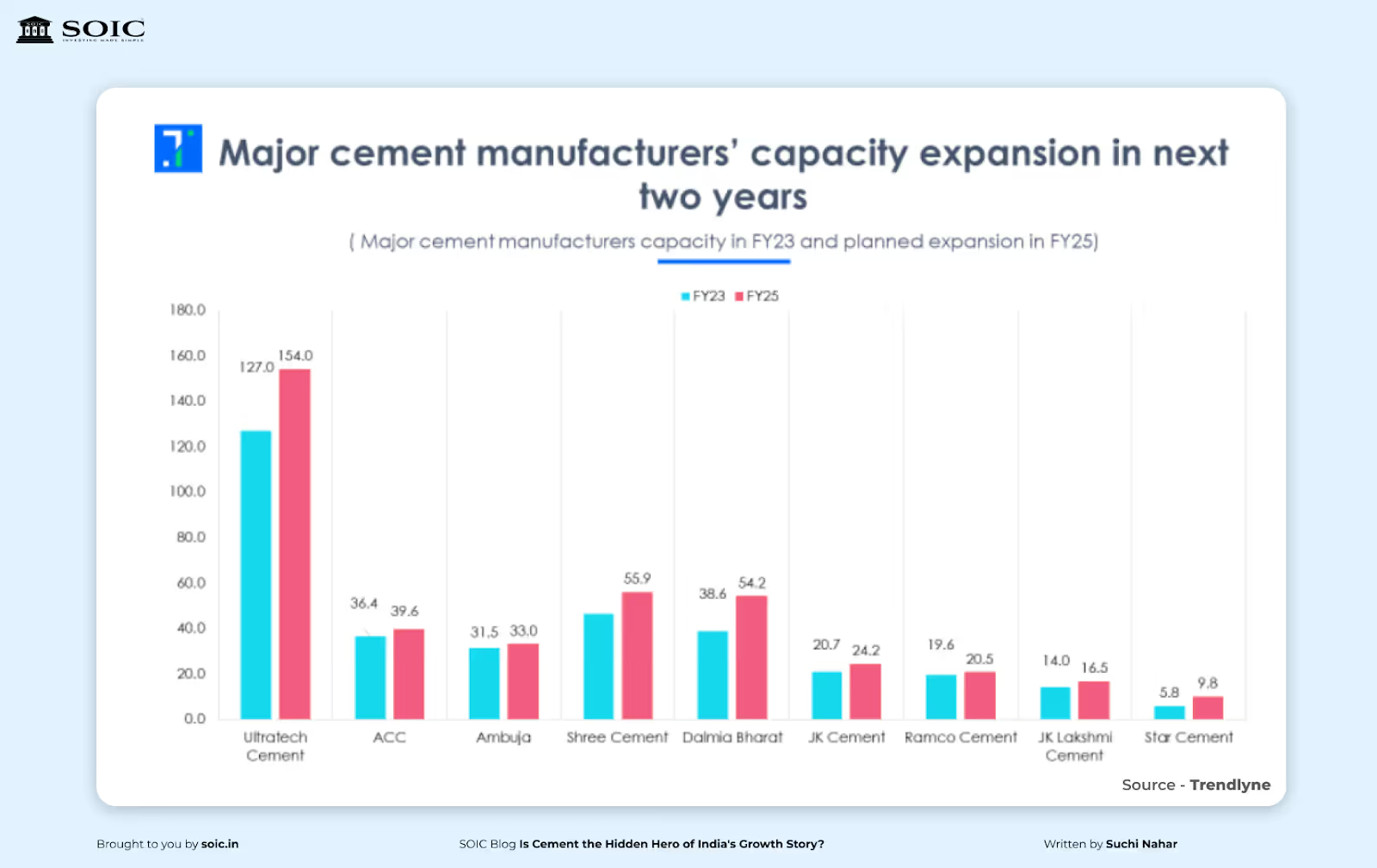

This has started a capex war among major cement manufacturers, who are now increasing their capacity by 8-10% annually for the next 2 to 3 years. As a result, the overall cement industry capacity is expected to reach 664 MT in FY25, up from the current 576 MT. However, large players are facing pricing competition from the unorganized sector, raising concerns about potential market share loss.

