The Sparkle Revolution: How Lab-Grown Diamonds Are Redefining Luxury and the Industry

BY

Shuchi Nahar

Consumer Goods

Consumer Trends

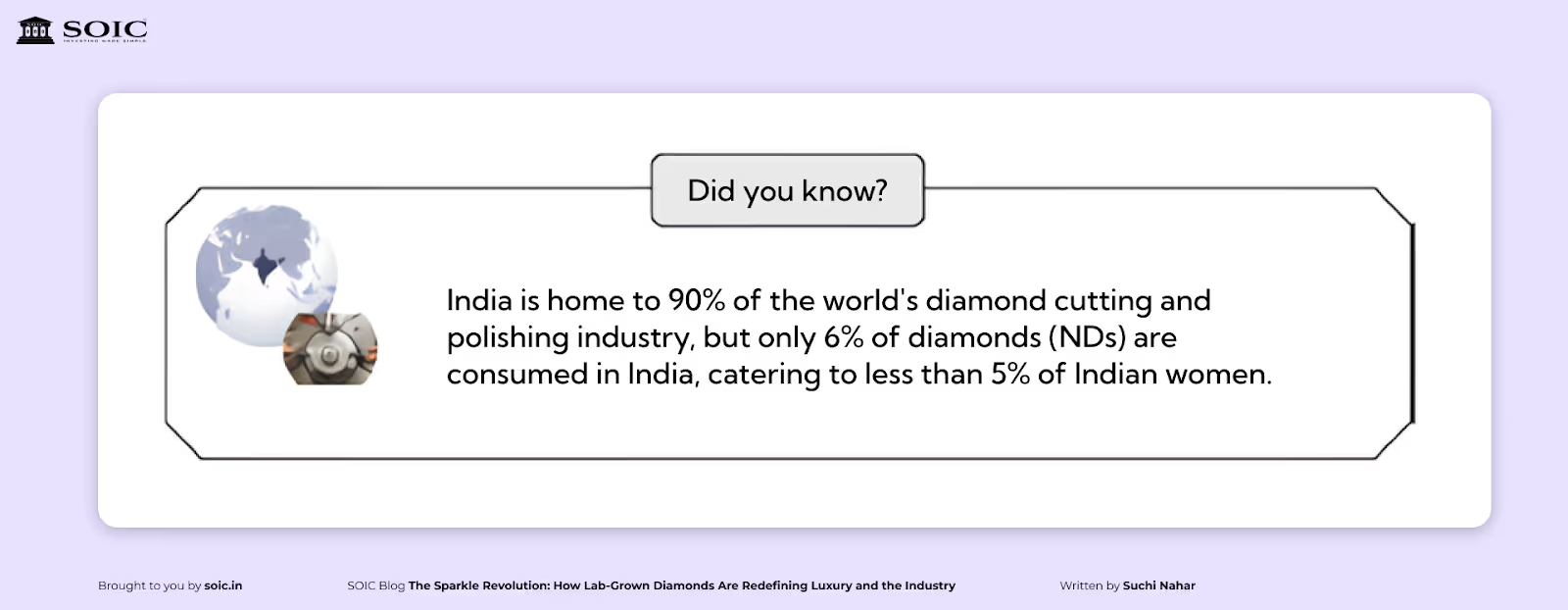

Very closely related to a city that is famously called the Diamond Hub of India (Surat), a place where sparkling gems aren’t just stones but a way of life. Over the years, I’ve witnessed a fascinating shift—one that still amazes me every time I hear about it. The transition from natural diamonds to lab-grown diamonds (LGDs) isn’t just an industry trend; it’s a cultural movement.

Talking to friends whose families have been in the diamond trade for generations, I hear firsthand how Millennials and Gen Z are rewriting the rules of luxury. What was once a distant dream—the solitaire engagement ring or that dazzling diamond necklace—is now within reach, thanks to LGDs. And let’s be honest, it’s a win-win for both men and women. Women get more variety, better clarity, and a guilt-free sparkle, while men? Well, they don’t have to empty their life savings to propose anymore (finally, a sigh of relief! 😆).

