1. Theme

2. Business & about the Promoter

3. Growth

4. Risk

5. Valuations

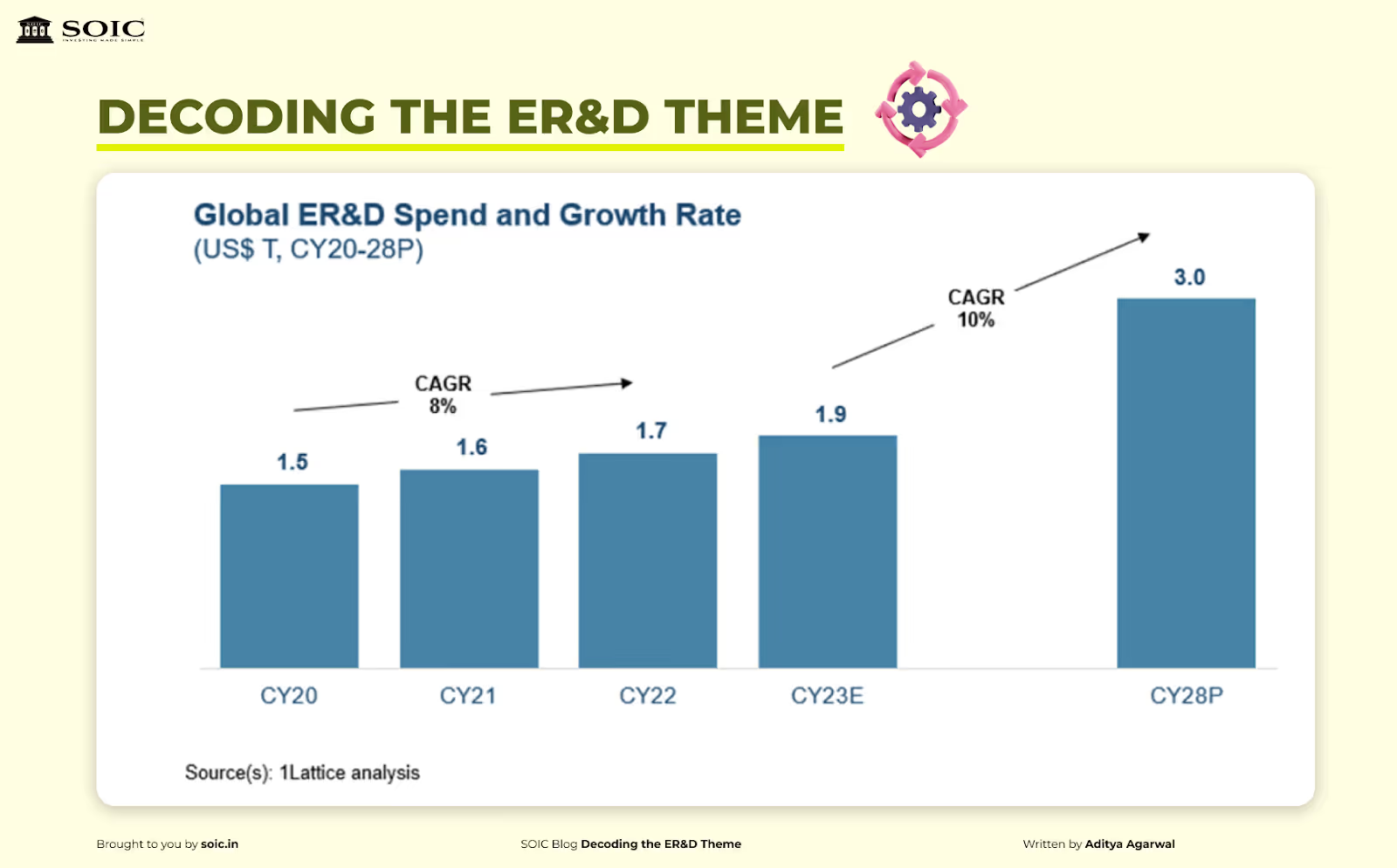

The engineering, research and development (ER&D) services space is at an early stage of penetration with a large TAM ( Total Addressable Market). Rapid advancement of technology and faster innovation has translated to a drastic reduction in product development timelines. This has increased the demand for outsourcing ER&D to third-party vendors with extensive experience in both traditional and contemporary products.

The manufacturing sector (auto, defence, industrials, aerospace) accounts for 49% of spending, followed by the technology sector (semiconductor, IT, telecom) at 40%, and the services sector (BFSI, media, health) at 11%. Geographically, North America leads with 50% of the spending, followed by APAC at 25%, and Europe at 24%.

The ER&D market's growth is fueled by several key factors, including shorter innovation cycles, cost optimization, a growing skills gap, Industry 4.0, and the need to address challenges in manufacturing engineering and digital twin technology.

The aerospace and defence ER&D sector is expanding at a rate of 16% and currently stands at $17 billion. Demand in aerospace is driven by a large order backlog which necessitates outsourcing. Specialized providers play a crucial role in providing cutting-edge expertise for advanced aircraft systems, hypersonic technologies, and AI-driven defence systems.

The demand in the defence industry is driven by the need for electronic warfare, advanced missiles, drones, AI in defence, commercial off-the-shelf solutions becoming prevalent.

The automotive industry is driven by increasing innovation in ADAS, telematics, infotainment, autonomous driving, and emissions. The global ER&D spend is US$ 25 billion at a 14% CAGR. Companies are switching to EVs rapidly, which requires a lot of software and technology incorporation. The digital engineering spend is expected to have >45% of outsourced automotive ER&D spend in CY28 compared to ~30% in CY23.

The energy and utilities industry are seeing a renewable revolution which requires expertise in solar panel technology, grid integration, smart meters and energy storage solutions. The integration of AI, IoT, cybersecurity, and data analytics is also a key trend in this sector, which currently stands at $11 billion and is growing at 15%.

The semiconductor industry is seeing increasing demand. Each new batch is super complicated and needs to be made at a fast pace which necessitates outsourcing. These include outsourcing services like advanced packaging, chip stacking, AI in value chain, design customization. These outsourced services have grown rapidly, reaching a market size of $13 billion and expanding at a rate of 19%.

The heavy engineering industry requires cost and process optimization, R&D, new technology and materials, and meets sustainability requirements. By leveraging advancements in smart manufacturing and supply chain management, the industry is poised to grow from its current value of $19 billion at a rate of 19%.