The cement industry is currently undergoing a consolidation phase, with Ultratech and the Adani Group vying for market dominance. Acquiring smaller players in various regions provides a more cost-effective and quicker way to scale up compared to investing in new production capacity.

Over the past two years, rising debt burdens and increased commodity costs have impacted the profitability of small and medium-sized cement companies. As a result, promoters of these companies have sold their cement assets in order to reduce debt and redirect their focus to other businesses.

A trend of market consolidation through mergers and acquisitions has been observed in the cement industry, and this pattern is likely to continue going forward. Companies are looking to take advantage of economies of scale and expand their global reach, which may lead to increased competition and innovative business practices.

Recently, the Adani Group's ACC Cements acquired Asian Concretes and Cements (ACCPL) for ₹775 crore, adding 2.8 million tonnes per annum to ACC’s production capacity. This acquisition reflects a broader industry trend where larger players are becoming increasingly dominant, pushing smaller companies towards consolidation. For instance, Ultratech Cement recently acquired Kesoram Cements in a share swap arrangement.

The acquisitions of ACC and Ambuja Cements by the Adani Group have significantly impacted the Indian cement sector. As infrastructure spending rises, financially robust new players are entering the market, particularly the Adani Group, which has shown interest in expanding further after purchasing ACC and Ambuja Cements.

The Adani Group aims to increase its capacity from the current 76.1 million tonnes per annum (MTPA) to 140 MTPA by 2030. Furthermore, the Adani Family recently invested ₹6,661 crore in Ambuja Cement, increasing their stake in the company to 66.7%. This positions Ambuja with stronger financial stability and steers its growth trajectory towards doubling its capacity to 140 MTPA by 2028. Major cement producers have also increased their budgets and capital expenditures in FY28 to protect their market share.

Adani's entry coincides with a challenging time for the sector, which is already facing intensified competition from smaller players and difficulties due to fluctuating freight and fuel prices. India continues to hold its position as the second-largest cement producer in the world.

To capture market share in the cement industry, greater production capacity is essential. Most major producers have developed ambitious long- and medium-term plans for capacity expansion. While acquisitions provide access to operational plants with established customer bases, organic growth tends to be more costly and time-consuming.

