From Chocobar Carts to Corporate Cream: India's Ice Cream Empire is Just Getting Started!

BY

Shuchi Nahar

Consumer Goods

Remember chasing the Kwality wala on a hot summer day? That joy of your first chocobar or that Sunday scoop of kesar pista at the local Vadilal parlour? What once was a simple indulgence is now turning into one of India’s most thrilling consumer stories.

In the backdrop of a $5 trillion economy dream, a quiet cold war is brewing in the freezers—between legacy giants, global entrants, and new-age premium disruptors. Now, with Kwality planning a comeback listing, Vadilal sharpening its global edge, and brands like Havmor, Hatsun, and Hocco cooking up bold new strategies, the Indian ice cream industry is finally ready for its golden melt-up moment.

So what’s changed? Why is this ₹42,000 crore market suddenly hot? Which brands are positioned to ride the next big consumption wave?

Let’s scoop into the coolest story of Indian FMCG today.

Global Market Size

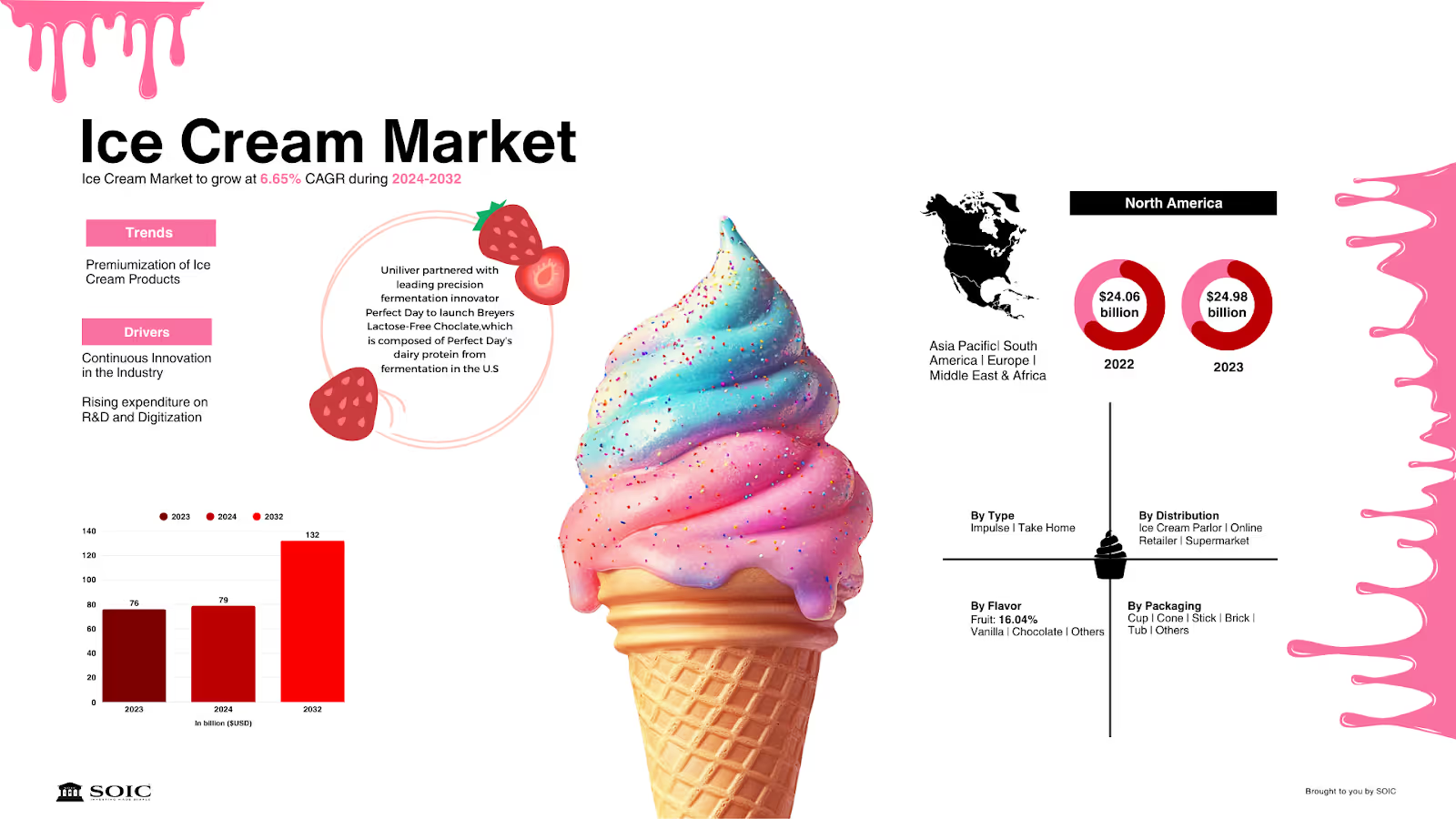

Globally, the ice cream market is valued at approximately $75-80 billion, with mature markets growing modestly at 3-5%, while emerging markets are seeing faster growth. Trends in health-conscious consumption and indulgent experimentation with flavors are prevalent, with major global players including Unilever, Nestlé, and General Mills.