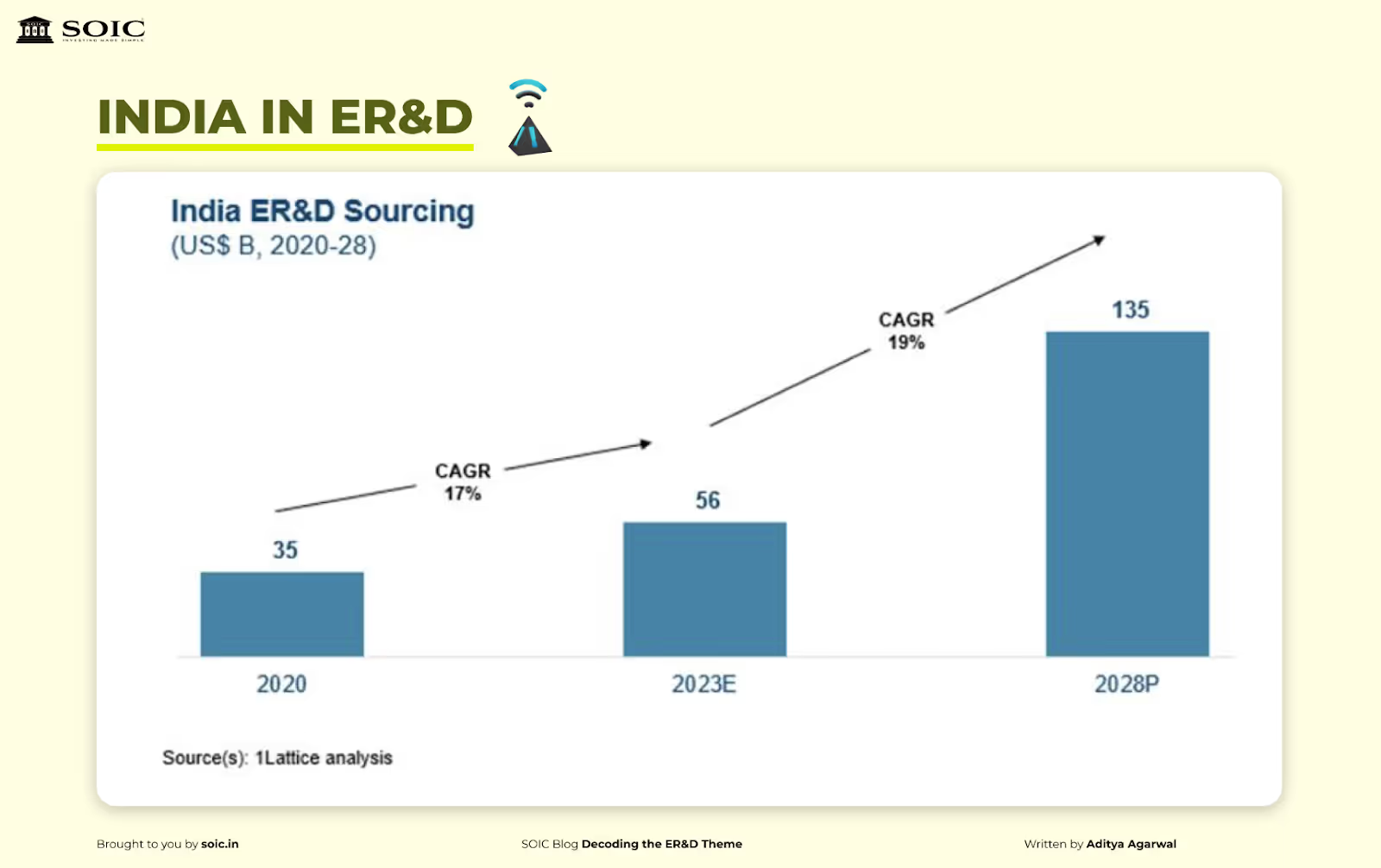

India emerged as a favourable destination for outsourced ER&D spend due several factors, including a large talent pool, an innovation ecosystem, affordable costs, maturing in-house research and development centres landscape and geopolitical support.