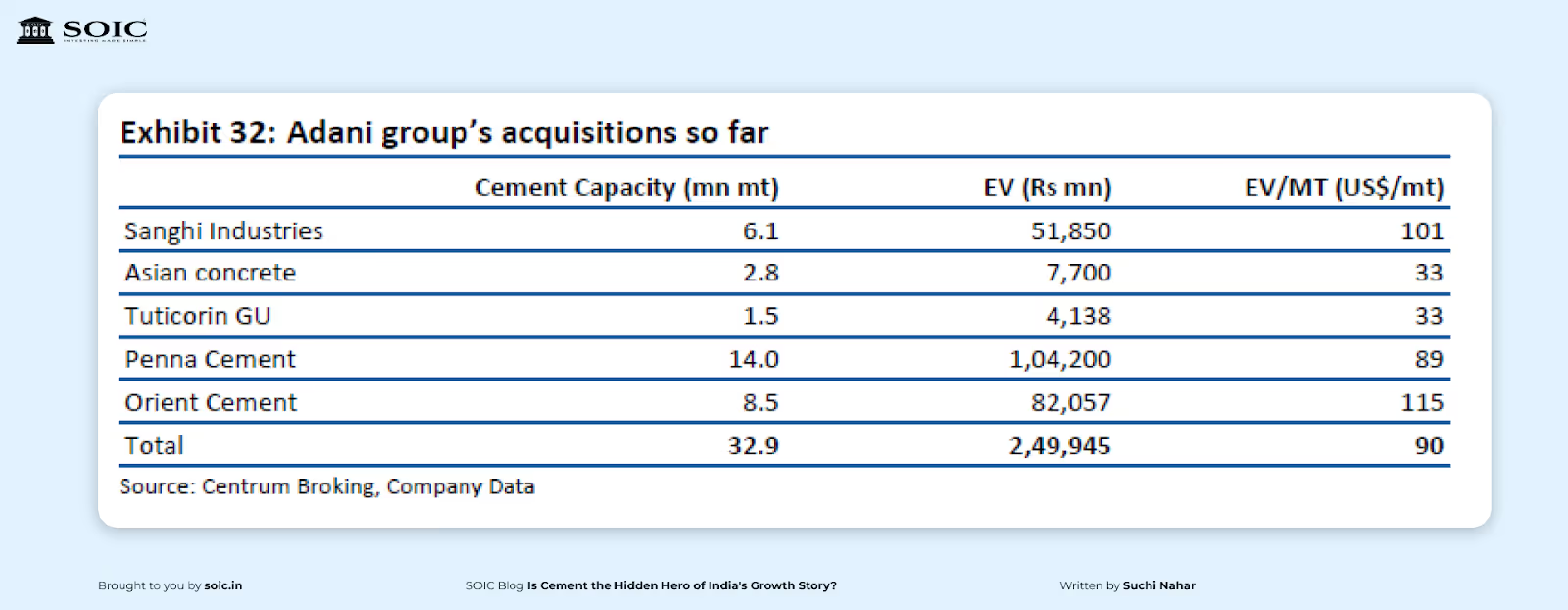

Since acquiring ACC and Ambuja, the Adani Group has set an aggressive growth trajectory, aiming to double its cement production capacity to 140 million metric tons (mt) by FY28. The company has completed five acquisitions, which have increased its capacity by 33 million mt at a cost of USD 90 per metric ton. With the recent acquisitions of Penna and Orient Cement, Adani's share of the South Indian market has risen from approximately 14% to 25%. Ambuja is on track to achieve a capacity of 100 million mt by FY25, bringing it closer to the overall target of 140 million mt.

While the Adani group has been on an acquisition spree to double its capacity to 140 mn mt, Ultratech has also seized certain opportunities and is moving closer to its capacity target of 200mn mt.