The global ice cream market size was valued at $76.11 billion in 2023 and is projected to grow from $79.08 billion in 2024 to $132.32 billion by 2032, exhibiting a CAGR of 6.65%. Moreover, the ice cream market size in the U.S. is projected to grow significantly, reaching an estimated value of $28.56 billion by 2032, driven by high demand for frozen dairy desserts and the rising number of fast food chains and restaurants in the country. Asia Pacific dominated the ice cream market with a market share of 32.82% in 2023.

Indian Market Size

The Indian ice cream and frozen dessert market, valued at approximately $3.4 billion in FY2023, is experiencing robust growth, projected to exceed $5 billion by FY2026. This growth is primarily driven by the nation's rising disposable incomes, a young population, and expanding retail and food delivery networks. Despite this, per capita consumption remains low at 1.6 liters per person annually, compared to China's 4.3 liters, suggesting significant room for demand expansion.

The Indian market is dominated by large brands like Amul, Kwality Wall’s, Mother Dairy, and Vadilal, which together represent around 60% of the organized market. Emerging trends include increasing health-conscious consumption and growing demand for premium and natural products, with players like Naturals and NOTO catering to these niches.

Vadilal Industries Ltd.

Founded in 1907, Vadilal Industries is one of India's oldest and most well-known ice cream brands. Over the decades, it has introduced innovations and expanded its footprint across the country. The company is estimated to hold about 15-16% of India's organized ice cream market.

Product Portfolio:

Vadilal’s portfolio includes ice creams, frozen desserts, and frozen foods, with popular sub-brands like "Happinezz" and "Gourmet." While ice cream remains the majority of its revenue, the company has diversified into processed frozen foods under the "Quick Treat" brand, which has seen success, particularly with the Indian diaspora.

Manufacturing & Operations:

Vadilal operates two large ice cream production facilities in Gujarat and Uttar Pradesh, with a combined capacity of 625,000 liters per day. The company also runs a processed foods factory in Gujarat, catering primarily to international markets. With an extensive distribution network, including over 1,500 distributors and partnerships with major retail outlets, Vadilal ensures its products are widely available.

Geographic Reach:

While Vadilal is strongest in Gujarat and neighboring regions, it is gradually expanding into South and East India. Internationally, Vadilal has made significant inroads into the U.S. and other global markets, capitalizing on the growing demand for Indian products, especially among the Indian diaspora.

Key Business Triggers:

Promoter Dispute Resolution: A key issue for Vadilal in recent years has been the ongoing promoter disputes, which have raised governance concerns. These disputes escalated over allegations of financial mismanagement and resulted in the resignation of independent directors and the company’s auditor. However, a major settlement reached in March 2025 aims to resolve these disputes, enhancing corporate governance, streamlining brand ownership, and consolidating management. This resolution is expected to positively impact investor confidence, improve operational focus, and lead to a potential re-rating of the stock.

Export Growth & U.S. Market Performance: Vadilal’s U.S. business has grown exponentially since 2015, driven by strong demand within the Indian diaspora. The U.S. market now accounts for the majority of Vadilal's international revenue. With higher price realizations and margins compared to the domestic market, the U.S. business has become a significant profit driver. The company has also expanded its distribution network in the U.S. and is eyeing further growth in markets like the UK, Australia, and the Gulf.

Ongoing Capex Investment: Vadilal is undertaking a major capex initiative of ₹385 crore to relocate and expand its Bareilly plant. This will enhance manufacturing capacity, improve cold-chain infrastructure, and further strengthen the company's distribution capabilities. These investments are expected to support both domestic and export growth, particularly in high-margin international markets.

Financials & Valuation:

Vadilal Industries has demonstrated strong recovery post-pandemic, with revenues of ₹1,125 crore in FY2024 and net profits of ₹146 crore, reflecting a 13% net margin. EBITDA margins have expanded to 20%, aided by improved scale and operational efficiency. The company’s balance sheet is healthy, with manageable debt and strong liquidity.

Currently trading at a TTM PE Ratio of approximately 21x, Vadilal's valuation appears attractive compared to typical FMCG and consumption-focused companies in India. With improved governance and operational focus, the company is poised for a re-rating. Analysts expect top-line growth of 15-18% in FY2026, supported by increased domestic demand and sustained growth in the U.S. market.