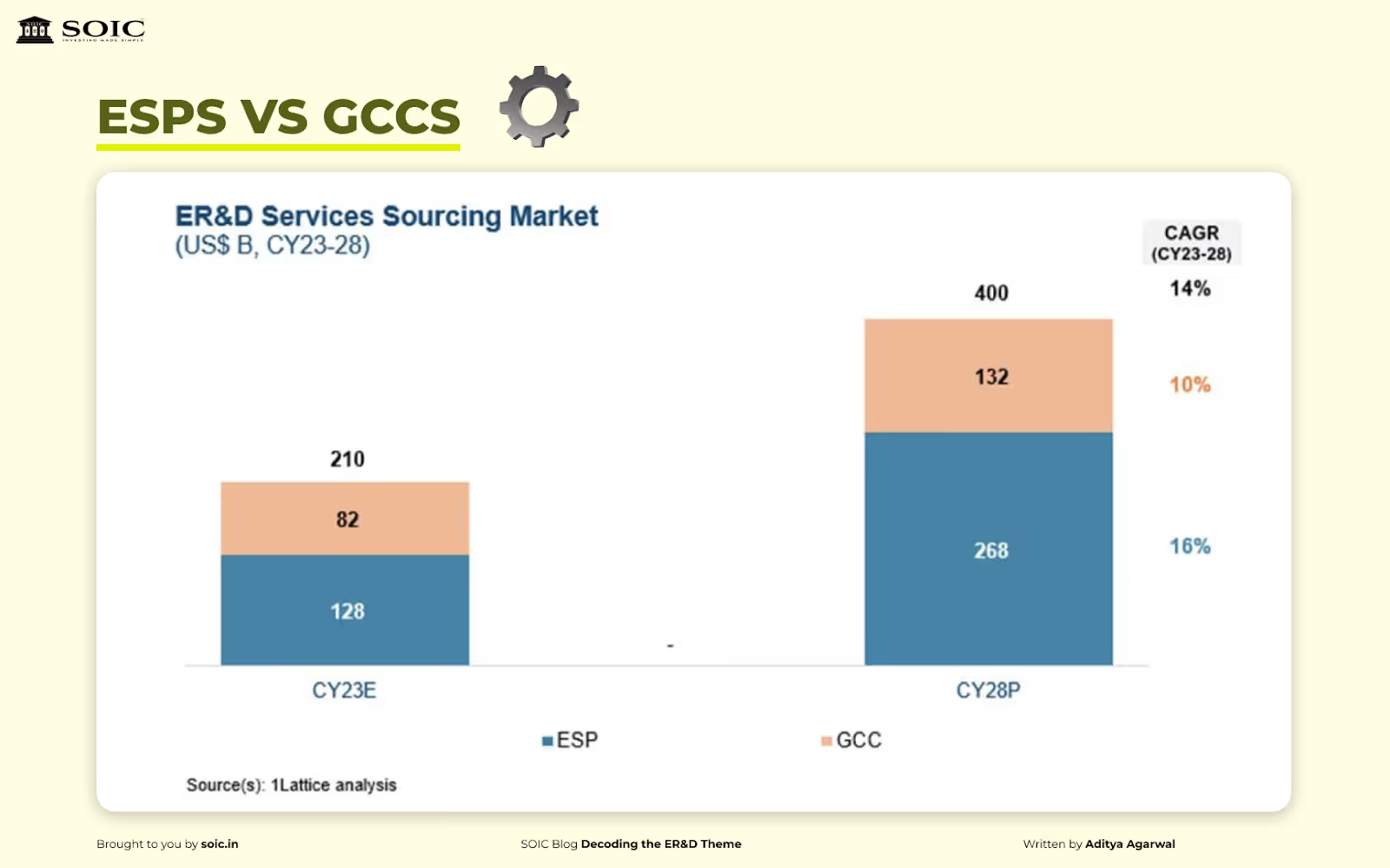

The Indian ESPs outsourced market currently holds 23% of the total outsourced ER&D spending through ESPs and has grown significantly over the years, with 1.3 million professionals available.

The global defence electronics market is valued at $142 billion and is anticipated to grow at 7% CAGR. This consists of communication, radar, electronic warfare, surveillance, and navigation systems, sensors, drones, 5G in defence, cloud computing, cyber defence, avionics and AR/VR in training.

The same market for India is valued at $2.7 billion and growing at a CAGR of 15.3%. India’s defence exports have grown with a CAGR of ~43%.

The Indian domestic market is seeing an increased demand in electronic warfare solutions, commercial off-the-shelf solutions and advanced missiles.

In the Union Budget 2023-24, capital allocations for the modernization and infrastructure development of the defence services have been increased to Rs. 1,62,600 crore, marking a 6.7% rise over 2022-23. The industry received Rs. 5.94 lakhs crore in budget 2023-24, reflecting a significant 13% increase from the previous year.

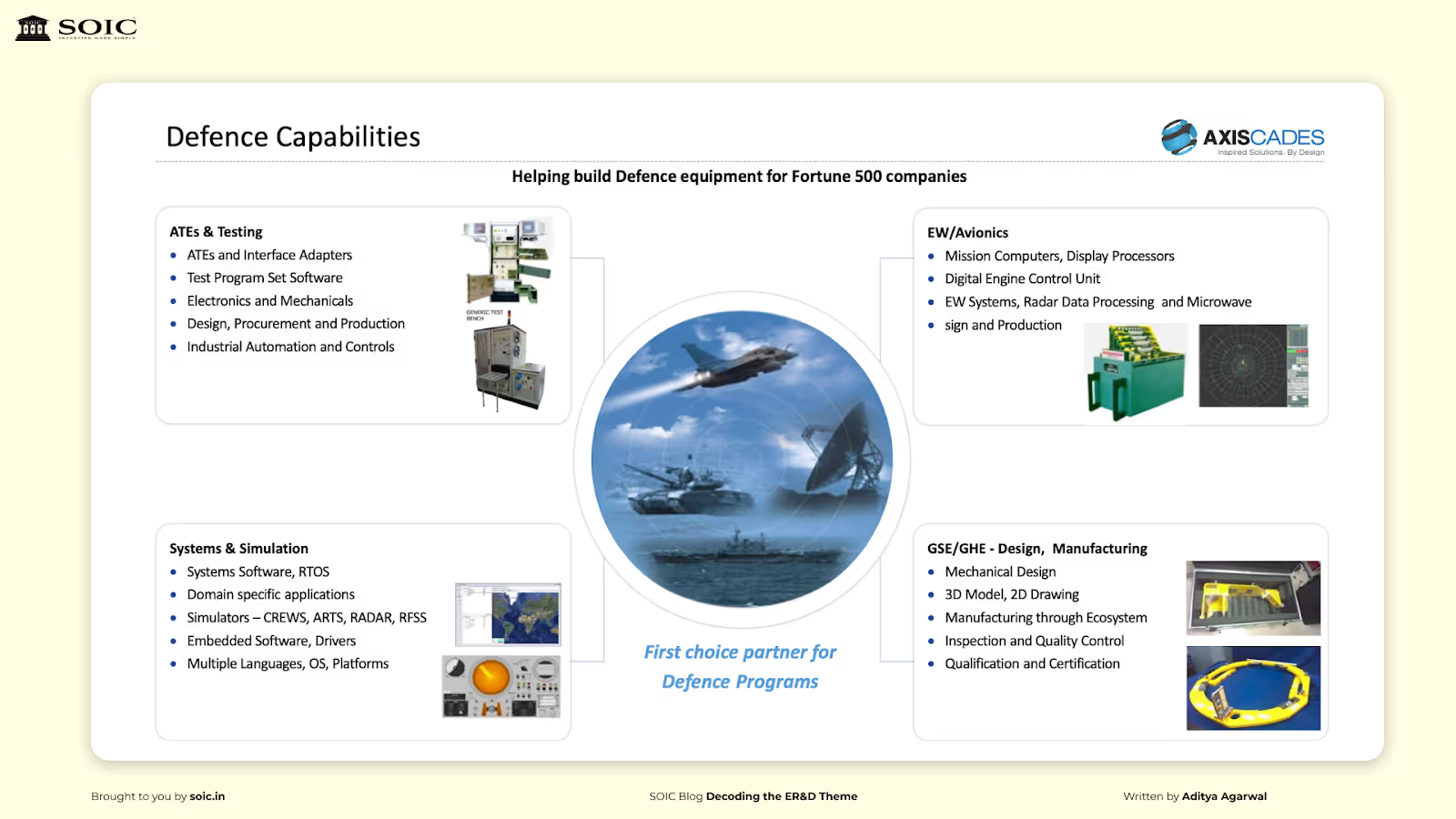

Aerospace capabilities include design solutions for primary and secondary structures, ranging from concept to certification, manufacturing and plant engineering, manufacturing concessions, in-service repair, aircraft modifications and certifications, 3D CAD modelling and detailing, aircraft communication, surveillance and infotainment systems.

Notable clients include Airbus, Bombardier, Thales, etc.

Dr. SRN established Airbus Engineering in India as a founder director. He also served as the Chairman of the FICCI Defense Task Force. He joined in 2008.

Murali Krishnan, CEO of the business, worked from 2008-2016 in Axiscades as Vice President. Then led the engineering divisions of Pennar and Cyient. He has now joined Axiscades again.

