For years, nuclear energy was treated like a forgotten chapter of history.

The world believed solar and wind alone would power the future.

Then reality arrived.

AI data centers started consuming unimaginable electricity. Europe faced an energy crisis. Countries realized that economies cannot run on intermittent power alone. And suddenly, the world started looking back at nuclear energy — not as a problem, but as a solution. Now India is preparing for one of its biggest energy transitions ever.

The interesting part? The real opportunity may not just lie in electricity generation… but in the hidden ecosystem of engineering, capital goods, precision manufacturing, and industrial oligopolies quietly powering this theme behind the scenes.

The Silent Energy Revolution That Could Shape India’s Next 20 Years

For almost three decades, nuclear energy was treated like a dangerous relic of the past.

Chernobyl happened.

Then Fukushima happened.

Countries started shutting down nuclear plants. Investors avoided the sector. ESG narratives pushed solar and wind as the only future. Slowly, the world began believing that nuclear energy belonged to the past.

But history has a strange habit.

Just when the world thought it had moved on from nuclear, reality came knocking again.

Europe faced an energy crisis after the Russia-Ukraine conflict. Gas dependency became a geopolitical weapon. AI and data centers suddenly started demanding unimaginable amounts of electricity. Countries realized that intermittent power alone cannot run modern economies.

And slowly, quietly, nuclear energy began returning to the global conversation.

Not as a backup option.

But as a strategic necessity.

Today, some of the world’s biggest economies are once again accelerating nuclear investments. China is rapidly building reactors. The European Union has declared nuclear importance for energy security. Even global technology giants are signing long-term nuclear power agreements to secure electricity for AI infrastructure.

And in the middle of this global shift, India may be entering one of the most important energy transitions in its history.

The biggest misconception in energy discussions is this:

People often confuse installed capacity with actual electricity delivered.

A solar plant may have large installed capacity, but solar power works only when the sun shines. Wind power works only when wind conditions are favorable.

Electricity grids, however, do not care about narratives.

They need reliable power every second.

Hospitals cannot stop operating because wind speed falls. Factories cannot shut down because of cloudy weather. AI data centers cannot pause their servers at night.

This is where nuclear becomes important.

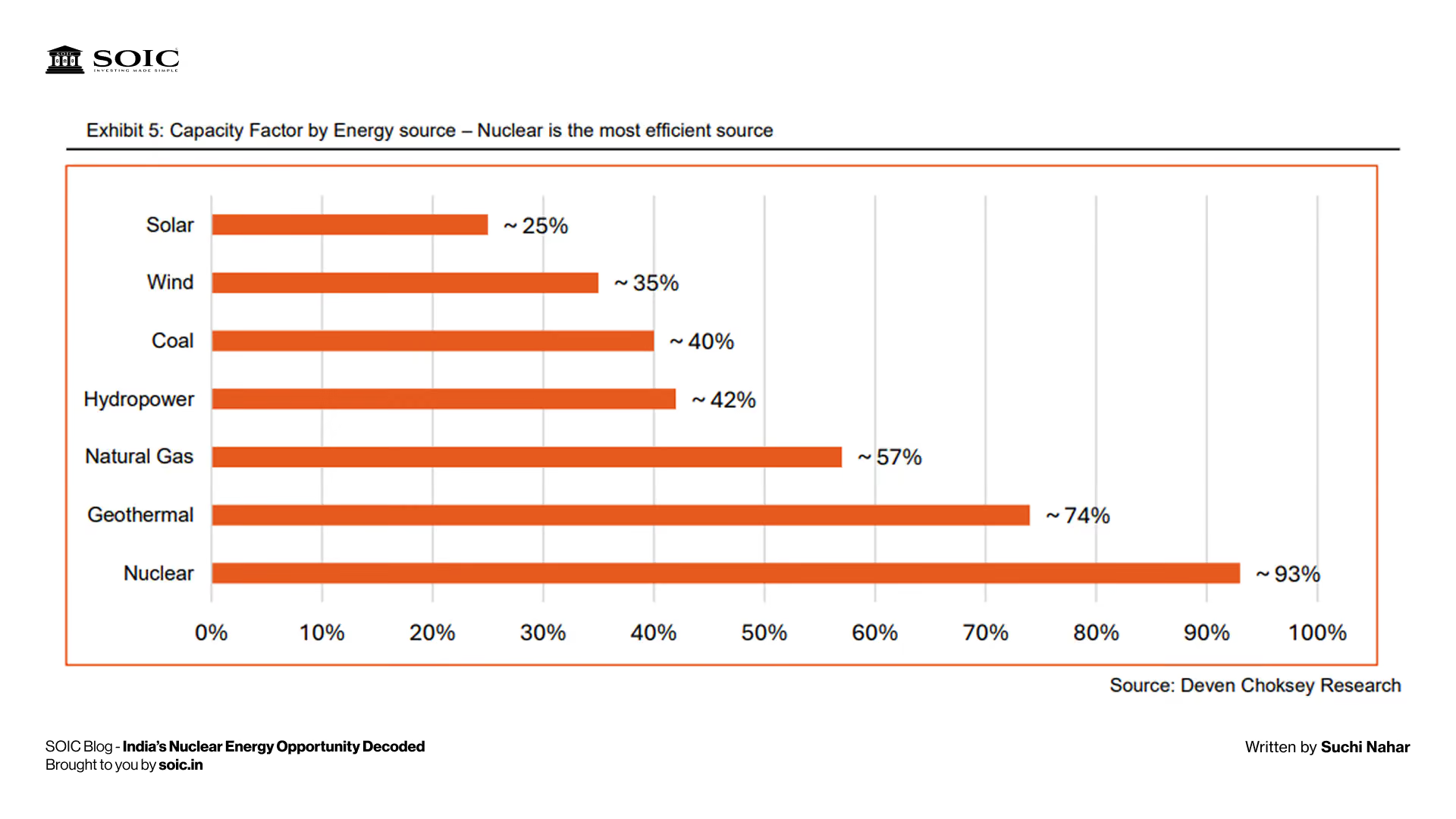

Nuclear plants operate at extremely high capacity factors compared to renewable energy. The DR Choksey report highlights that nuclear plants operate at nearly ~93% capacity factor versus much lower utilization for solar and wind.