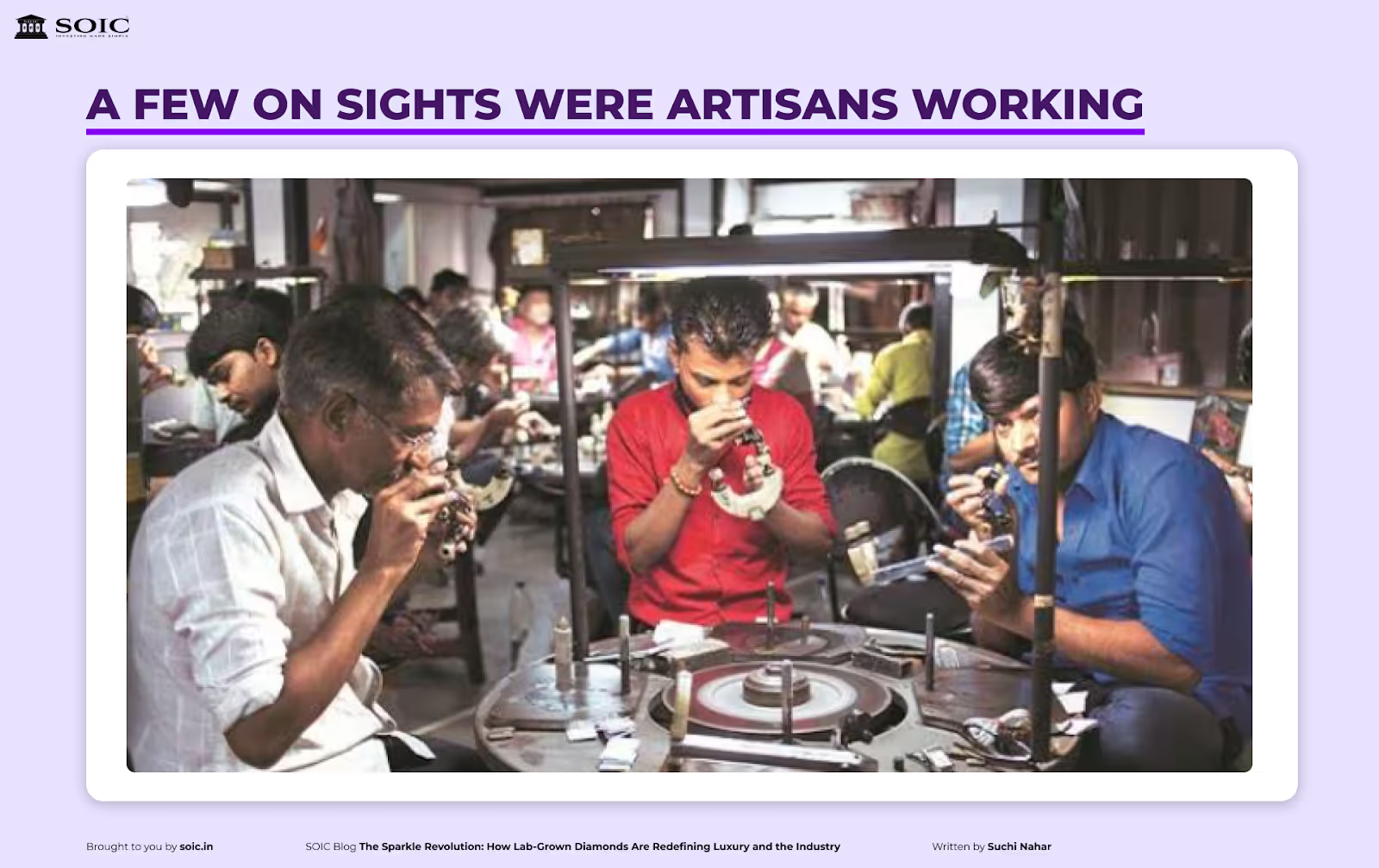

But beyond the glamour and affordability, there’s a world few get to see—the silent hum of thousands of machines, the steady rhythm of workers polishing each diamond with precision, and the unseen effort that transforms carbon into brilliance. It’s a world where thousands toil amidst hazardous chemicals, extreme temperatures, and endless hours of craftsmanship, all to bring us that one perfect stone.

The shift to lab-grown diamonds is not just about cost or sustainability—it’s a revolution. And today, we’re diving deep into how this transformation is reshaping the diamond industry forever. Ready to explore? Let’s go!

Understanding the Lab-Grown Diamond (LGD) Value Chain in Detail

The process of manufacturing lab-grown diamonds is highly scientific but results in diamonds that are identical to natural ones. The value chain consists of several key stages:

a) Seed Creation and Sourcing

The process begins with a diamond seed, a tiny slice of natural or lab-grown diamond.

Currently, India sources seeds from Japan, Israel, and the US, but there is an increasing focus on local seed production.

b) Growth Process: HPHT vs. CVD

Lab-grown diamonds are produced using two main methods:

Chemical Vapor Deposition (CVD) – A more advanced method, where carbon atoms bond to a seed layer, growing a diamond one atom at a time.

c) Cutting, Polishing, and Certification

After growth, LGDs undergo the same cutting and polishing processes as natural diamonds.

They are graded and certified by institutions like GIA and IGI, ensuring quality.

d) Jewelry Manufacturing & Retail

The final step involves setting LGDs into jewelry and distributing them through retail and e-commerce channels.

Why India is Becoming a Global Leader in Lab-Grown Diamonds

India is already the largest processor of natural diamonds, but now it's rapidly gaining dominance in LGD production. Here’s why:

a) Government Support & Policy Tailwinds

The Indian government removed the 5% import duty on LGD seeds, reducing costs.

The PLI Scheme for Gems & Jewellery is encouraging domestic production.

The US-China trade war has led to more global retailers sourcing from India.

b) Cost and Skill Advantage

India has skilled artisans with expertise in diamond cutting and Jewellery design.

Labor costs are 60-70% lower compared to Western markets.

c) Expanding Global Demand for Sustainable Diamonds

Lab-grown diamonds are 60-70% cheaper than mined diamonds, making them affordable for younger buyers.

US retailers like Signet, Tiffany, and Pandora are shifting to LGDs to meet sustainability goals.

d) India’s E-Commerce Boom

Brands are bypassing wholesalers and going direct-to-consumer (D2C) via platforms like Tata CLiQ, CaratLane, and Bluestone.

E-commerce allows faster inventory turnover and better cash flow, benefiting companies like Goldiam International.

Industry Hurdles: Navigating the Challenges Ahead

Despite rapid growth, the LGD industry faces some challenges:

Price Volatility: LGD prices have declined due to increasing supply.

Consumer Awareness: Many still prefer natural diamonds for sentimental value.

Competition from China: China is a major LGD producer, but India's branding as a luxury supplier helps counter this.