The aerospace vertical has seen 19% growth Year-on-Year in Q2FY25. They provide services such as fuselage & product development, customer support services, plant engineering & embedded software and hardware solutions to Airbus (their main customer in this line of business).

They recently received a work order valued at Rs. 120 crores for aerostructures.

The company is also offering Digital Manufacturing Services to OEMs and is in talks with Airbus for aircraft and military programs. Additionally, the company is in talks with Agnikul to establish a space MoU.

Currently, the aerospace business is facing a challenge when it comes to growth. As their major customer AIRBUS isn’t able to ramp up production due to shortages. Axiscades revenues in this business line are linked to how much AIRBUS is able to produce. Airbus has downgraded its own production guidance this year from 800 planes to 774.

Before we start analysing this segment, think of defence revenues in terms of production and prototyping or in simpler words, prototyping means providing samples for a product or a defence equipment to get it approved. Whereas, production means to get the final order for the same. Prototyping comes in at a loss but it is important to get orders for the final production. It’s like a catch 22 situation. Defence businesses which are transitioning from prototyping revenues to production are the ones where non linear scale up of revenues and margins can happen. For example, when Data Patterns IPO’d, it was going through this transition period. Their margins in 2019 were 19% and these expanded to 43% over the last 4 years.

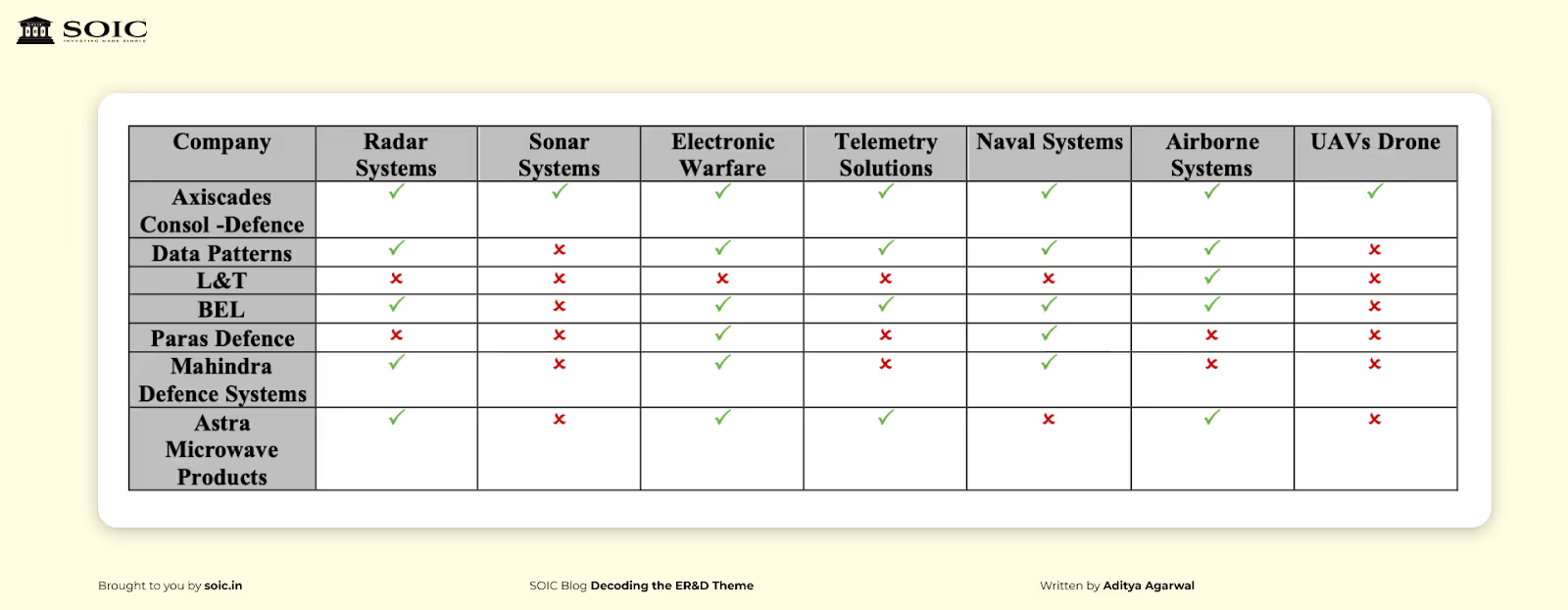

Coming to Axiscades Defence business, they have a portfolio of radar, sonar, anti done solutions, drones for high payload applications and systems for electronic warfare. They are an offset partner to an entity registered in France and have successfully established strategic partnerships for discharge of its offset obligations.

In 2022, Axiscades completed the acquisition of Mistral Solutions, a Bangalore-headquartered company specializing in radar systems, sonar systems, electronic warfare, telemetry solutions, naval systems, and airborne systems, with a presence in the USA, Canada, Europe, Singapore, and South Africa. The acquisition was valued at Rs. 292 crores, approximately two times of Mistral Solutions' revenue, and was financed through debt, bank guarantee, and a Rs. 70 crore share swap.