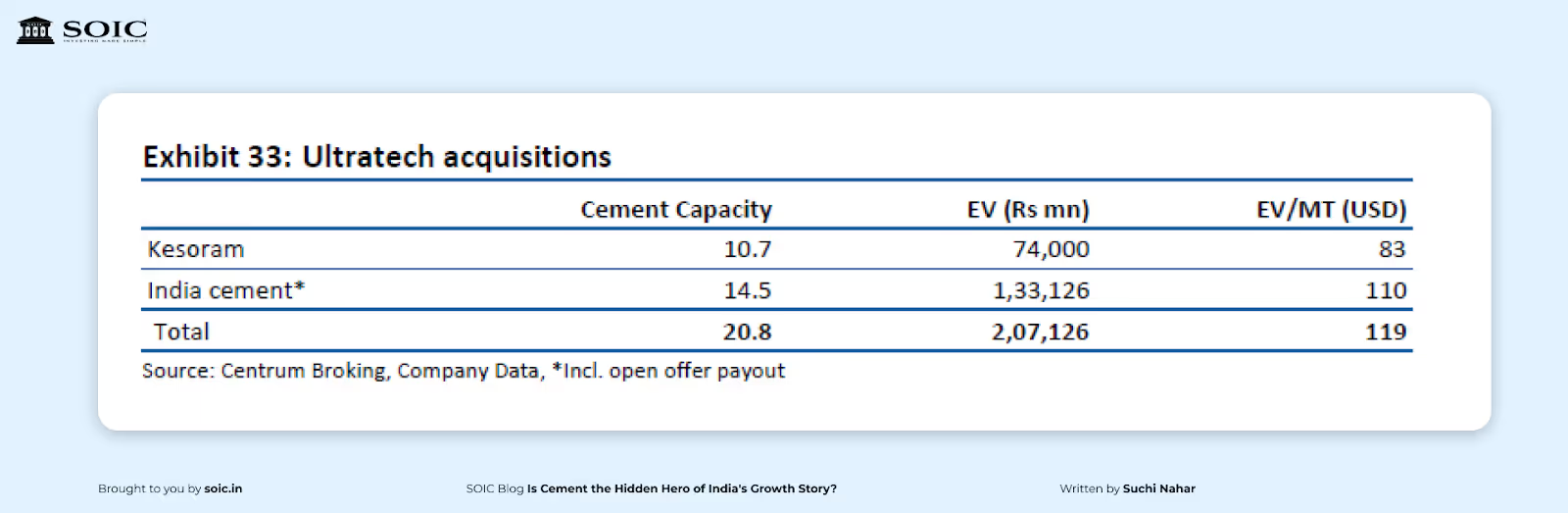

In Dec '23, Ultratech acquired Kesoram Industries through a share swap deal at EV of Rs74bn (USD83/mt), which provided them with assets in the South region, especially Telangana where they did not have much presence. After Ambuja’s acquisition of Penna Cements, Ultratech responded by acquiring a non-controlling stake in India Cements at EV/mt of USD88/mt and consequently buying another 32.72% stake from the promoters in July 2024 for Rs. 39.54bn.

After the acquisition of Kesoram and India Cements, Ultatech will have a capacity share of ~23% in the South region as against 13% now. Additionally, it has also acquired a non-controlling stake in Star Cements Ltd.