Key Risks:

Seasonality & Weather Dependence: Sales are subject to seasonal variations, heavily influenced by weather conditions, which can impact demand, particularly in colder months.

Raw Material Price Volatility: Vadilal is exposed to fluctuations in dairy and other commodity prices, which could affect its profit margins.

Competition & Execution Challenges: The ice cream and frozen dessert market is highly competitive, with both established brands and new entrants vying for market share. Successful execution in product quality, distribution, and marketing will be critical for Vadilal’s continued growth.

Vadilal Industries is well-positioned to capitalize on the expanding ice cream and frozen dessert market in India and abroad. The company’s strong brand legacy, extensive distribution network, and growing export business, particularly in the U.S., provide solid growth prospects. The resolution of internal disputes and professionalization of governance are significant positives that could unlock further value. However, the company must navigate challenges such as seasonality, raw material price volatility, and intense competition to maintain its growth trajectory.

Kwality Walls:

Kwality Wall’s, a flagship brand under Hindustan Unilever Ltd (HUL), stands as a prominent player in India’s organized ice cream and frozen dessert sector. Leveraging HUL's extensive distribution network, the brand has achieved widespread availability across urban and semi-urban markets. Its product portfolio encompasses a variety of offerings, including Cornetto, Magnum, Feast, and Paddle Pop, catering to diverse consumer preferences.

Market Share & Competitive Landscape:

While specific market share figures for Kwality Wall’s are not publicly disclosed, industry estimates suggest that HUL's ice cream division holds a significant portion of the organized market, competing closely with leaders like Amul and Vadilal. The brand's emphasis on impulse consumption products and innovative flavors has bolstered its position in the competitive landscape.

Strategic Initiatives & Expansion:

Digital & E-commerce Integration: Kwality Wall’s has embraced digital platforms, partnering with food delivery services to enhance accessibility and meet the growing demand for home-delivered frozen treats.

Product Innovation: The brand continues to introduce new flavors and formats, aligning with evolving consumer tastes and preferences, including health-conscious options.

Sustainability Efforts: HUL has committed to sustainable practices across its brands, including Kwality Wall’s, focusing on eco-friendly packaging and responsible sourcing.

Strategic Demerger:

The demerger allows HUL to focus on its core operations while enabling the newly formed ice cream business to pursue growth opportunities independently. By listing the ice cream division separately, both entities can attract targeted investments and streamline their operations to better serve their respective markets.

Market Positioning and Competition:

Kwality’s market share has eroded in the past few years due to intense competition from both organized and unorganized players. Amul and Vadilal have strengthened their positions through better supply chains and higher brand equity.

Kwality is now attempting to reposition itself by focusing on affordability, regional appeal, and by exploring potential partnerships with global brands to boost its competitive edge.

Enhanced Focus: The new entity can concentrate on innovation and expanding its product portfolio to cater to evolving consumer preferences.

Production Capacity: Approximately 60,000 liters of ice cream daily.

Manufacturing Operations:

Processing Plants: Over 35 facilities across India.

Milk Chilling Centers: 800+ centers.

Distribution Network: Covers over 1.5 million retail outlets, ensuring product delivery within 24 hours of collection.

Geographic Reach:

Primary Markets: Strong presence in South India, especially Tamil Nadu.

Expansion: Diversifying into Andhra Pradesh, Telangana, Maharashtra, and other regions.

Key Business Triggers:

Product Diversification: Shift towards value-added products, which contributed to 43% of revenues in the first nine months of FY24.

Geographic Expansion: Reducing dependency on Tamil Nadu (from 67% to 55% revenue share over five years).

Supply Chain Efficiency: Robust procurement and distribution networks enhancing operational efficiency.

Financial Valuations:

Revenue: Estimated over ₹8,000 crore for FY24.

Net Profit: ₹235.8 crore for the first nine months of FY25, a 9.6% increase YoY.

Debt Metrics: TOL/TNW ratio improved to 1.55x as of March 2024 interest coverage ratio remains above 5x.

Hatsun Agro Product Ltd (HAPL): The ice cream segment is a significant contributor, estimated at around 25% of total revenue.

Key Risks:

Competitive Landscape: Facing stiff competition from players like Amul, Nestlé, and Britannia.

Regulatory Changes: Compliance with evolving food safety standards can increase operational costs.

Market Conditions: Fluctuations in rural demand and milk prices can impact profitability.

Operational Challenges: Supply chain disruptions and rising logistics costs.

Hindustan Foods Ltd (HFL)

Product Portfolio:

Categories: Home care, personal care, food and beverages, health and wellness, pet care, household insecticides, leather goods, sportswear, and accessories.

Recent Additions: Color cosmetics, OTC health products (e.g., Scholl footcare), ice creams, and beverages.

Business Model: Contract manufacturing for various FMCG products, including ice cream.