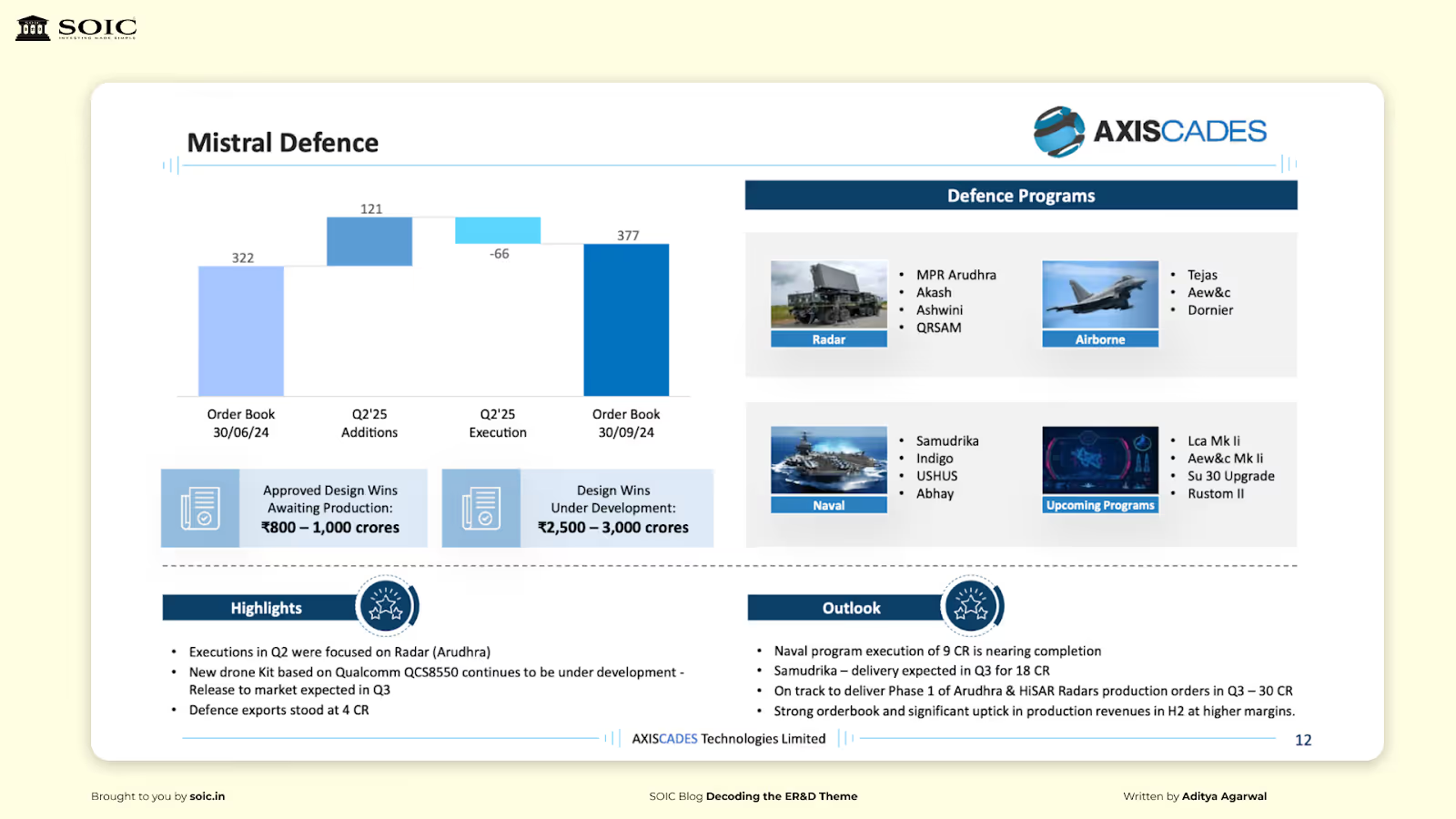

Some of the major defence projects where they are participating include Tejas, Sukhoi, Ashwini radar, Arudhra radar, QRSAM, and Aakash. This is where both risks and opportunities lie. If some of these projects get delayed, then the revenue scale up might take some time. The commercial production of LCA Tejas (around 16-24 per year) and Su30 upgrades (around 50 per year) would gain traction starting FY27. However, HAL has been facing delays in engine supply from GE: https://www.india.com/news/us-betraying-india-over-tejas-fighter-jet-donald-trump-pm-modi-external-affairs-minister-mirage-2000-jaguar-and-mig-29-fighter-jets-lca-7561917/

Currently, Mistral has an order book of Rs. 377 crores. Prototyping is a loss making part of Pie and in production revenues they make 25%+ EBITDA Margins. Lets see how the Production revenues have been scaling up:

FY23: 30 Crores

FY24: 112 crores

FY25 expectation: 170 crores

In their recent concall (Q2), the management stated that they want to scale up defence business to become 60% of their overall revenues in next 12-18months. This implies their defence business is scaling up from Rs. 170 crores expected in FY25 to almost Rs. 500 crores. This will be majorly led by production revenues which are high margin in nature.

How their production revenues scale up and growth of Defence business is the make or break thesis for this business which is the key monitorable going forward.

Services include product design and validation, engineering, software development, manufacturing support, virtual manufacturing, supply chain management, and automated engineering processes.

Notable Clients include Caterpillar, Komatsu, and Siemens.

While this business is growing at 8-10% YoY, they are focusing on optimizing cost structure and focusing on higher-margin digital engineering work instead of existing low-margin mechanical business. This is a business where they make single digit EBITDA Margins. The major customer is Caterpillar for whom they do fixed cost drawing. They have recently renegotiated the contract. As an investor its difficult to see how this vertical scales up or improves.

Includes programming tools, processors/ micro- processors, memory devices along with other embedded engineering services and platforms. Through the acquisition of Mistral, Axiscades got access to design and fabrication facilities for electrical and electronic items.

Due to the increasing adoption of semiconductors in auto and aerospace industries, Axiscades has a competitive advantage in chip design services and AI functionality.

Semiconductor business witnessed a growth of 36% year-on-year, driven by an increased traction from existing clients. Main customers in semiconductors are Texas Instruments and Qualcomm. Both of them contribute to 80% of revenues in this part of the business segment. They have just recently started doing work with NVIDIA. The semiconductor business is similar to ER&D services which other players such as HCL do in this vertical.

Competencies lie in concept design, vehicle electronics, telematics, active and passive safety systems (ADAS), Infotainment, manufacturing engineering, wiring harness, software testing and after-market services. Provide solutions with respect to interiors, exteriors, powertrains, chassis and hydraulics. Significant role in the software driven future of mobility. Their capabilities in this vertical includes integrating cutting-edge technologies such as AR, VR, AI, and ML to position our customers in the adoption of Industry 4.0 practices.

Acquired add-solutions GmbH in Germany because of their relationship in 2022 and they are serving Volvo, Mercedes-Benz, Volkswagen.

In the fiscal year 2023, experienced growth of 65.20% YoY. However, due to muted auto demand in Europe, the company’s business declined 11% year on year in Europe. The company expects this to revive in the long term as companies will slowly restart product development cycles in hybrid and electric. This business segment is suffering especially post influx of cheap Chinese EV’s in Europe. It will be interesting to see if they can get back to growth here or not. For this year, they have guided for degrowth/flattishness.

Axiscades recently acquired Epcogen Private Limited, a niche player in the energy sector has expanded structure design offerings and is also helping them reach the Middle East markets. They are working with two customers from the UK in renewable energy projects and have recently opened an office in Dubai to expand their customer basel in the Middle East. This is a small part of the business at the moment, it will be interesting to see how it develops going forward.