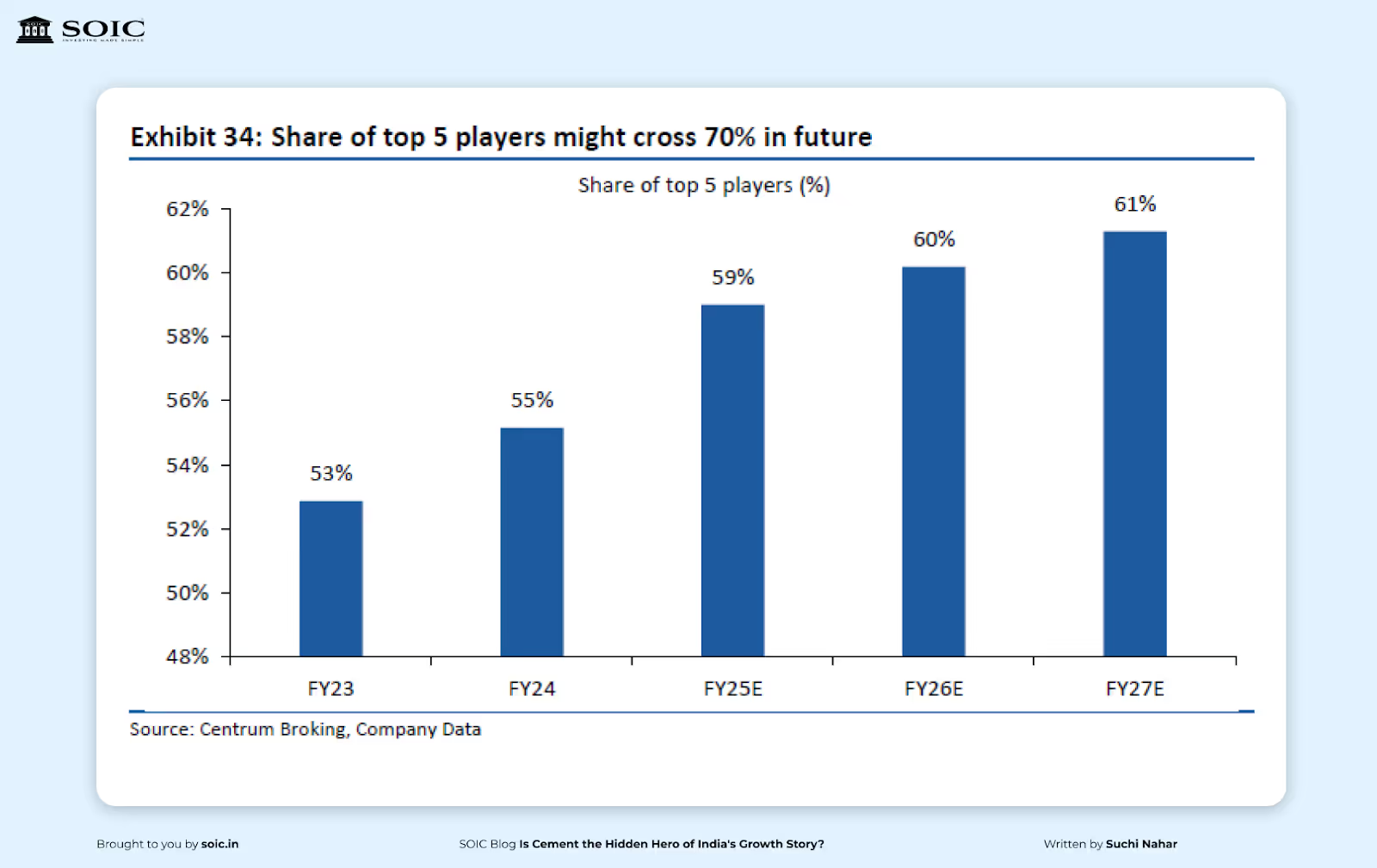

The capacity share of top 5 players is expected to increase from 53% in FY23 to 61% in FY27E. Consolidation has largely taken place in the South region, with the leaders increasing their capacity share, which is quite fragmented. Better balance sheet strength has enabled the top players to grow their market share inorganically through internal accruals.

The share of top 5 players in South India stood at 8% in FY23 and the same is expected to rise to 14% by the end of FY25 when the acquired capacities come on stream following the regulatory approvals. It is expected to have a few more deals in the Cement sector over the next 12-18 months, which will eventually take the share of top 5 players above 70%.

The Indian government’s 2025 budget has allocated a significant increase in infrastructure spending, directly benefiting the cement industry. Key highlights include:

The cement industry is expected to grow by 9-10% in FY26, supported by a combination of pent-up demand, government spending, and rural housing growth. Key factors driving this demand include:

India currently has the fifth-largest metro network in the world and will soon overtake advanced economies such as Japan and South Korea to become the third-largest network. Metro rail network reached 810 km and is operational in 20 cities as of September 2022.

At almost 20 km, the Mumbai monorail is the third largest route in the world after China with 98 km and Japan with 28 km. India plans to spend US$ 1.4 trillion on infrastructure through the ‘National Infrastructure Pipeline’ in the next five years.