Recent Developments: Established a wholly-owned subsidiary, HFL Consumer Products Private Limited, to undertake an ice cream project in Uttar Pradesh.

Estimated Revenue Contribution: Given the recent entry into the ice cream segment, it is estimated that this segment currently contributes less than 5% to HFL's total revenue.

Manufacturing Operations:

Facilities: Multiple units across India, including recent expansions in Nashik (ice cream) and Hyderabad (home & personal care).

Capex: Significant investments in greenfield and brownfield projects, with gross block increasing from ₹77 crore in FY19 to ₹1,238 crore as of September 2024.

Geographic Reach:

Operations: Pan-India presence with manufacturing units strategically located to serve diverse markets.

Clientele: Partners with major brands like Hindustan Unilever, Reckitt Benckiser, Danone, and US Polo Association.

Key Business Triggers:

Client Acquisition: Secured new clients in the ice cream sector, aiming to become a leading contract manufacturer in this category.

Strategic Expansions: Investments in high-margin categories like color cosmetics and OTC health products.

Operational Efficiency: Focus on long-term contracts with guaranteed returns, ensuring stable cash flows.

Financial Valuations:

Revenue: ₹1,757 crore for H1 FY25, a 35% YoY growth.

EBITDA: ₹148 crore for H1 FY25, a 39% YoY increase.

Net Profit: ₹50 crore for H1 FY25, a 4% YoY growth.

Debt-to-Equity Ratio: 1.03 as of September 2024.

Hindustan Foods Ltd (HFL): The ice cream segment is a nascent part of the business, currently estimated to contribute less than 5% of total revenue

Key Risks:

Project Execution: Delays or cost overruns in new projects can impact profitability.

Integration Challenges: Recent acquisitions, like the shoe business, have introduced additional costs and complexities.

Equity Dilution: Frequent fund-raising for expansions may dilute existing shareholders' equity.

So, How Do You Play This Ice Cream Boom?

Now that we’ve licked through the trends and transformation, let’s talk capital allocation. The Indian ice cream story is no longer just about flavours—it’s a bet on logistics, brand equity, cold chain scale, and rural reach. And yes, there’s a smart way to ride this theme through listed players.

1. Hatsun Agro – The Rural Scoop King

With brands like Arun Ice Creams and Ibaco, Hatsun is a silent category creator, especially in southern India. The company has built unmatched distribution strength in Tier 2 and 3 towns, coupled with deep cold chain integration. With ice cream contributing a healthy share of its ₹7,000+ crore topline, Hatsun is a solid compounder in the dairy-plus-dessert playbook.

2. Hindustan Foods – The Dark Horse in Contract Manufacturing

Not a direct ice cream brand, but a critical enabler. Hindustan Foods manufactures for FMCG majors and has announced moves into the frozen food and desserts category. If capacity ramps up here, it could be India’s “frozen foods Foxconn.” Watch this one as a stealth beneficiary of premiumisation and third-party manufacturing growth.

3. Vadilal Industries – The Export-Fueled Comeback

Vadilal isn’t just revamping domestic offerings—it’s quietly exporting to 45+ countries, building an international brand in ethnic and premium ice creams. A turnaround in its corporate governance and strong results in FY24 make it a potential re-rating candidate.

4. Devoted Dairy Giants (Unlisted but worth tracking)

Amul – A category shaper but cooperative-run and unlisted.

Kwality Walls (HUL) – Part of Hindustan Unilever, which gives you indirect but strong exposure via its food portfolio. After it’s delisting it will be a good story to track

Havmor (Lotte) – Acquired by Lotte Korea, not separately listed, but HOCCO can be tracked closely

Growth Potential in Export Markets:

Though Kwality Wall’s is primarily focused on the Indian market, here are some nuanced pointers:

1. Global Play via Unilever Ecosystem:

Brands like Magnum and Cornetto, which are also sold under Kwality Wall’s umbrella, are already global brands. This allows HUL to tap into the Unilever Global Supply Chain, if needed, to explore select export or NRIs-centric markets (e.g., Middle East, SEA).

2. Export Tailwinds:

India's cost-competitive manufacturing in processed food could make it a hub for ice cream exports—particularly for shelf-stable dessert products (think pre-packed cones, frozen novelty items). If India becomes a production hub for Magnum-type products, HUL may push export-led growth from India—though this would be more visible in the global Unilever strategy than HUL’s.

Future Prospects:

With India’s per capita ice cream consumption at ~400 ml/year (vs. 22L in the US), there’s a massive headroom for long-term growth.

HUL’s management has signaled continued investment in expanding its ice cream footprint via infrastructure (cold chain) and digital-first initiatives (e.g., mobile kiosks, delivery).

High scalability due to HUL's pan-India reach + operational excellence means margins can expand with volume.