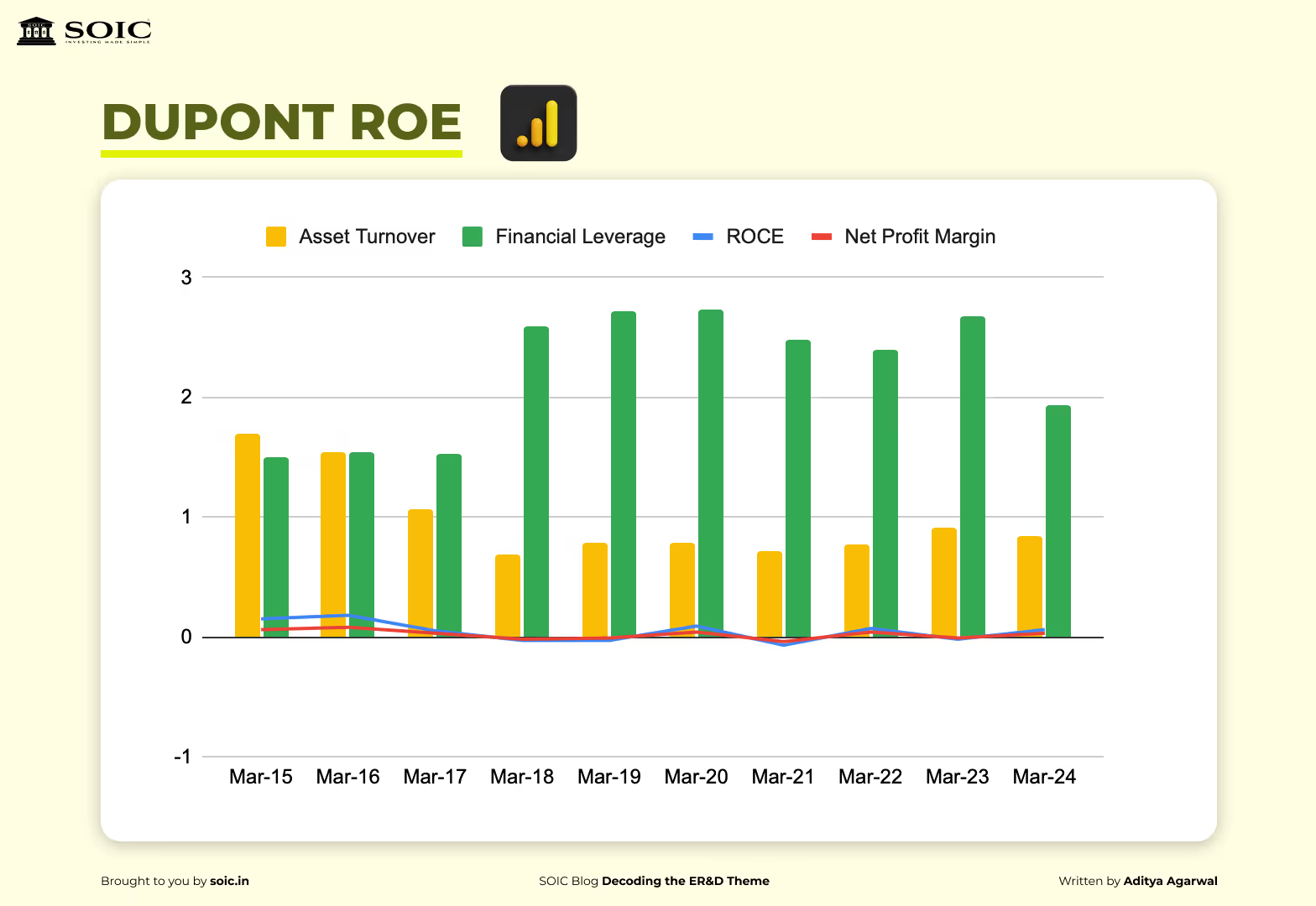

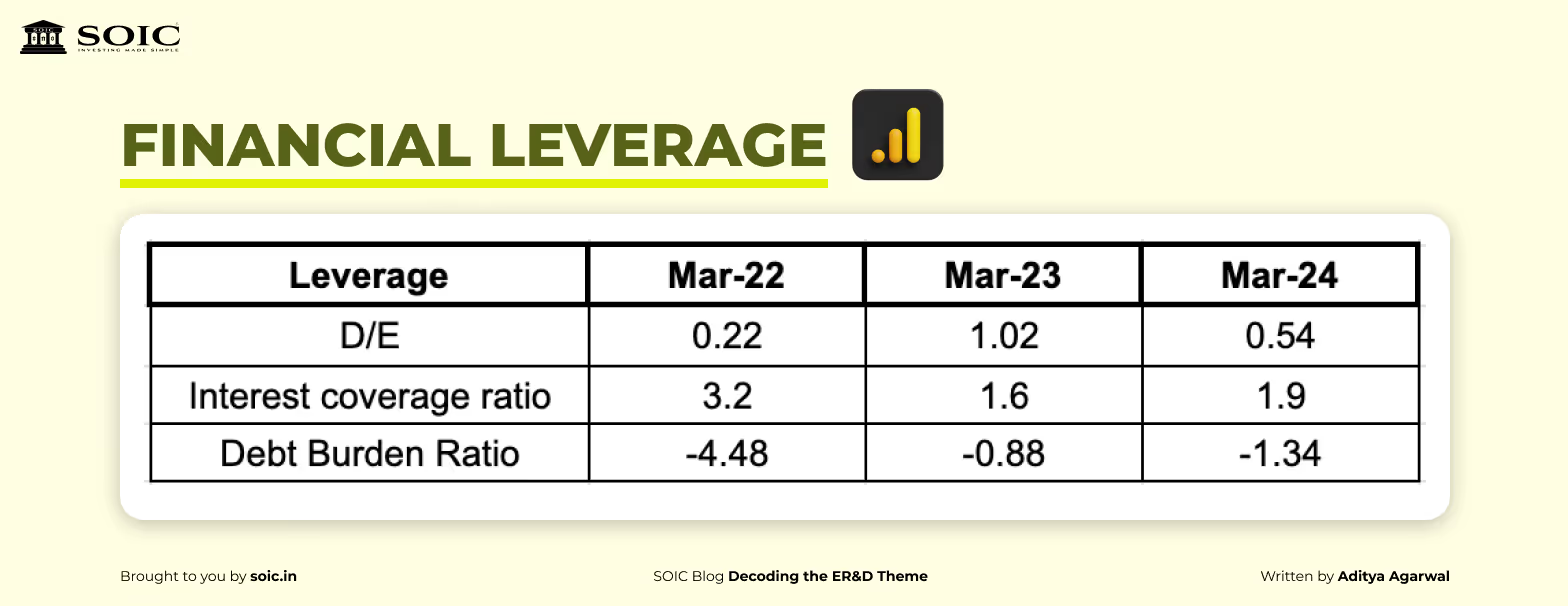

Improving financial leverage, but poor asset turnover and net profit margins have brought the ROE down to 6% (Average of 5%).