Goldiam International: A Leading Indian Player in Lab-Grown Diamonds

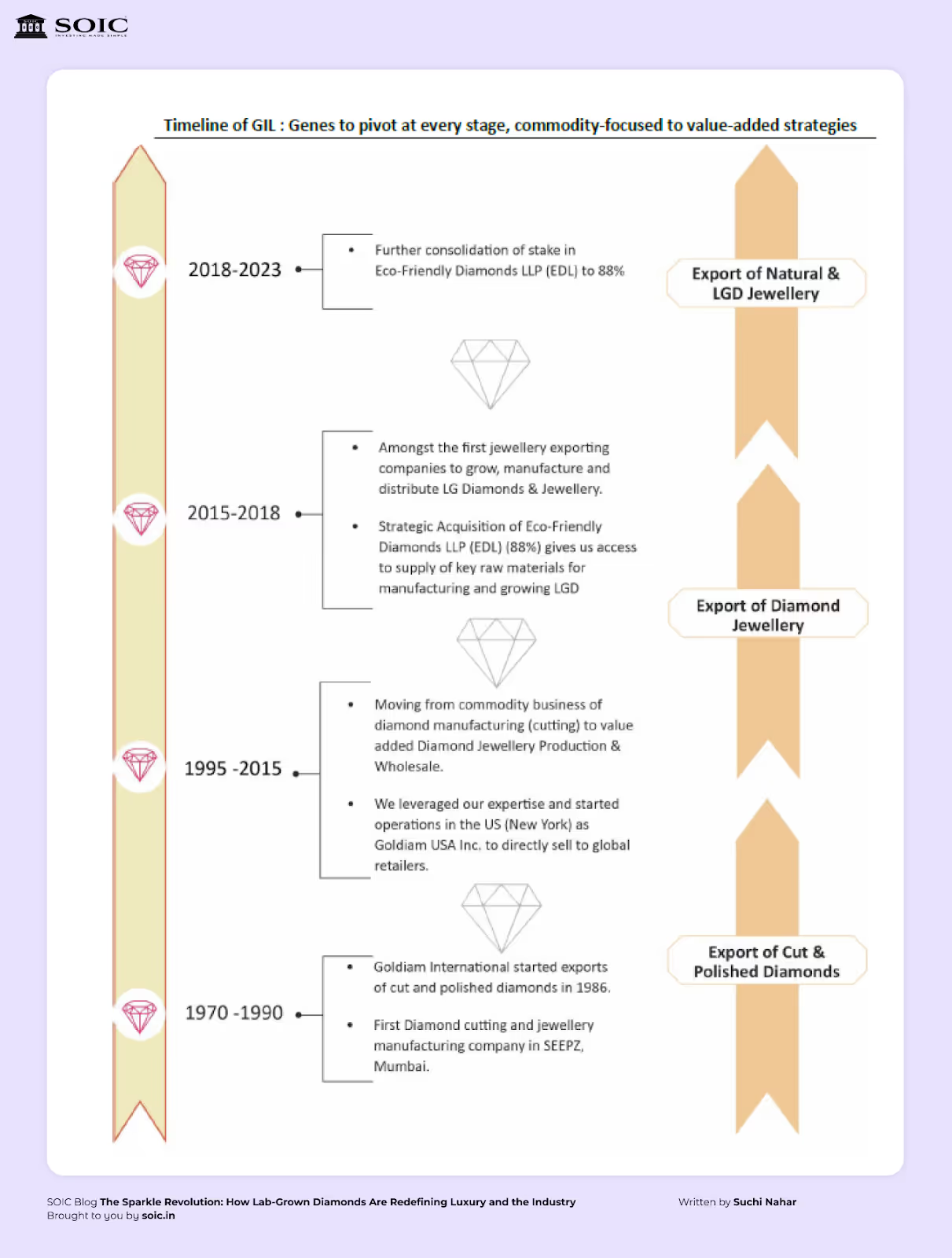

Goldiam International Ltd is a pioneer in India's LGD industry, integrating diamond manufacturing, jewelry production, and e-commerce distribution. Goldiam International Ltd, established in 1986, specializes in manufacturing and exporting diamond-studded gold and silver jewelry. The company's product range includes engagement rings, wedding bands, anniversary rings, bridal sets, earrings, and pendants.

Goldiam has been transitioning from a focus on natural diamonds to becoming a major supplier of lab-grown diamond jewelry, adopting an omnichannel sales strategy. The company serves retailers, departmental stores, and wholesalers across American and European markets, with exports primarily to the United States, Europe, and other countries.

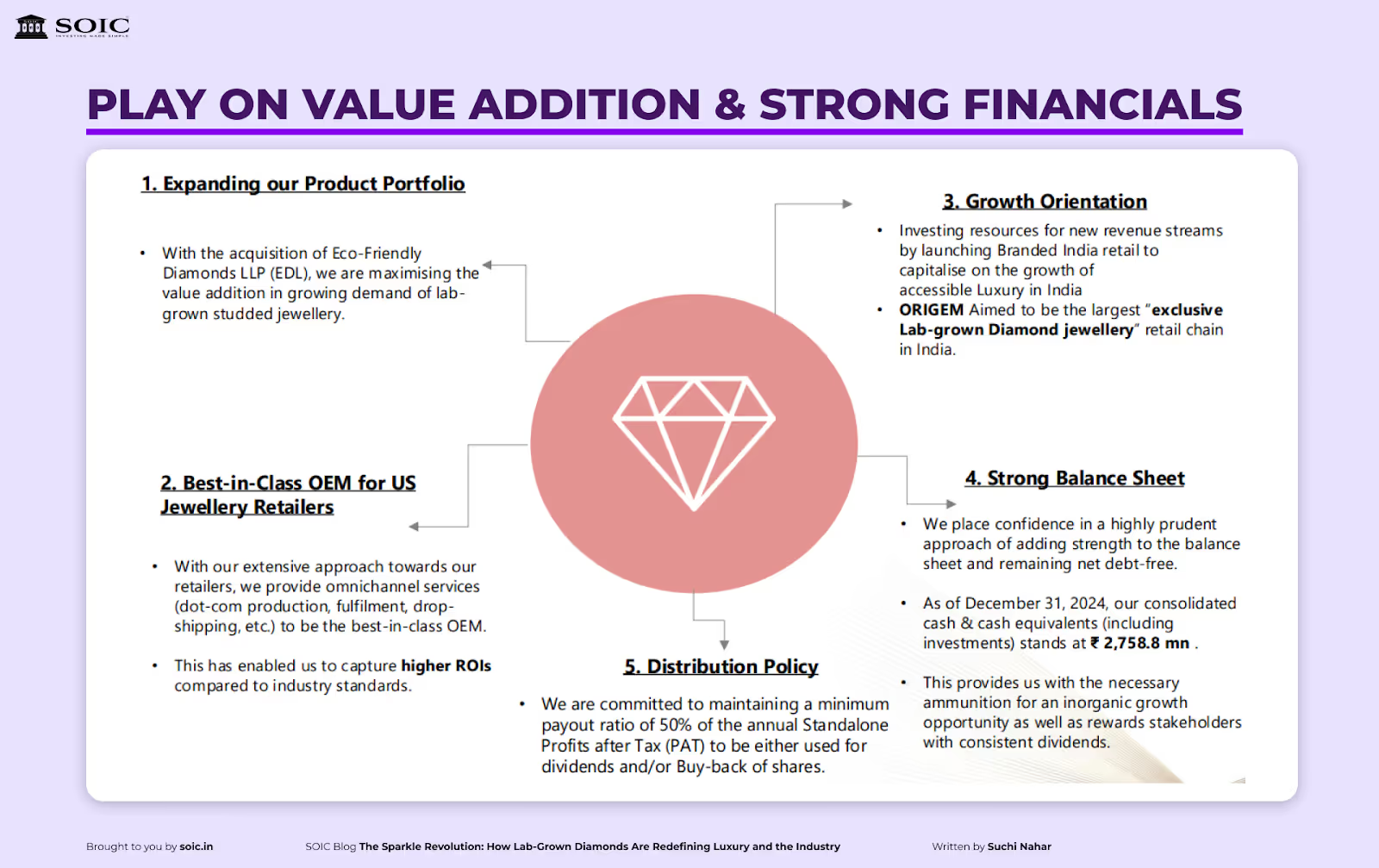

Goldiam's subsidiaries include Goldiam Jewellery Limited, Diagold Designs Limited, Eco-Friendly Diamonds LLP, and Goldiam USA, Inc.