Management Views on the Listing of Kwality Walls:

HUL added that Kwality Walls (India) will be a leading listed ice cream company in India, with experienced management equipped with greater focus and flexibility to deploy strategies suited to its distinctive business model and market dynamics, thus realising its full potential.

“The business will continue to be equipped with the portfolio, brand, and innovation expertise from the largest global ice cream business, enabling it to keep winning in the marketplace. Demerger will also facilitate a smoother transition for business as well as our people,” said HUL in its exchange filing.

Positioning Summary:

Kwality Wall sits between mass premium and impulse indulgence.

It plays in both ₹10 Paddle Pops and ₹90 Magnums, covering a wide spectrum of aspirational consumption.

Focus on urban/semi-urban, catering to Gen Z and family-friendly categories (via Paddle Pop, Cornetto, etc.)

Differentiators:

Strong branding and recall due to celebrity endorsements, emotional advertising, and hygiene assurance (being a "branded" dessert in a fragmented market).

Cold chain infrastructure via HUL’s FMCG backbone gives it an edge in product delivery & consistency.

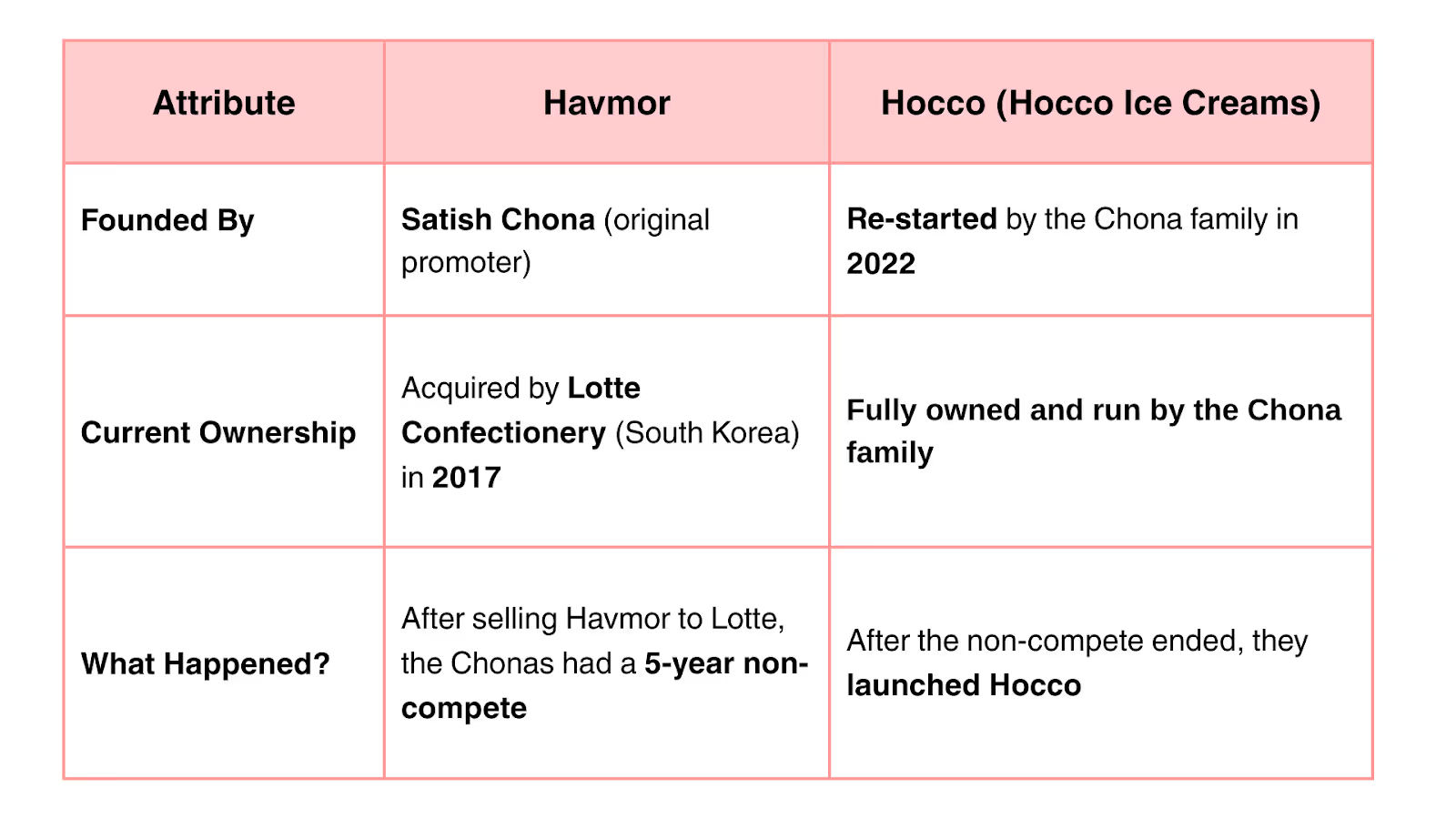

Havmor Ice Cream

Havmor Ice Cream, like Kwality, operates in the rapidly growing Indian Ice Cream and Frozen Dessert Market. The company competes primarily with Amul, Kwality, and Vadilal, and has been focusing on expanding its share in the organized sector. With the market expected to grow at 12-15% CAGR, Havmor has an opportunity to leverage this growth by capturing more market share in both the value and premium segments.