In simple words:

Nuclear plants produce electricity almost continuously.

This makes nuclear power one of the few large-scale sources of clean baseload power available to humanity.

And that distinction changes everything.

One of the most fascinating aspects of nuclear energy is its sheer energy density.

1 kilogram of enriched uranium can generate nearly 160,000 kWh of energy compared to roughly 3 kWh from 1 kilogram of coal.

Think about that for a second.

The difference is not marginal.

It is exponential.

This is why nuclear plants require significantly less land compared to solar farms generating equivalent electricity. In a country like India, where land acquisition itself becomes a major bottleneck, this advantage becomes strategically important.

The debate is often framed as:

“renewables versus nuclear.”

Reality may be different.

The future grid may actually require both.

Renewables can provide distributed clean energy, while nuclear can provide the stable backbone required to support industrialization, electrification and AI-driven demand.

Nuclear’s high-capacity factor and dispatch ability makes it an important technology for ensuring grid stability in an increasingly electrified and decarbonizing ecosystem.

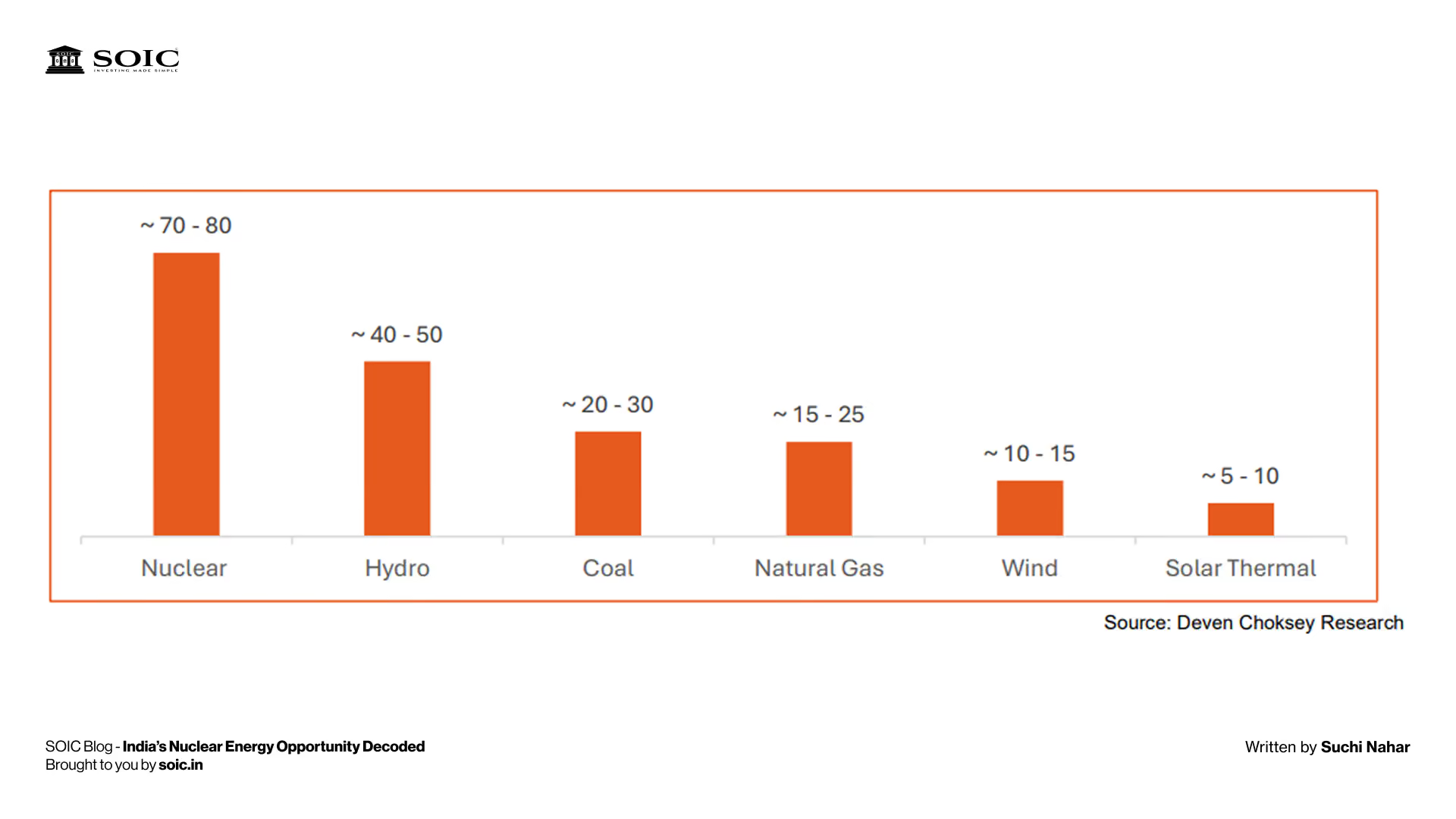

On an adjusted basis, after considering efficiency losses, storage requirements, transmission infrastructure, and balancing costs, nuclear energy stands out as one of the most cost-competitive sources of power generation. Although nuclear energy is characterized by high upfront capital intensity, its lifecycle economics shift the perspective. Nuclear energy has a superior Energy Return on Investment (EROI), meaning that nuclear assets generate significantly more energy output relative to the energy invested in their construction and operation.

Despite the elevated initial capital expenditures, the strong energy economics and lower system-level costs associated with nuclear energy make it a financially viable and scalable long-term solution within the global energy mix.