The company underwent a transformation from being an exporter of cut and polished diamonds in the 1990s to becoming a value-added jewelry manufacturer for both NDs and LGDS. Currently, the company is moving forward by integrating into retail stores under its own brand.

Growth Comparison: Natural vs. Lab-Grown Diamonds (LGD)

LGD Contribution to Revenue: Earlier (Pre-FY22): ~10% of revenue FY23: ~40% of revenue

FY24: ~80% of revenue (indicating a major strategic shift) Natural Diamond Contribution: Steadily declining as LGD adoption increases.

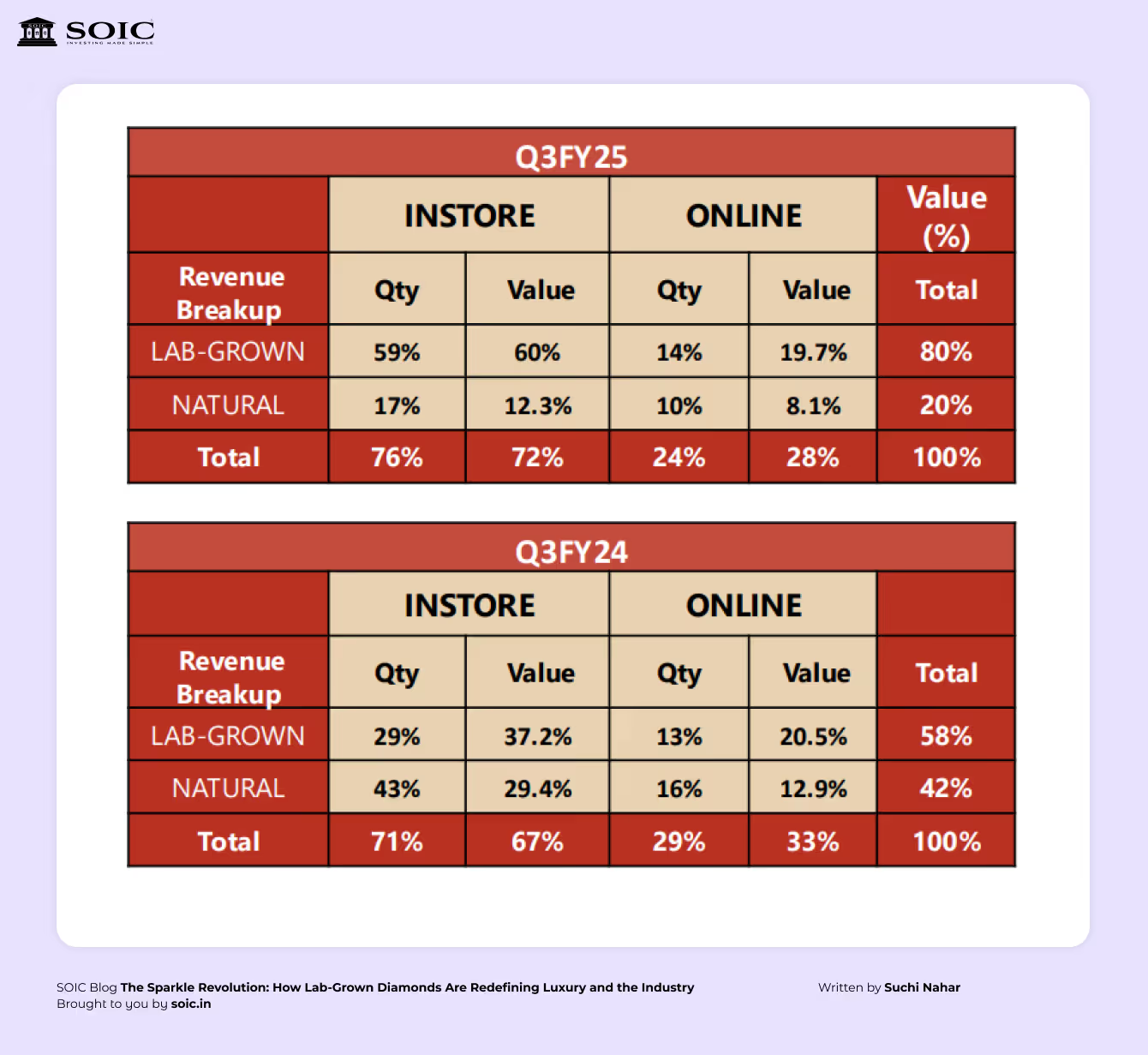

Goldiam has undergone a significant transformation, shifting from a traditional in-store jewelry retailer of natural diamonds to a leading supplier of lab-grown diamond jewelry, supported by an omnichannel sales strategy.