Havmor Ice Cream was founded in 1944, originally as a regional brand. The company has expanded over the years to become one of the prominent national players in India’s ice cream industry. Its reputation is built around offering a combination of affordable and premium ice cream options. In 2017, it was acquired by Lotte Confectionery, a South Korean company, which gave it an international distribution network and financial backing.

Product Portfolio:

Havmor offers a wide range of ice creams and frozen desserts, including tubs, cones, cups, and bars, catering to both value-conscious and premium customers. The brand has expanded its product line with innovative offerings such as sugar-free ice creams, health-conscious options, and limited-edition flavors.

Key Developments:

Corporate Governance Strengthening:

Havmor’s governance framework has improved significantly since its acquisition by Lotte Confectionery. The company now benefits from strong corporate governance practices and enhanced financial transparency.

The acquisition has allowed Havmor to streamline operations, optimize costs, and leverage Lotte's international experience in product development and distribution.

Expansion of Distribution and Market Penetration:

Havmor has strengthened its distribution network, especially in tier-2 and tier-3 cities, where demand for affordable ice cream products is growing. Its strong presence in traditional retail channels, along with its focus on modern retail and e-commerce platforms, has helped it increase its reach.

With Lotte's support, Havmor has been able to enhance its cold-chain infrastructure and logistics, ensuring consistent availability of products across India.

Innovative Marketing & Product Launches:

Havmor has invested significantly in branding and marketing to engage the younger generation, utilizing social media influencers, digital marketing, and regional advertising.

The brand is increasingly focusing on premiumization by introducing exotic flavors, lactose-free options, and sugar-free varieties. These innovations are aimed at catering to the growing health-conscious segment.

International Expansion through Lotte:

Since the acquisition by Lotte, Havmor has significantly benefited from international expansion. The brand now has a stronger foothold in markets outside India, especially in Southeast Asia, Middle East, and other regions where Lotte operates.

While Havmor and Hocco may seem similar at first glance—especially because they share common origins—they're actually two distinct brands today, with very different trajectories and ownership structures. Hocco is a spiritual successor to Havmor, created by the original promoters after they exited Havmor.

Hocco is positioning itself as a “clean label” brand, focusing on ice creams with no artificial flavors or synthetic ingredients. Think of it like the "premium artisanal revival" of the original Havmor legacy.

Future Prospects:

Valuations: Havmor, being a subsidiary of Lotte, enjoys stronger backing and governance, resulting in relatively better market sentiment compared to other players like Kwality. The company trades at a fair PE multiple, considering its market share, recent growth in the premium segment, and brand equity. For Hocco it is still an early-stage, private company so we have to observe how the story unfolds.

Growth Potential: Havmor's growth trajectory appears promising, especially with support from Lotte. The company's expansion of its product portfolio, emphasis on premium products, and enhanced distribution network are expected to drive both volume and value growth in the coming years. Hocco is prioritizing organic offerings and focusing on product quality within the premium segment. If scaled effectively, it could disrupt the premium market.

If Havmor is like a Maruti Suzuki of ice creams—mass appeal, trusted, and wide-reaching—then Hocco is like a Mini Cooper or Royal Enfield—niche, emotionally driven, and premium-by-positioning.

Key Risks:

High Level of Competition: Amul, Kwality, and up-and-coming premium brands are just a few of the regional and national competitors that Havmor must contend with in the fiercely competitive ice cream market.

Dependency on Distribution Channels: Due to its reliance on local markets for sales, the company is highly dependent on effective distribution and cold-chain logistics, both of which are susceptible to external factors like supply chain interruptions.

Seasonality: Havmor is susceptible to the seasonality of ice cream consumption, which peaks in the summer and declines in the off-season, just like other ice cream companies.

Market Share of Key Indian Ice Cream Brands (Organized Sector)

Note: Market shares are approximate and based on volume/value in the organized segment. Export businesses (like Vadilal’s US operations) are not included here unless directly impacting Indian revenues.

India’s Ice Cream Start‑ups: Funding Milestones and Growth Plans

A wave of young brands is reshaping India’s ice‑cream and frozen dessert landscape. Recent funding rounds signal both investor confidence and changing consumer tastes—toward clean labels, health‑focused treats, and nostalgic Indian flavours. Below is a concise look at the standout players and where their new capital is headed.