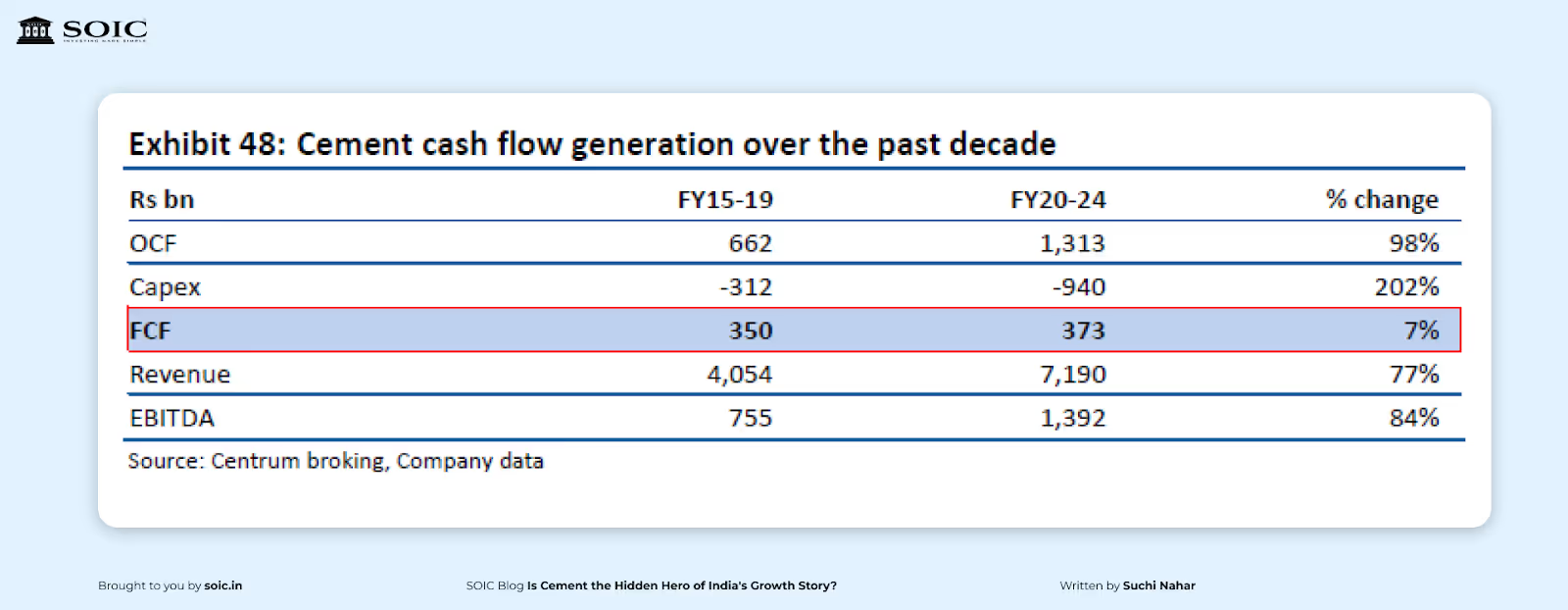

Over the past five years, improved balance sheet health (driven by reduced leverage and stronger operating cash flow) has fuelled ambitious expansion plans among most cement companies. There has been a notable shift in the managements' approach to capacity expansion, influenced both by optimistic demand projections as well as enhanced cash flows. The cash flow analysis of the cement sector for the past decade reveals a substantial increase in operating cash flow and capex intensity during the last five years compared to the earlier period from FY15-FY18.

In the first five years of the decade (FY15-FY19), the industry generated Rs662bn OCF and did a capex of Rs312bn. In the next five years (FY20-FY24), the industry generated Rs 1,313bn of OCF and spent Rs940bn on capex. The capex intensity increased ~3x compared to ~2x increase in OCF in the 2nd half of the decade, which resulted in FCF increase of just 7%. The higher FCF generation in the past is currently fuelling the next capex cycle in the industry.

While the outlook is largely positive, risks to this growth trajectory include:

The Indian cement sector is at the cusp of a strong growth cycle, driven by improved demand, pricing power, and industry consolidation. The Indian cement industry is witnessing significant transformation fueled by infrastructure spending and market consolidation. Despite challenges, including pricing pressures and rising costs, opportunities abound for growth.

By embracing innovation and strategic planning, cement manufacturers can navigate these dynamics to secure their market share and contribute to the nation's development goals.

With government-led infrastructure spending, increased rural and urban housing demand, and stable operating costs, the sector is poised for a significant upswing. Investors and stakeholders should closely track market dynamics to capitalize on this promising phase.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference

.avif)

0 Comments