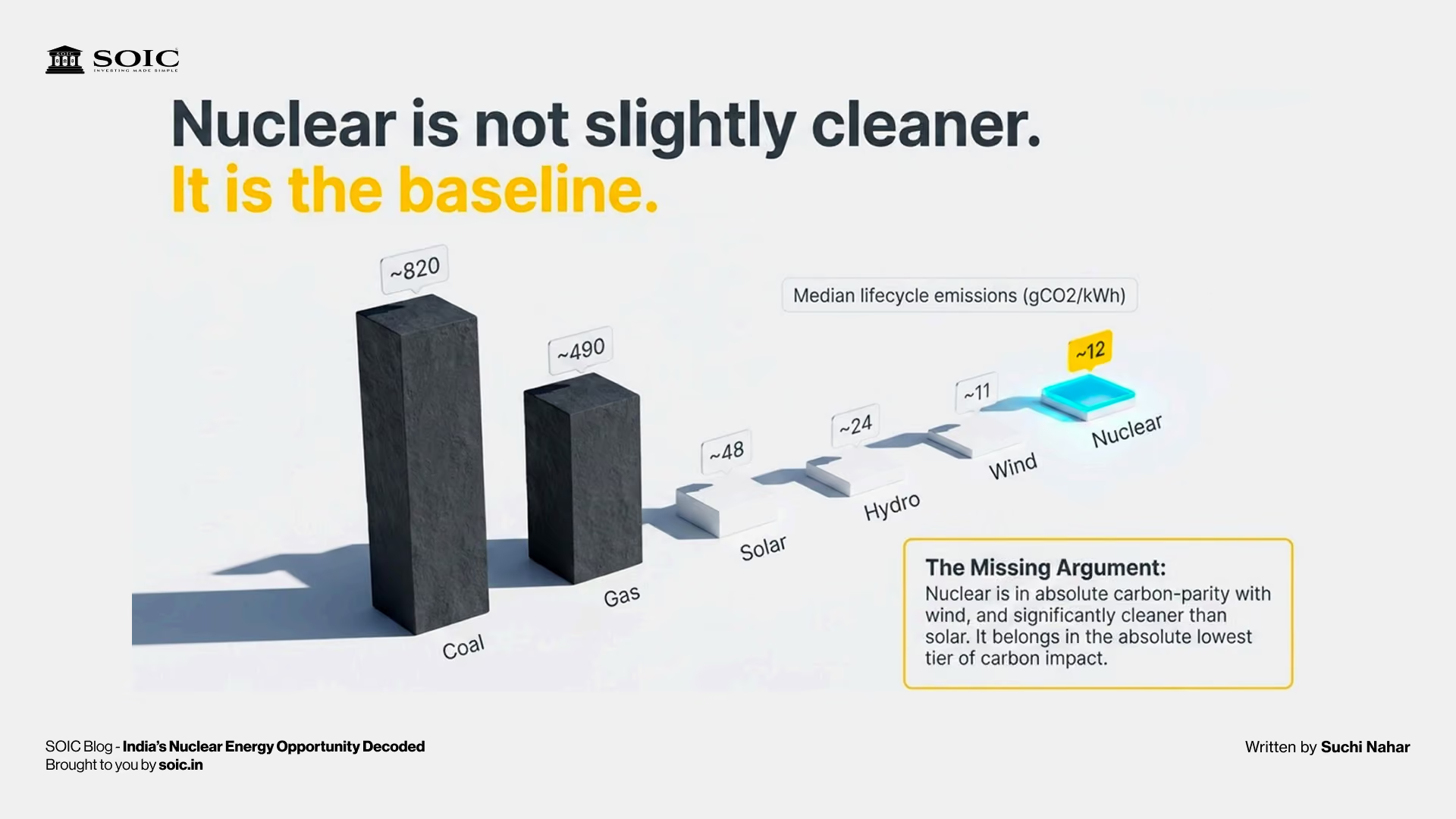

Nuclear energy is one of the lowest-carbon sources of power generation and causes minimal harm to the environment. When considering the full lifecycle—including construction, fuel transportation, operation, and decommissioning—nuclear energy ranks among the cleanest technologies in terms of greenhouse gas (GHG) emissions.

Although nuclear energy is characterized by high upfront capital costs, its lifecycle economics offer significant advantages. Energy Return on Investment (EROI) shows that nuclear facilities produce a much higher energy output compared to the energy invested in their construction and operation. Despite the considerable initial capital expenditure, nuclear energy’s strong economic performance and lower overall system costs make it a financially viable and scalable long-term solution in the global energy mix.