In the third quarter of FY25, the share of lab-grown diamond jewelry in export revenue reached 80%, compared to 58% in the same quarter of FY24. Additionally, online sales accounted for 28% of total sales in Q3 FY25.

a) Business Model & Growth Strategy

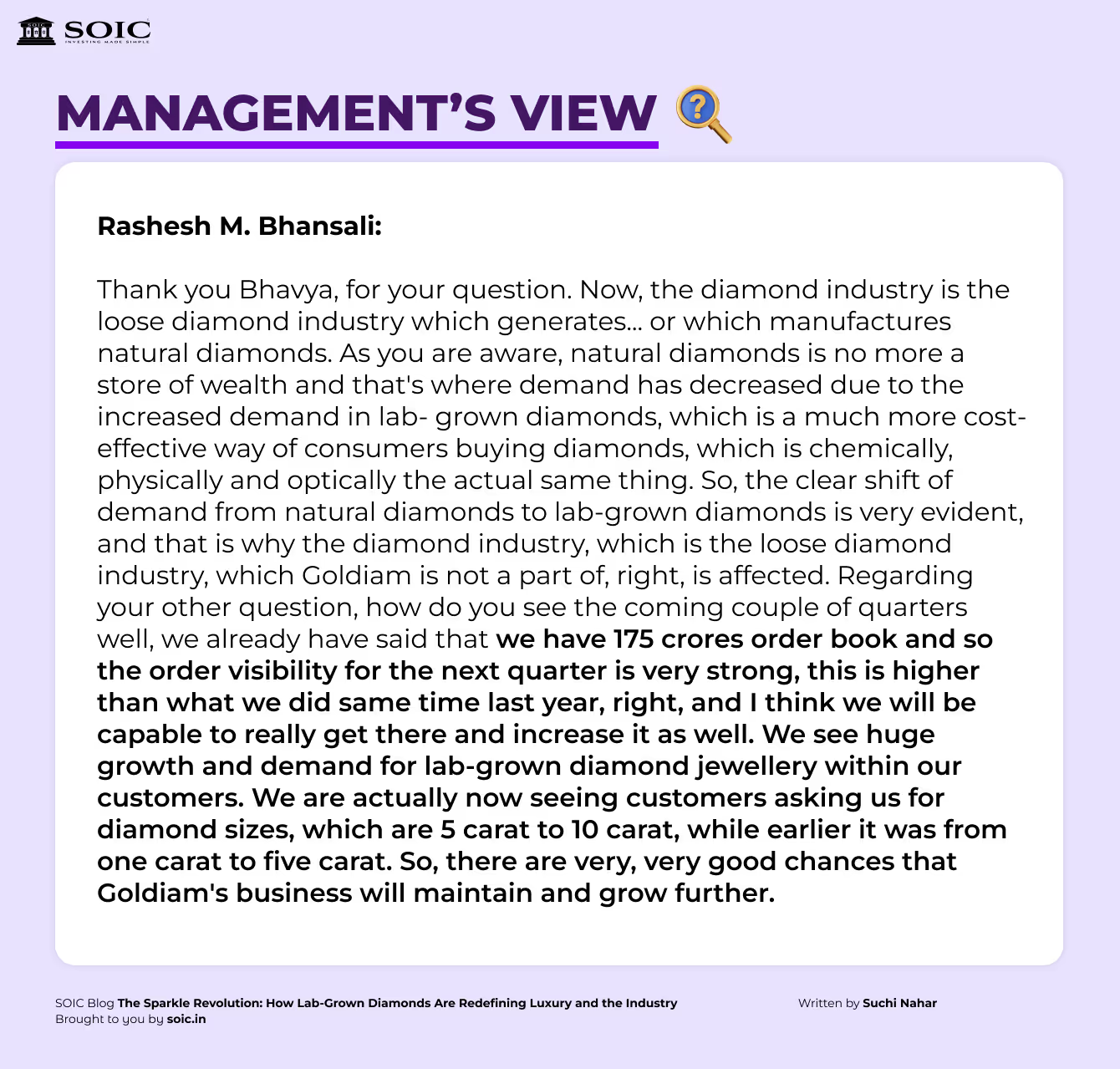

Goldiam is capitalizing on the rising demand for lab-grown diamonds (LGD) by implementing an aggressive expansion strategy. The company’s initial goal is to establish 25 company-owned and operated (COCO) stores within the next two - three years, prioritizing prime locations. Subsequently, it plans to transition into a franchise model.

Key Expansion Highlights:

First COCO stores to open in NCR and Bangalore within the next six months.

Targeting a total of 150 stores in three years.

Focus on premium trajectory, avoiding fast fashion.