The company repeatedly takes debt to do acquisitions. However, they are aiming to be net debt free by the end of 2026. Recent QIP of Rs. 200 crores helped them repay some debt and also take low cost debentures from improved credit rating.

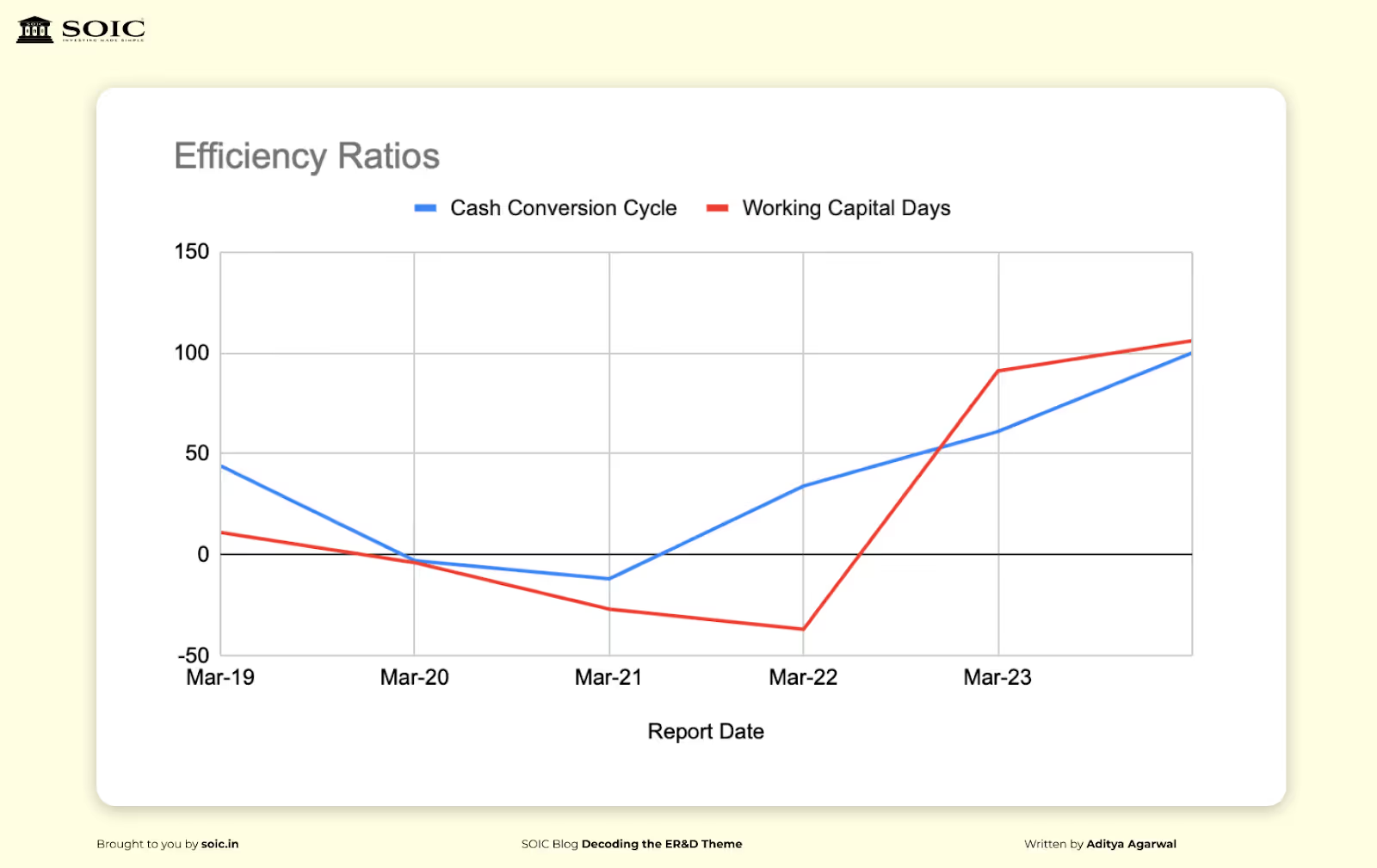

As the company takes more and more defence contracts, the cash conversion cycle extends due to the nature of government contracts and tenders. The average EBITDA to CFO conversion is 64%.