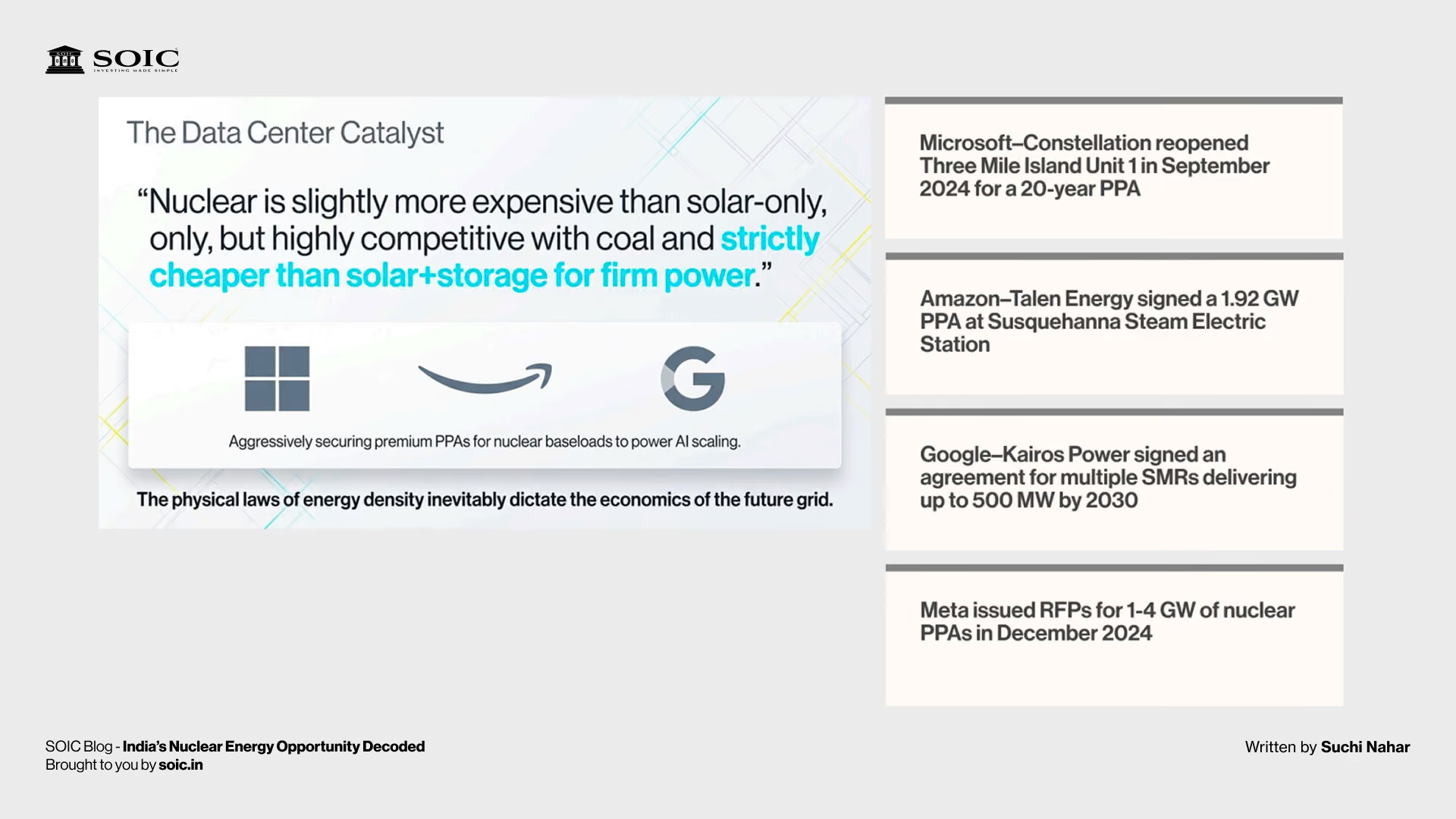

The world is entering a phase where electricity demand itself may structurally rise for the first time in years.

Artificial Intelligence is incredibly power intensive.

Massive data centers, semiconductor fabrication, cloud computing infrastructure and electrification trends are pushing electricity demand higher globally. AI data center electricity demand could rise exponentially over the coming decade.

This is precisely why technology companies are suddenly becoming interested in nuclear power agreements.

Because AI requires:

And currently, nuclear is one of the few scalable solutions capable of delivering all four simultaneously.

The narrative around nuclear power is no longer only about climate.

It is increasingly about economic survival in an AI-driven world.

Most countries built nuclear ecosystems using abundant uranium reserves.

India did not have that luxury.

India has relatively modest uranium reserves but possesses one of the world’s largest thorium reserves.

This forced India to think differently.

And perhaps that constraint became India’s biggest strength.

India designed a unique three-stage nuclear strategy:

This strategy was not built for short-term convenience.

It was built for long-term energy sovereignty.

The beauty of India’s PHWR model is that it does not require heavily enriched uranium, reducing dependence on foreign fuel cycles. Over decades, India slowly built indigenous capabilities despite sanctions, technology restrictions and geopolitical isolation.

India didn’t build its nuclear ecosystem quickly. It built it stubbornly.

And that persistence may now become valuable.