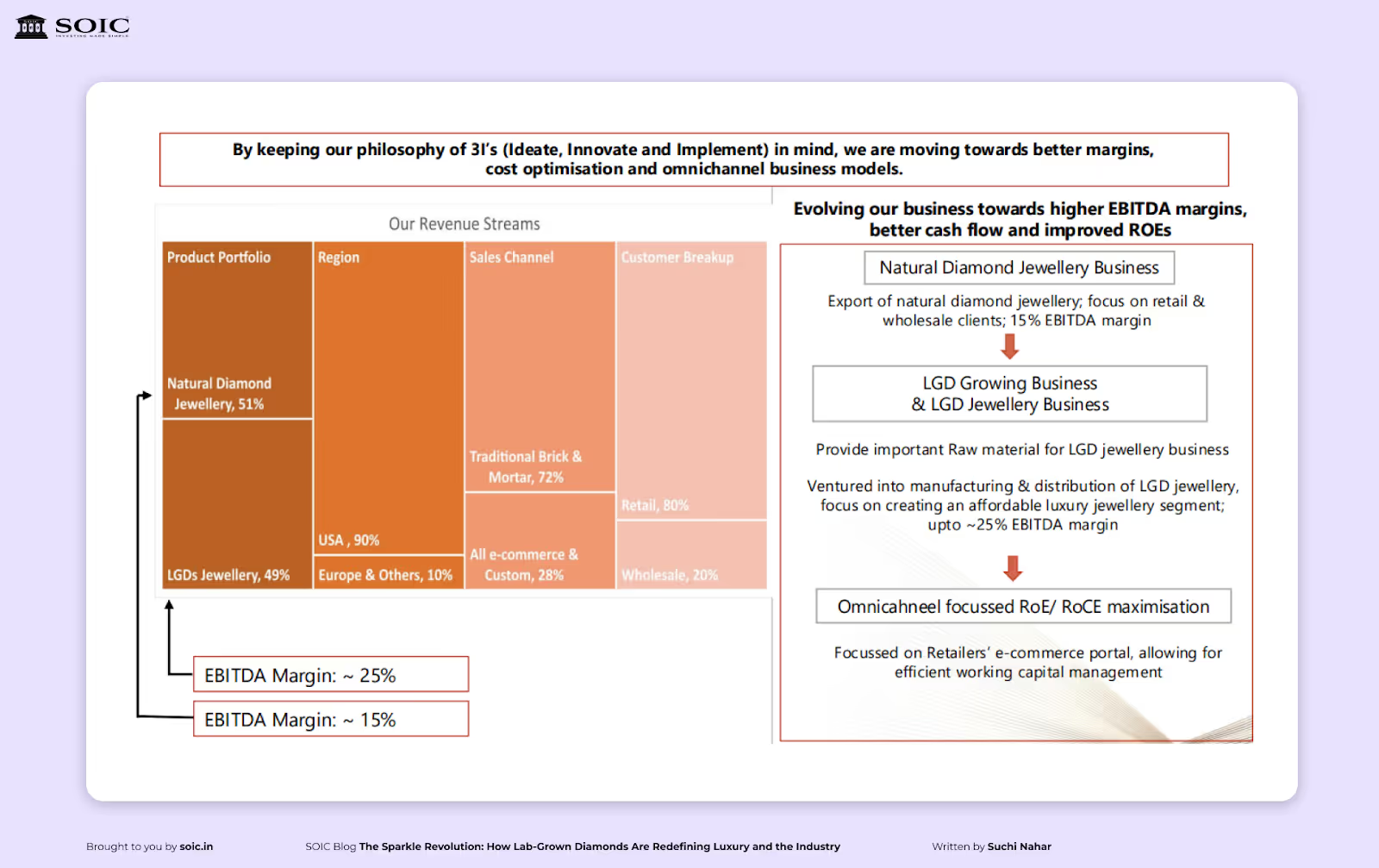

Around 70-80% of revenue comes from natural diamonds, but LGD has now started contributing 30-40% of total revenue (up from 0% five years ago).

LGDs are expected to be 50% of the company’s total business.

Lab-Grown Diamonds (LGD) Dominance - Goldiam has transitioned significantly toward lab-grown diamonds, which now constitute 80% of its total exports. This strategic shift has helped counter the declining demand for natural diamonds.

B2B Focus - The company supplies jewelry to large corporate retailers in the U.S., working on consignment and wholesale models. It also has a strong presence in mom-and-pop stores through distribution partners.

Indian Retail Expansion - Goldiam launched ORIGEM, a B2C lab-grown diamond jewelry brand, aiming to capture a substantial share of India’s growing fine jewelry market.

b) E-Commerce Disruption: Direct-to-Consumer (D2C) Model

Goldiam has seen a pivotal shift in online sales post-COVID-19, with U.S. customer behavior increasingly favoring online jewellery purchases. The company benefits from rapid payment cycles:

E-commerce realization: Money is received within 7-30 days. Goldiam’s shift to e-commerce (Amazon, Walmart, and JewelFleet platform) has reduced its working capital cycle to 10-30 days.

Traditionally, diamond businesses have long credit cycles (120-150 days).

E-commerce now accounts for 20% of total sales and is expected to grow further.

E-commerce Integration - The company has invested in a dedicated online presence (www.origemindia.com), leveraging omnichannel strategies to drive both online and offline sales. Goldiam is an OEM supplier to major US retailers, including Signet Group and JCPenney.

Online Revenue Contribution - 28% of Q3 revenue came from e-commerce, highlighting its significance in the company’s sales mix.

Fast Order Fulfillment - The company’s quick time-to-market capabilities and inventory efficiency allow for better stock rotation and minimal holding costs.

Customization and Made-to-Order Services - ORIGEM has seen a significant demand for personalized jewellery, with strong consumer interest in bespoke designs.

Omnichannel Approach - Goldiam ensures seamless integration between online browsing and offline store visits, mirroring successful digital-first jewellery brands.

c) Financial Strength & Valuation

Debt-free balance sheet and a strong cash position of ₹2.7 billion.

Revenue Growth: Consolidated revenue stood at ₹2,880 million, reflecting a 41% YoY growth and 104% QoQ increase.

EBITDA Surge: EBITDA grew by 62% YoY, with margins reaching an all-time high of 24.6%. EBITDA margins in LGDs are 30-40%, compared to 18-20% for natural diamonds.

Profitability: Net profit after tax stood at ₹498 million, a 54% YoY rise.

Cash Reserves: The company maintains strong liquidity with ₹2,759 million in cash and investments.

Dividend Policy: The board declared a second interim dividend of ₹1 per equity share, indicating robust shareholder returns. Consistent dividends and buybacks (50% of standalone PAT is returned to shareholders).

Profitability & Margins: EBITDA: ₹710 million (+62% YoY), 24.6% EBITDA margin (record high) Net Profit: ₹498 million (+54% YoY)

Balance Sheet Strength: Net Cash Company: ₹2,759 million in cash & investments No significant debt, ensuring financial flexibility.