NOTO – Healthy Dessert Pioneer

NOTO is often grouped with “low‑calorie ice cream,” but the internal deck reveals a far broader ambition: to own the “healthy dessert” aisle across formats—ice cream, vegan pints, popsicles, low‑sugar mithai, and ambient sweeteners

50 + SKUs across five platforms: low‑cal high‑protein ice cream, zero‑sugar popsicles, vegan pints, mini bites, and halwai‑style sugar‑free mithai. Pipeline includes ambient pancake mixes, chocolate fudge sauce, and Greek‑yoghurt bars.

Centralised recipe development; third‑party conversion of premix to finished goods, supervised by NOTO staff.Swiggy/Zomato dark stores 67 %, D2C site 15 %, modern + general trade 9 %, quick commerce 1 % (pilot). Live in Mumbai, Bengaluru, Delhi‑NCR, Chennai, Pune via 85 dark stores; plan for 150 dark stores/600 retail outlets across 15 cities by Mar 2024.

Growth levers FY 24‑27 - Dark‑store expansion to 300, offline retail to 1,500, entry into 22 cities; ambient products for Amazon‑first scale; new formats like high‑protein chocobars; Tier‑2 penetration via general trade.

Unit Economics Snapshot FY 23

Average selling price (pint): ₹360

Gross margin: 52 % (ingredient cost diluted by premium ASPs, low wastage due to dark‑store proximity)

CAC payback: < 2 orders on aggregator channels; one order on D2C website.

NIC Ice Creams (Walko Food)

Total capital raised: > US $35 million

Latest rounds: US $11 million (May 2023); US $20 million led by Jungle Ventures (Feb 2024)

Approximate valuation: US $150 million

Portfolio brands: NIC, Yummo, Grameen Kulfi, Cream Pot

Next steps: Wider reach in modern trade and kirana stores, plus a pipeline of new flavours and formats.

Go Zero

Total capital raised: US $6 million

Latest round: ₹30 crore Series A (≈ US $3.6 million) in March 2025

Approximate valuation: ₹166 crore (≈ US $20 million)

USP: Zero‑added‑sugar, low‑calorie ice cream

Current footprint: E‑commerce and quick‑commerce platforms (Swiggy, Zomato, Blinkit, Zepto) across Mumbai, Delhi, Pune, Bengaluru and Hyderabad; expanding into offline retail.

Go DESi

Total capital raised: ≈ US $6.7 million

Latest round: US $4.9 million Series B (May 2024, led by Aavishkaar Capital)

Flagship products: Traditional Indian confections such as Desi Popz

Distribution: More than 40,000 general‑trade outlets nationwide.

Skippi Ice Pops

Total capital raised: ₹10 crore (≈ US $1.2 million)

Latest round: Pre‑Series A (May 2024) backed by Hyderabad Angel Network and Venture Catalysts

Product line: Fruit‑flavoured ice popsicles

Go‑to‑market model: Omnichannel—own D2C site, large e‑commerce marketplaces, and a fast‑growing retail network.

Legacy Leader: Naturals Ice Cream

Founded in 1984, Mumbai‑based Naturals remains a benchmark for artisanal, preservative‑free ice cream.

Metric Status (FY 24)

Annual revenue ₹380 crore

YoY growth 10 – 15 %

Outlets 160+ across 15 states

Estimated valuation ≈ ₹400 crore (privately held)

Growth agenda: doubling production capacity, adding domestic stores via its franchise model, and evaluating select international markets.

From sugar‑free innovation to regionally inspired pops and kulfis, India’s frozen‑dessert start‑ups are attracting capital at unprecedented speed. Their success will hinge on execution: scaling cold‑chain logistics, differentiating on flavour and health claims, and carving shelf space in both online and offline channels. Established players like Naturals show there is plenty of room—when quality and brand story align with evolving consumer expectations.