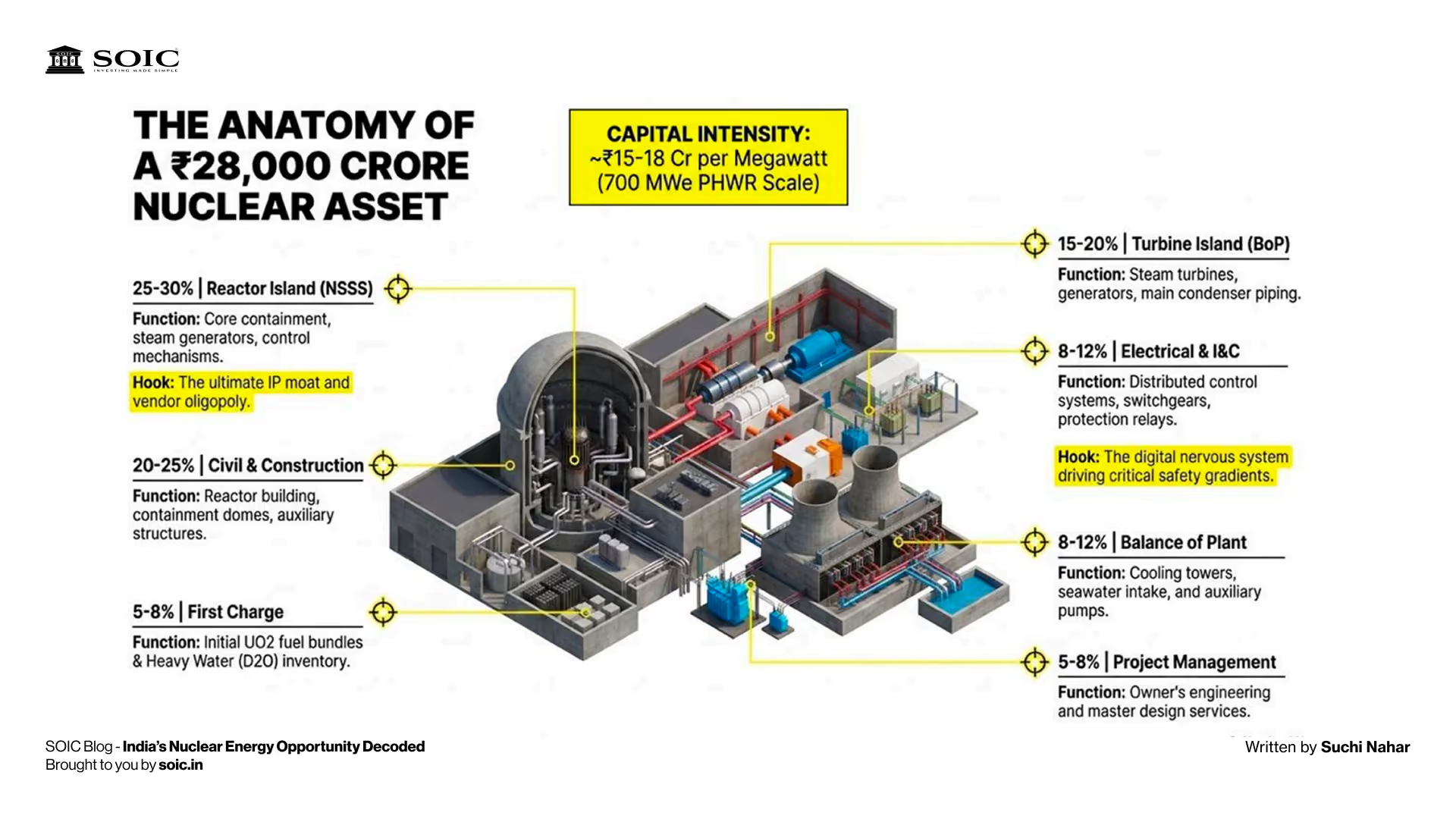

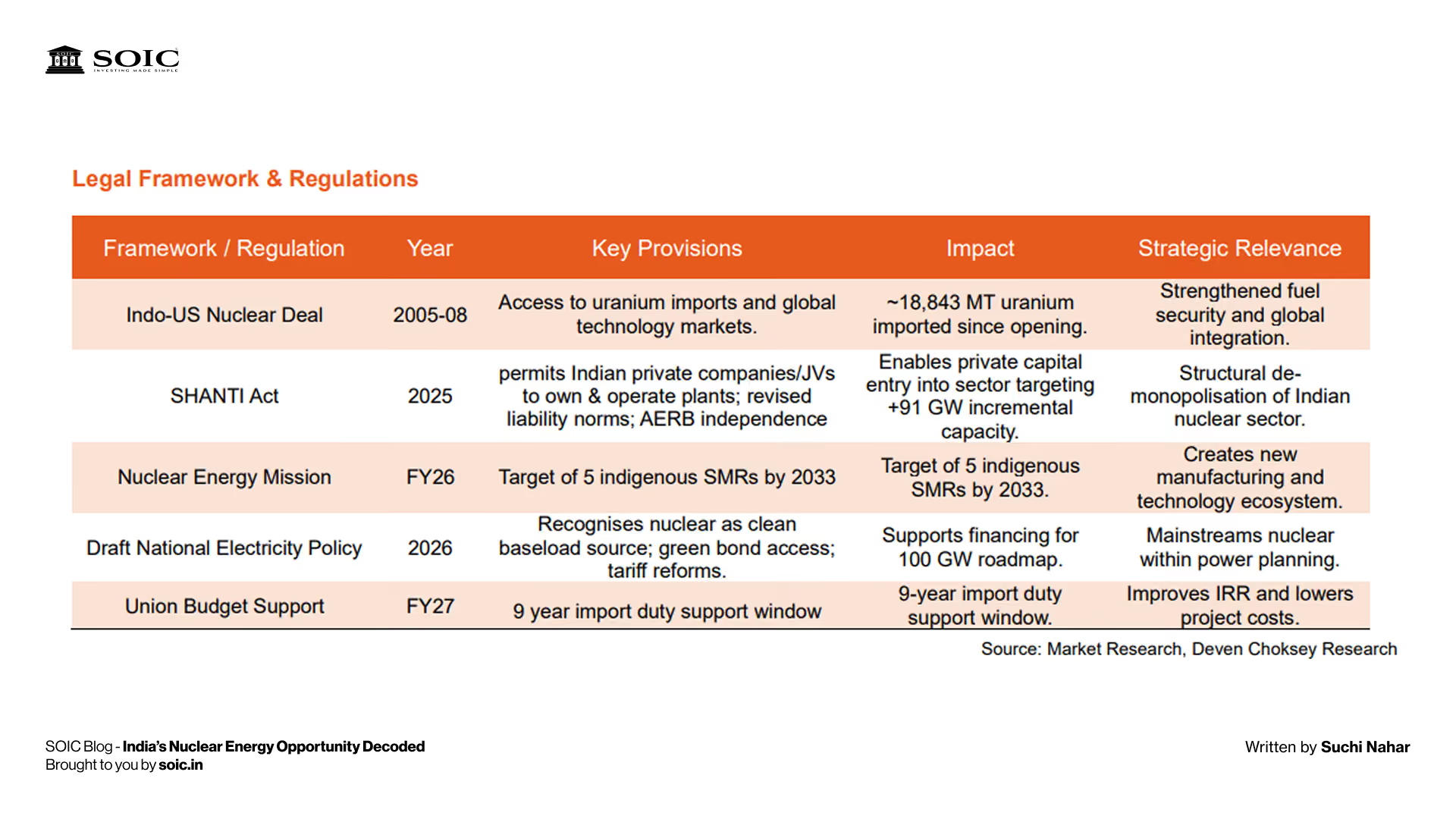

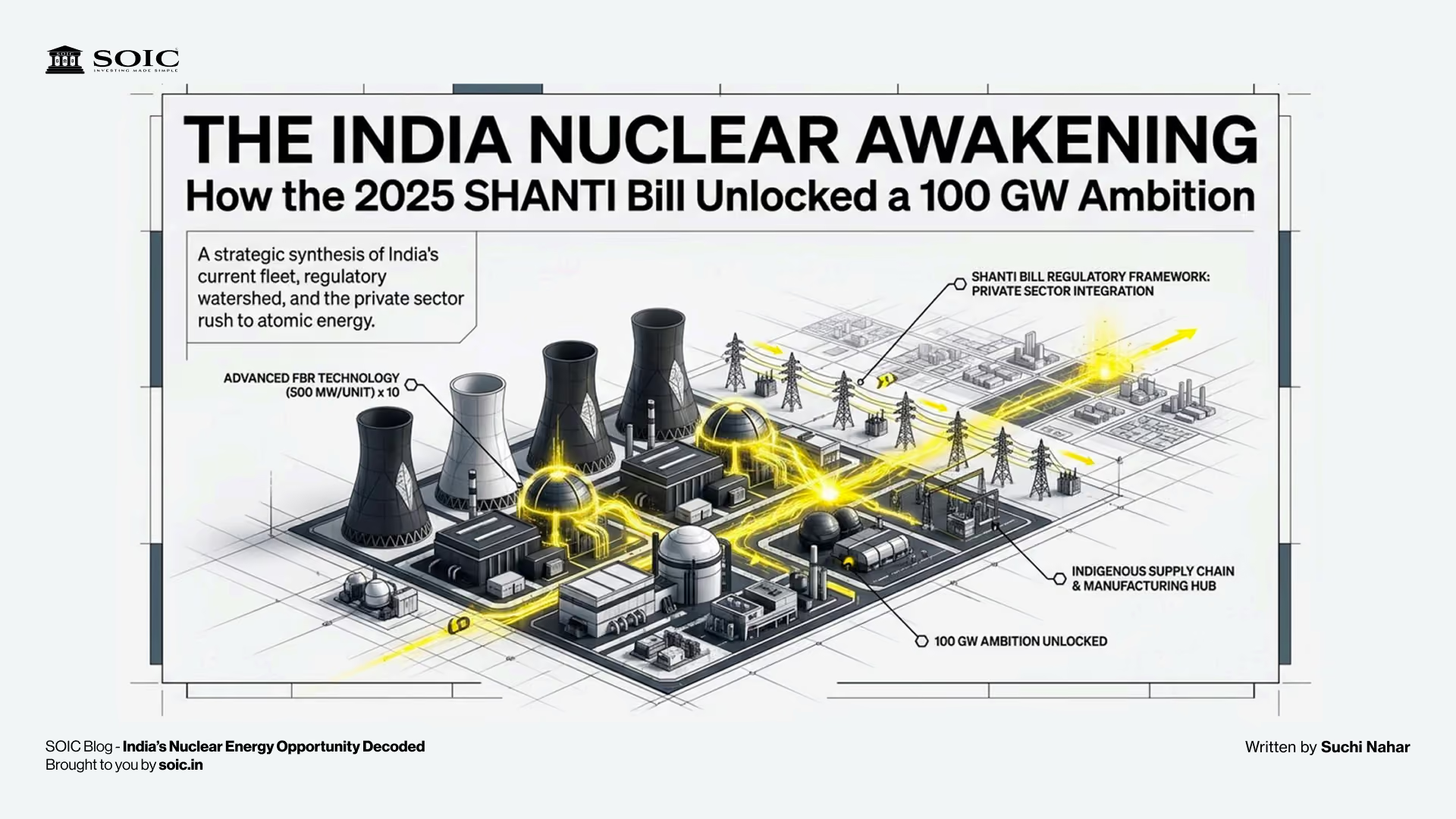

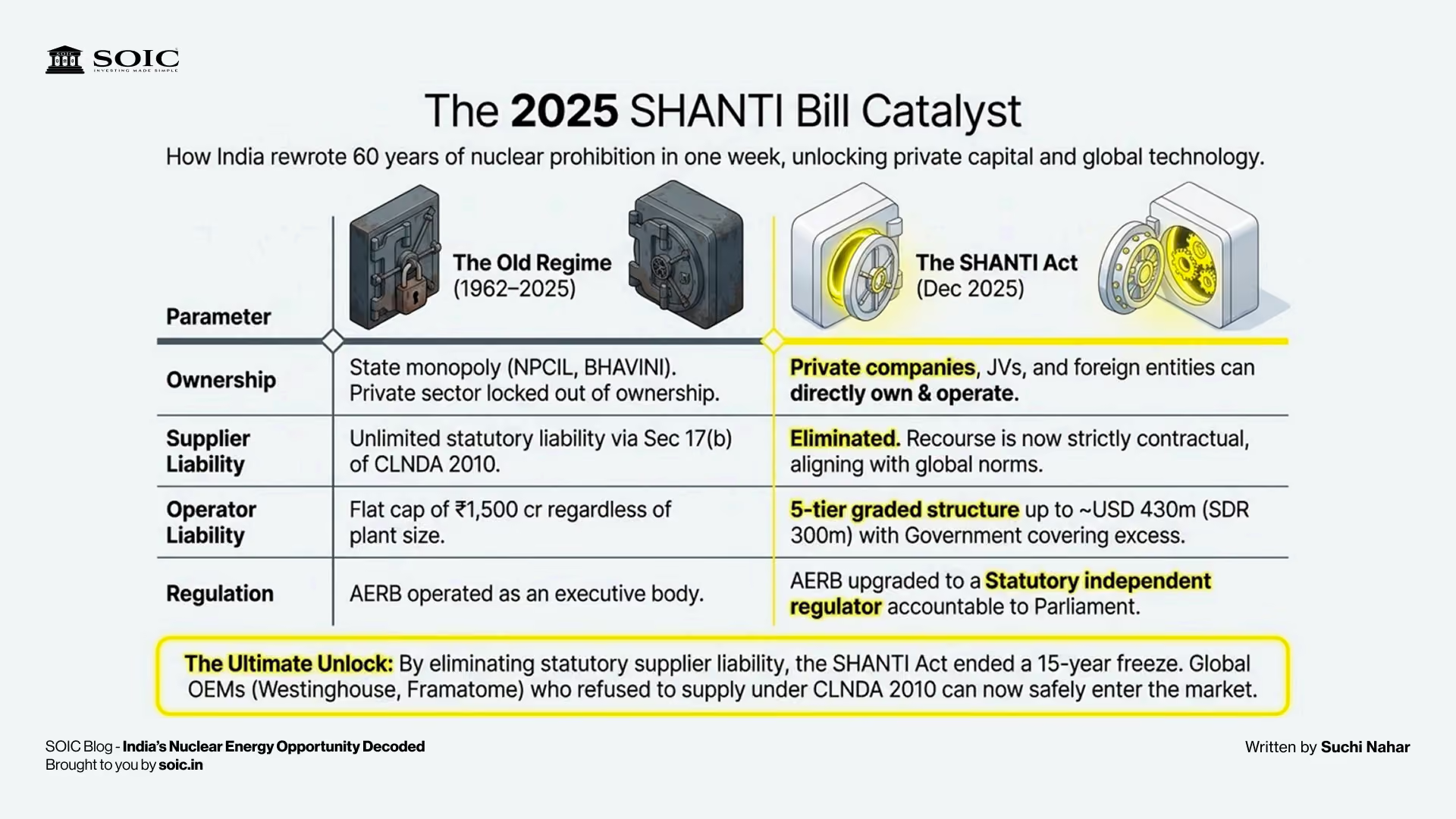

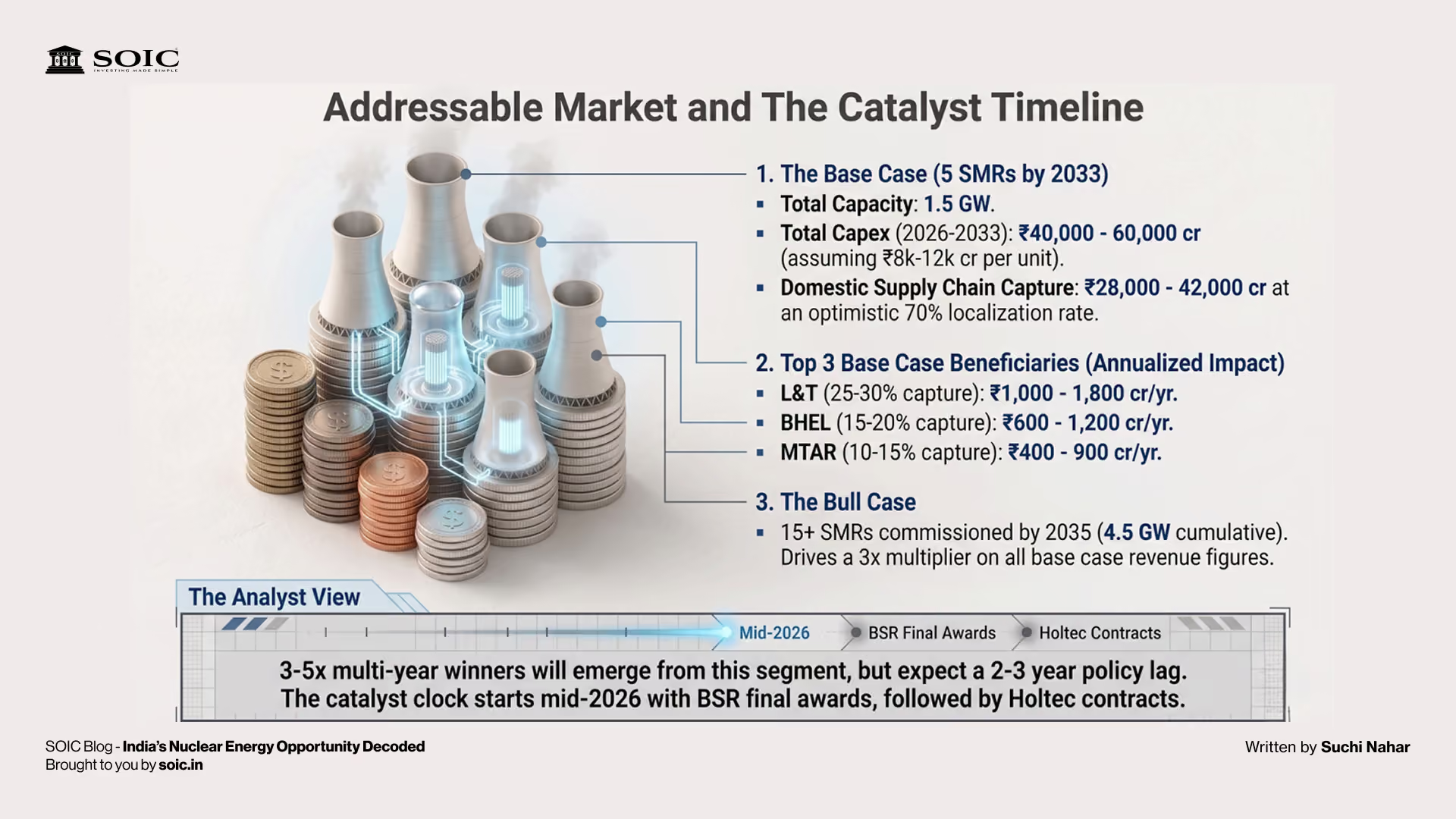

India’s nuclear sector has entered a structural re-rating phase as regulation shifts from being a constraint to a growth enabler. The SHANTI Act, 2025 replaces legacy laws and creates a modern framework aligned with the national objective of scaling capacity from 8.8 GW to 100 GW by 2047.

Most importantly, the Act permits regulated private participation in plant ownership, operations, equipment manufacturing, and selected fuel-cycle activities. This ends a six-decade state-dominated model and creates a parallel capex engine beyond NPCIL-led expansion. At an estimated capex intensity of INR 20–30 Cr/MW, the incremental buildout implies an INR 18–27 lakh Cr long-duration opportunity across generation and supply chains.

India currently operates around 8.8 GW of nuclear capacity, but the long-term ambition is far larger.

This is not a small expansion.

This is a potential multi-decade industrial buildout.

More importantly, recent policy changes are becoming increasingly supportive.

The SHANTI Act 2025 could become a turning point because it opens the door for greater private participation, revised liability structures and a broader nuclear ecosystem.

Historically, India’s nuclear sector remained highly state controlled.

Now the structure appears to be slowly evolving from:

“strategic restriction” towards “strategic expansion.”

That shift matters enormously for capital markets.