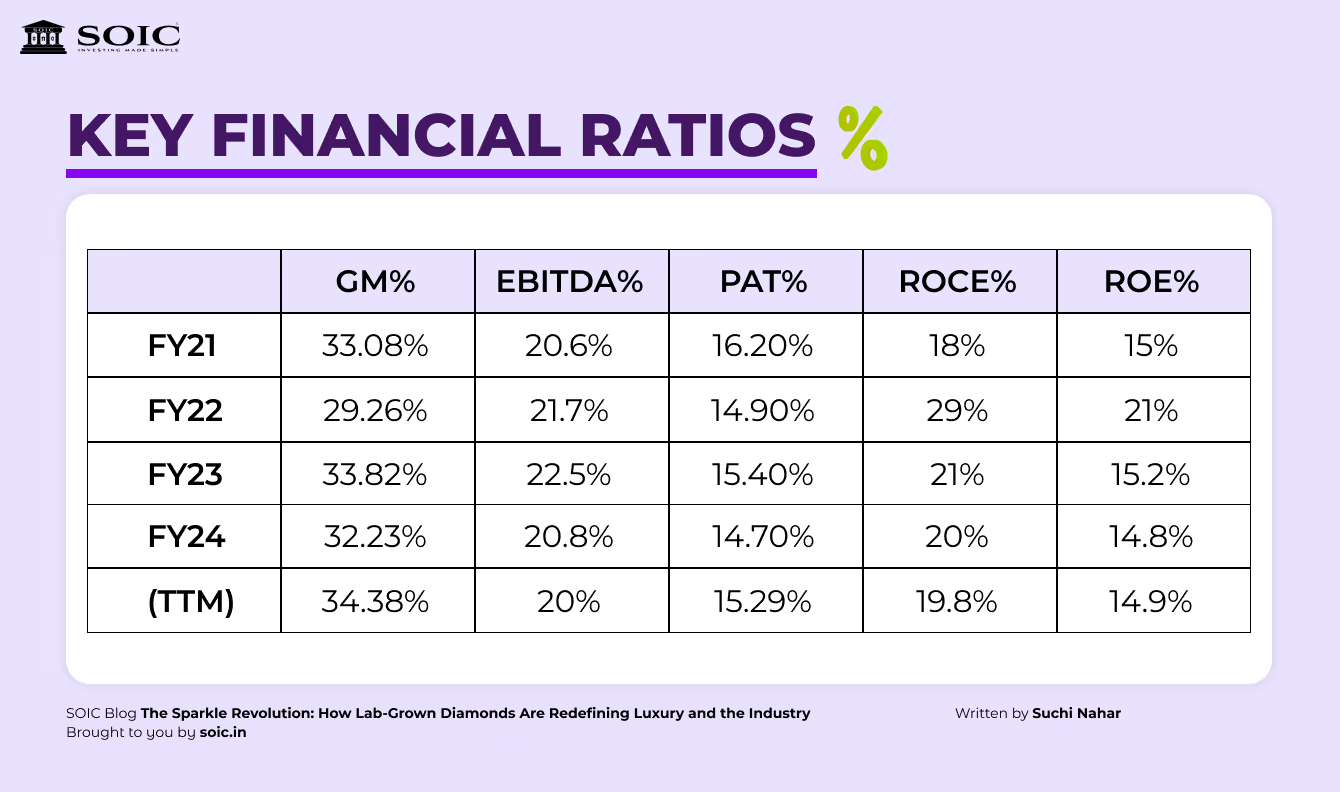

Key Financial Ratios:

Share Buybacks and Net Cash Position

Share Buybacks: The company has engaged in share buyback programs, reducing the equity share capital from ₹21.79 crore in March 2023 to ₹21.36 crore in March 2024, indicating a strategy to enhance shareholder value.

Net Cash Position: With substantial cash and investments totaling ₹282.55 crore and negligible debt, Goldiam International maintains a robust net cash position, providing flexibility for future growth initiatives.

The company’s valuation is supported by its high-margin business, strong cash flows, and scalable retail expansion. While the broader diamond industry faces headwinds, Goldiam’s pivot towards LGD and B2C retail strengthens its long-term outlook.

d) Expansion into the Indian Retail Market

Goldiam’s entry into Indian retail through ORIGEM marks a strategic shift from a purely export-driven model. Key developments include:

Retail Store Openings: The company opened flagship stores in Mumbai and plans to expand to NCR and Bangalore. By March 2025, it will have six stores in Mumbai.

Revenue Potential: Each store is expected to break even at ₹30 lakh monthly sales, with plans to scale to 150-200 stores over the next 4 years.

Competitive Positioning: ORIGEM is priced 15-40% lower than competitors due to its vertically integrated supply chain.

Consumer Trends: The rise in gold prices has made LGD jewellery more attractive to Indian consumers, boosting demand for affordable, high-quality diamonds.

Expanding their Product Profile

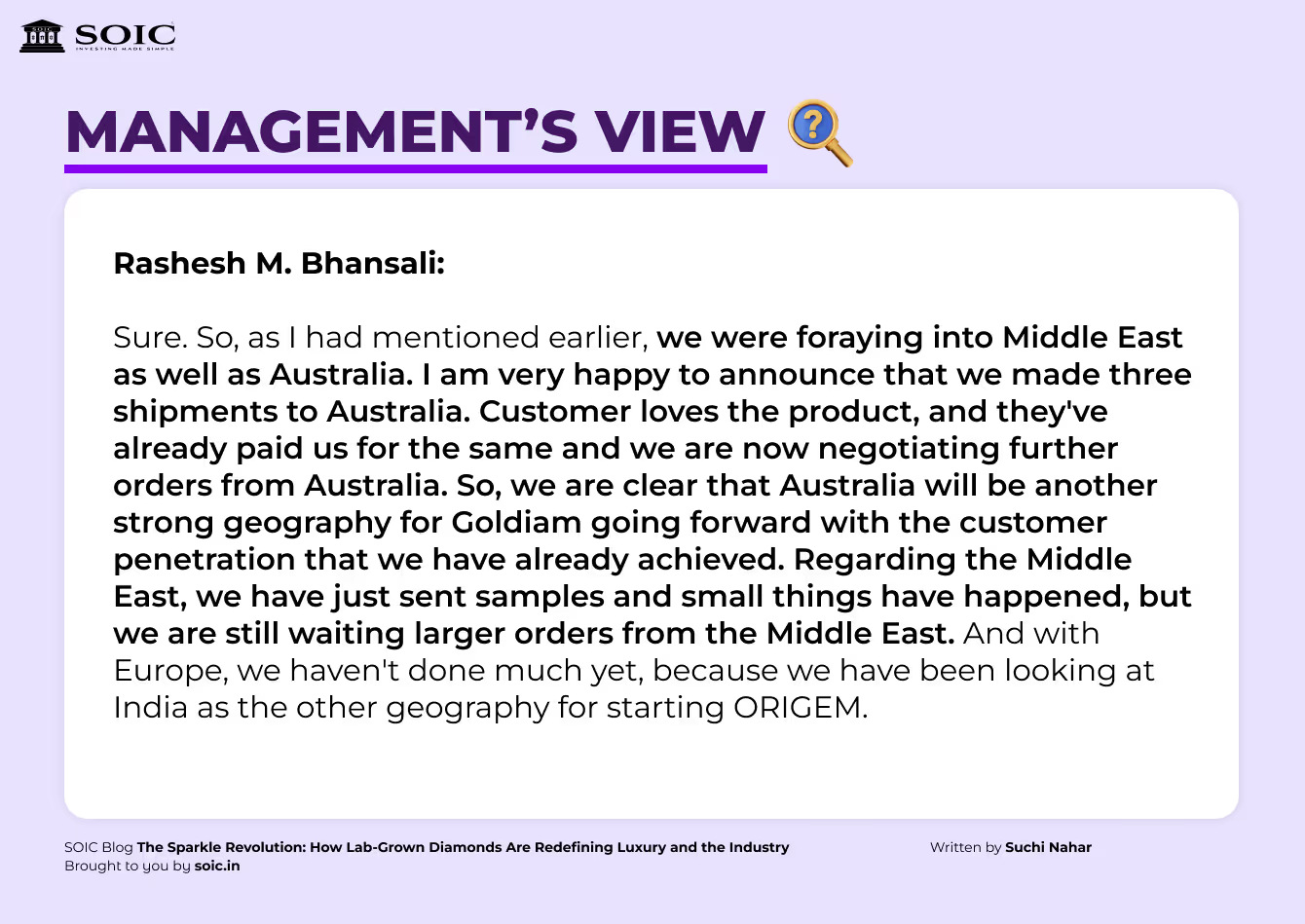

Foraying in Multiple countries – Management comments in the recent Conference Call