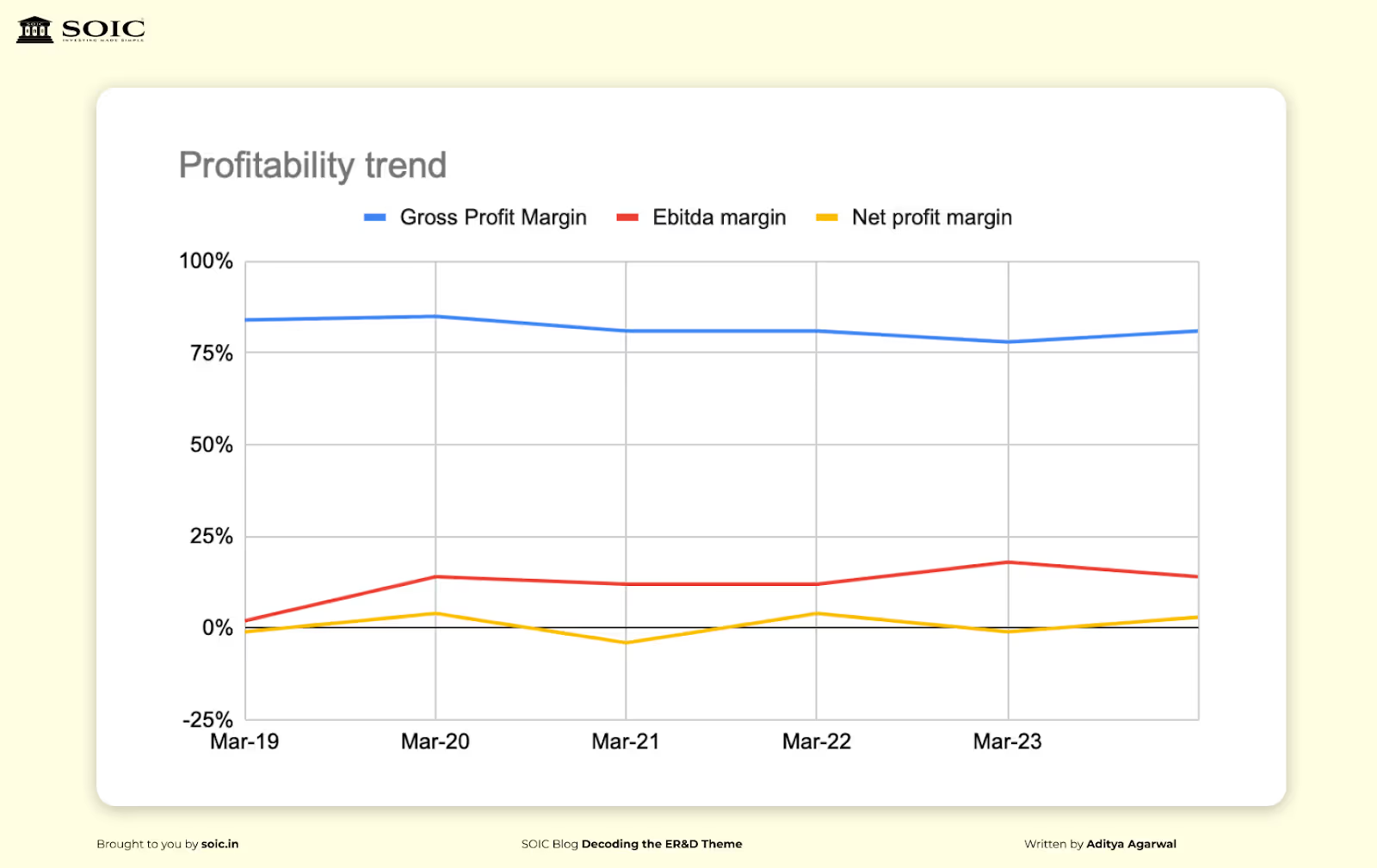

Gross profit margin looks high at about 81% because there are very few sales of goods in the company. As the company slowly increases goods sales, this might become more relevant.

The EBITDA margin averages around 12% and accurately represents the margin from both goods and services sales.

The net profit margin has been highly volatile in the past due to high financing costs in the company. This will change going forward as debt falls to 0.

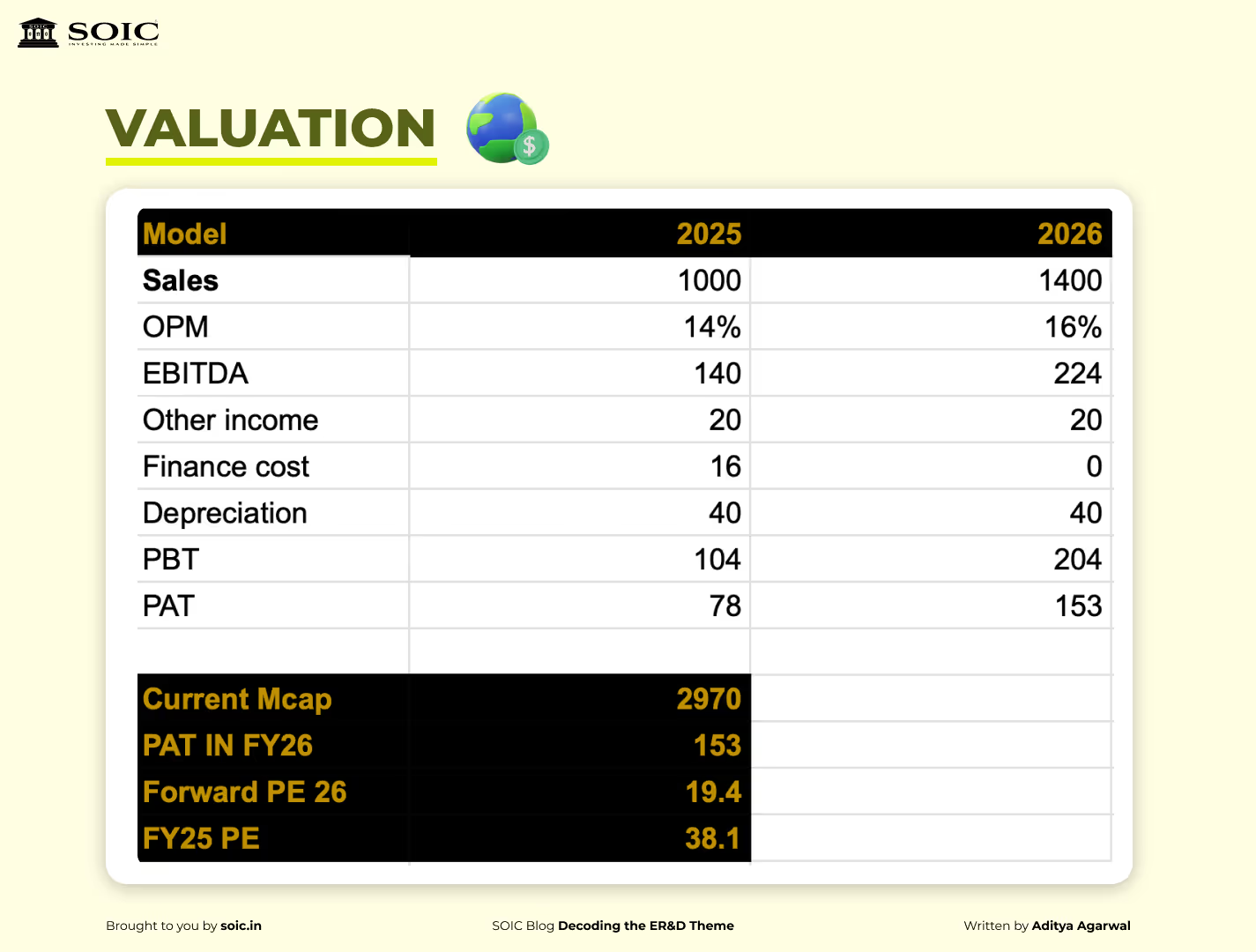

Let's go by their guidance and be more conservative. Earlier, the management was guiding for Rs. 1,600 crores and Rs. 160-170 crores PAT. We have reduced that to Rs. 1400 crores top-line in our assumptions. This is just a rough framework for looking at the multiples below.

Finance cost will fall to 0 as they are paying off debt, depreciation to be constant and sales to grow by 40% as growth in defence, semiconductor and aerospace inflects with EBITDA margins expanding by 2% YOY in FY26.

Post the management change announcement, the stock broke-out on high volumes, and currently is going through a pullback phase with increasing relative strength vs the market.

We discussed the business of Axiscades in depth covering all the key details of the business, promoters, risks, valuations and key growth drivers. Key monitorable remains the growth in defence production, aerospace and semiconductor segments. Monitoring EBITDA margins will be the key for profitability to inflect.

Please share your thoughts with us in the comments section for the author Aditya Agarwal. Twitter profile: https://x.com/adityaphobia

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organisation, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference

0 Comments