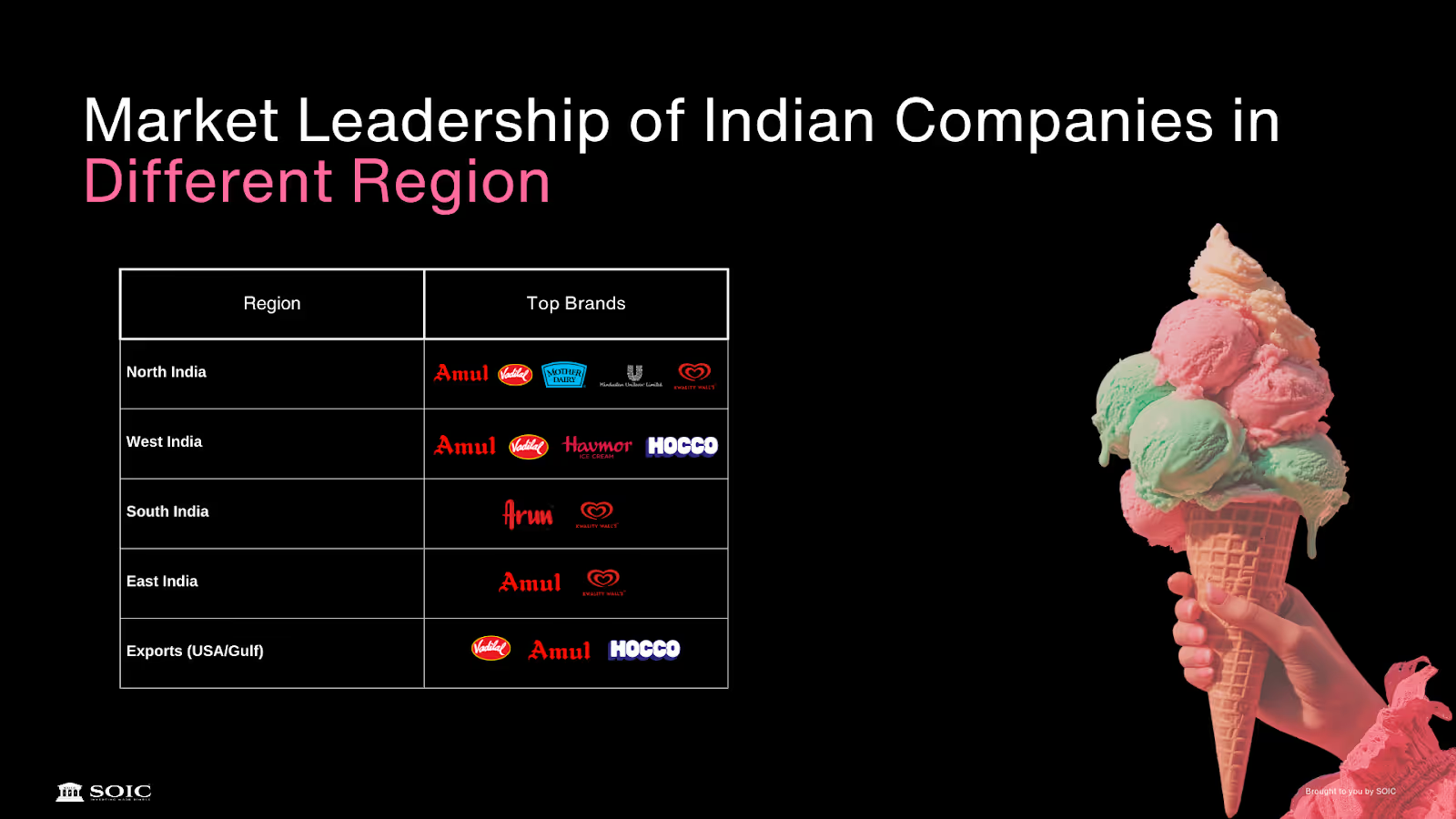

Market Leadership of Indian companies in different regions

What started as a simple chase behind the Kwality Wala has now transformed into a fierce competition for dominance in boardrooms, factories, and freezer aisles. The once humble stick of chocobar is now supported by global supply chains, extensive cold storage networks, and private equity firms investing heavily in India’s booming ice cream market.

Today's ice cream wars are about much more than just taste; they encompass distribution reach, expertise in cold chain logistics, strong retail presence, and a robust digital strategy. Companies like HUL with its scale-driven approach through Kwality Wall's, Havmor's transformation backed by Korean capital, and Vadilal's blend of global nostalgia with innovation are all rewriting the rules of the dessert industry.

The ice cream aisle is no longer a battle of tubs versus cones; it is a multi‑format, omni‑channel race to deliver “healthy hedonism.” Funding is a means, not an end—the winners will master cold‑chain logistics, disciplined new‑flavour cadence, and brand storytelling that resonates from Mumbai’s fitness studios to Lucknow’s family freezers. With its aggressive dark‑store rollout and product breadth, NOTO is the one to benchmark in 2025.

As rural cooling access improves, impulse purchases surge, and Gen Z opts for ice cream cones over traditional chai, this ₹42,000 crore+ industry is not just warming hearts — it’s creating competitive advantages, generating profit margins, and establishing long-lasting brands.

So, the next time you're at a roadside cart or in a premium dessert café, remember: you're not just tasting a dessert. You're witnessing India’s coldest consumer revolution. And trust us… this is just the first scoop.

Disclaimer:

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

Consumer Goods

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

.avif)

0 Comments