e)Store Economics

Goldiam has structured its store model with strong unit economics to ensure profitability from the outset.

The Average Selling Price (ASP) per store: ₹56-57k.

Store size: 800 sqft, with a cost of ₹6-6.5k per square foot.

Rental deposit: ₹40 lakhs.

Total store opening cost: ₹90 lakhs.

Inventory requirement: ₹1.1-1.2 cr. for regular stores and ₹2.2 cr. for large stores.

Breakeven within the first month, with a breakeven point at ₹30 lakh of monthly revenue.

Stores achieving ₹40-45 lakh monthly revenue can contribute significantly to PBT.

Goldiam has a stronghold in the U.S. market and is optimising its operations for efficiency.

The top 3 customers in the U.S. account for 55% of sales.

25 eco-friendly machines in operation, with no plans for expansion.

Shift from single-digit to 80% incremental sales in LGD.

Inventory risk management and innovative design remain core focus areas

Forward Integration and Margins

Goldiam’s forward integration into jewellery manufacturing and retailing is expected to drive margins and ROCE.

ORIGEM brand: Focused on everyday fine jewellery, offering lower price points for studded pieces.

20-30% price benefit due to in-house manufacturing.

Centre stone setting factory was planned in the U.S., with a ₹15-20 crore outlay and a 3-4 month decision timeline.

Order book lead time: 3-5 months.

Consignment sales: ₹150 crore.

18% differential between loose and finished diamonds in India.

All-natural diamond center stones are set in the U.S.

Future Outlook: The Lab-Grown Diamond Boom in India

The lab-grown diamond industry is still in its early stages but is poised for exponential growth. Here is an interesting video that shows the growth journey of Natural diamonds vs. lab-grown diamonds over the years: c6b2e521-e4b4-442c-b577-aeb0598afa1a.wmv

Goldiam International’s growth trajectory is driven by:

Continued Expansion in the U.S. Market: Deepening relationships with large retailers and increasing per-store penetration.

Retail Scale-up in India: ORIGEM is set to become a major player in lab-grown diamond jewellery.

E-Commerce Optimization: Further integration of digital sales channels to enhance customer engagement.

Strong Financial Execution: Maintaining profitability, high cash reserves, and steady dividend payouts

Global Market Projections

The LGD market is expected to grow from $22.3 billion (2021) to $55.6 billion by 2031 (9.8% CAGR).

LGDs currently make up 11% of the US fine jewelry market, up from 3% in 2020.

By 2030, LGDs are expected to account for 10-15% of total global diamond sales.

India's Role as a Manufacturing Hub

India is set to become the largest exporter of LGDs, surpassing China.

With major FTAs (Free Trade Agreements) with the US and Europe, Indian companies will gain tariff-free access to key markets.

Will LGDs Overtake Natural Diamonds?

Younger consumers prefer sustainable alternatives and don’t see a difference between natural and lab-grown.

Luxury brands like Cartier and Tiffany are slowly adding LGDs, validating their long-term potential.

In India, bridal jewelry is still dominated by natural diamonds, but LGDs are gaining popularity for engagement rings and fashion jewelry.

Lab-Grown Diamonds (LGDs) are groundbreaking products that offer properties comparable to natural diamonds but are available at only one-tenth the cost. The company is leading the current transformation in the diamond jewelry sector, supported by strong distribution advantages from its partnerships with major retailers in the USA. With a solid management team and a history of financial prudence, the company distinguishes itself from other companies in the diamond jewelry market, some of which have questionable reputations.

The company has consistently rewarded its shareholders, distributing Rs. 2.1 billion over the past six years through dividends and buybacks. Notably, GIL has zero debt and a strong cash position of Rs. 2.7 billion as of the first half of FY24, demonstrating financial strength and resilience that is uncommon for a company of its size.

Over time, the company has transitioned from being a commodity player to a value-added participant. It focuses exclusively on jewelry manufacturing and avoids the commoditized trading of cut and polished diamonds. Key drivers of its robust revenue growth include maximizing wallet share with retailers in the USA, entering the Indian retail market for Lab-Grown Diamond jewelry with its proprietary brand, and expanding into new geographical territories.

As acceptance of Lab-Grown Diamonds continues to rise in the USA, it is expected that this trend will extend to India. Given that India has the largest consumer market with approximately 410 million millennials, the shift toward LGDs is likely to gain momentum in the country. We believe the company has strong jewellery manufacturing capabilities and the financial resources necessary to reinvest and build a powerful proprietary brand. Goldiam International is at the forefront of a revolutionary shift in the jewellery industry. As consumer preferences evolve and lab-grown diamonds become the new norm, Goldiam’s strategic expansion, robust financials, and innovation-driven approach position it as a clear winner in the space.

With its aggressive retail expansion in India, strong presence in the U.S., and innovative digital strategies, the company is not just adapting to change—it is leading it. Investors and industry stakeholders should closely monitor this growing sector and its pioneers, such as Goldiam, as it strives to become a dominant force in the global jewelry market. The future looks promising for LGD’s, much like the diamonds —sustainable, innovative, and full of potential!

Share your thoughts on whether you would prefer a lab-grown diamond or a natural diamond to surprise your loved one with. 🙂

A few on sights were artisans working

Disclaimer:

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

Consumer Goods

Consumer Trends

Industry Trends

Sector Analysis

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

%20(1).avif)

0 Comments