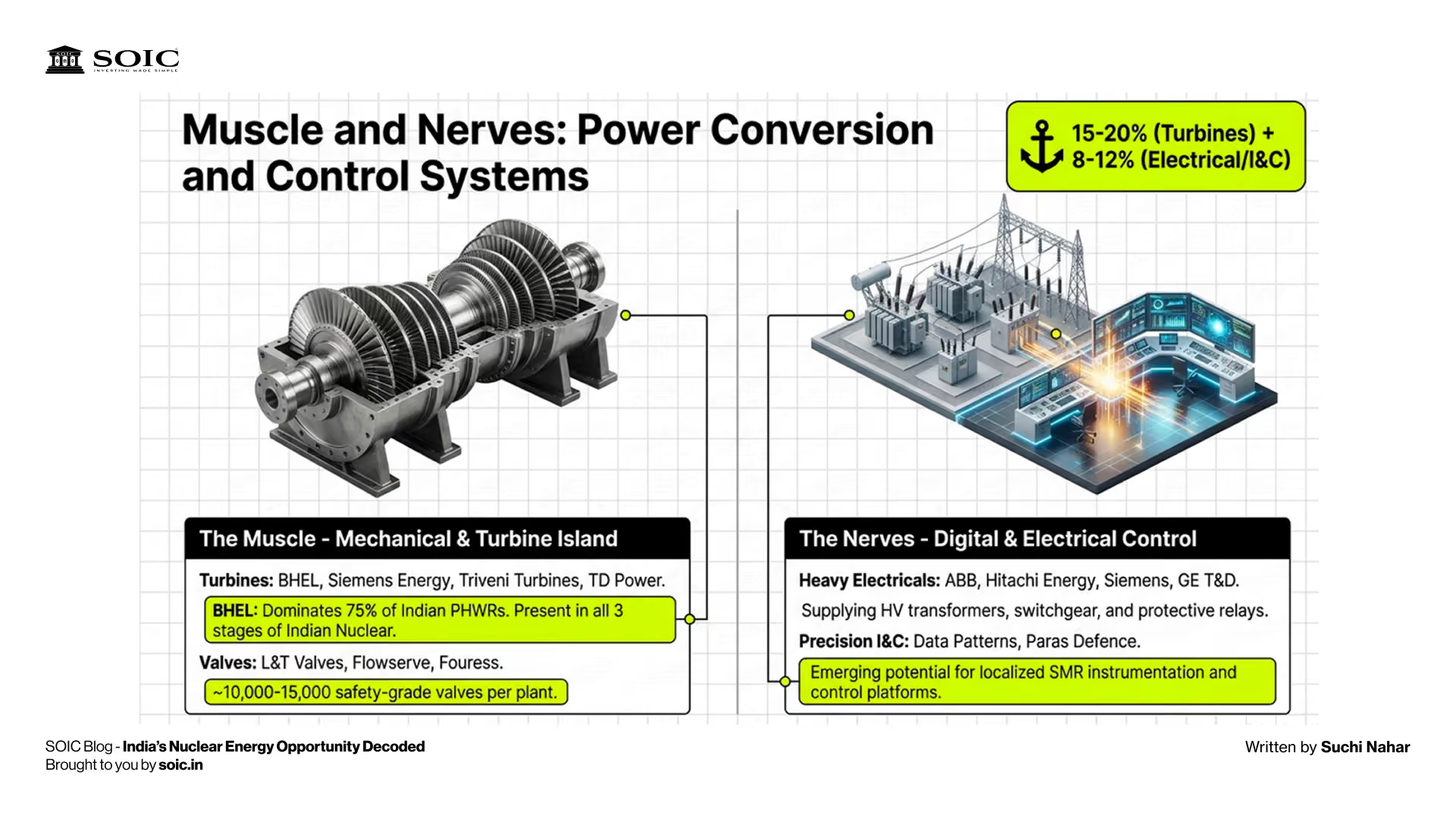

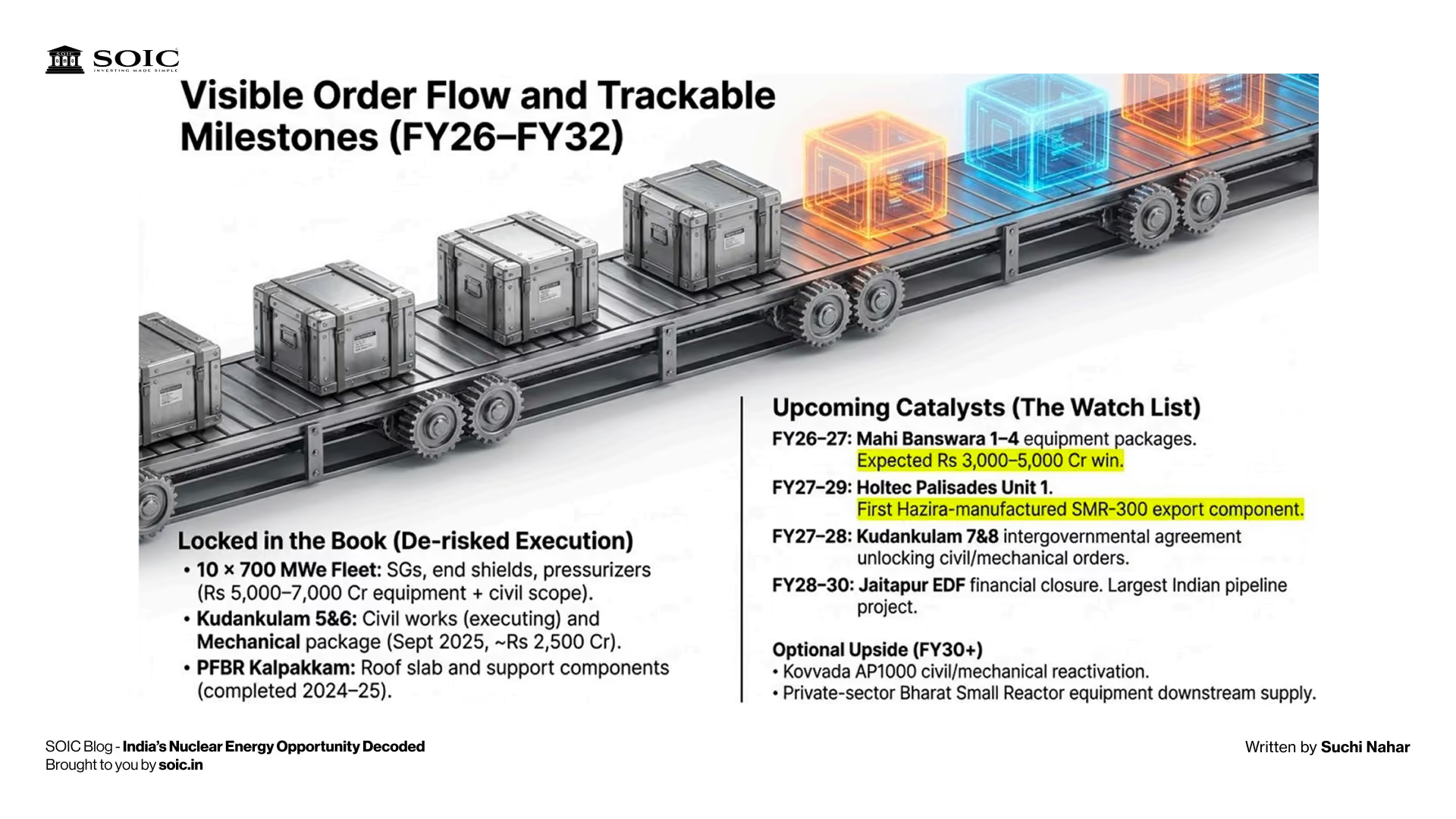

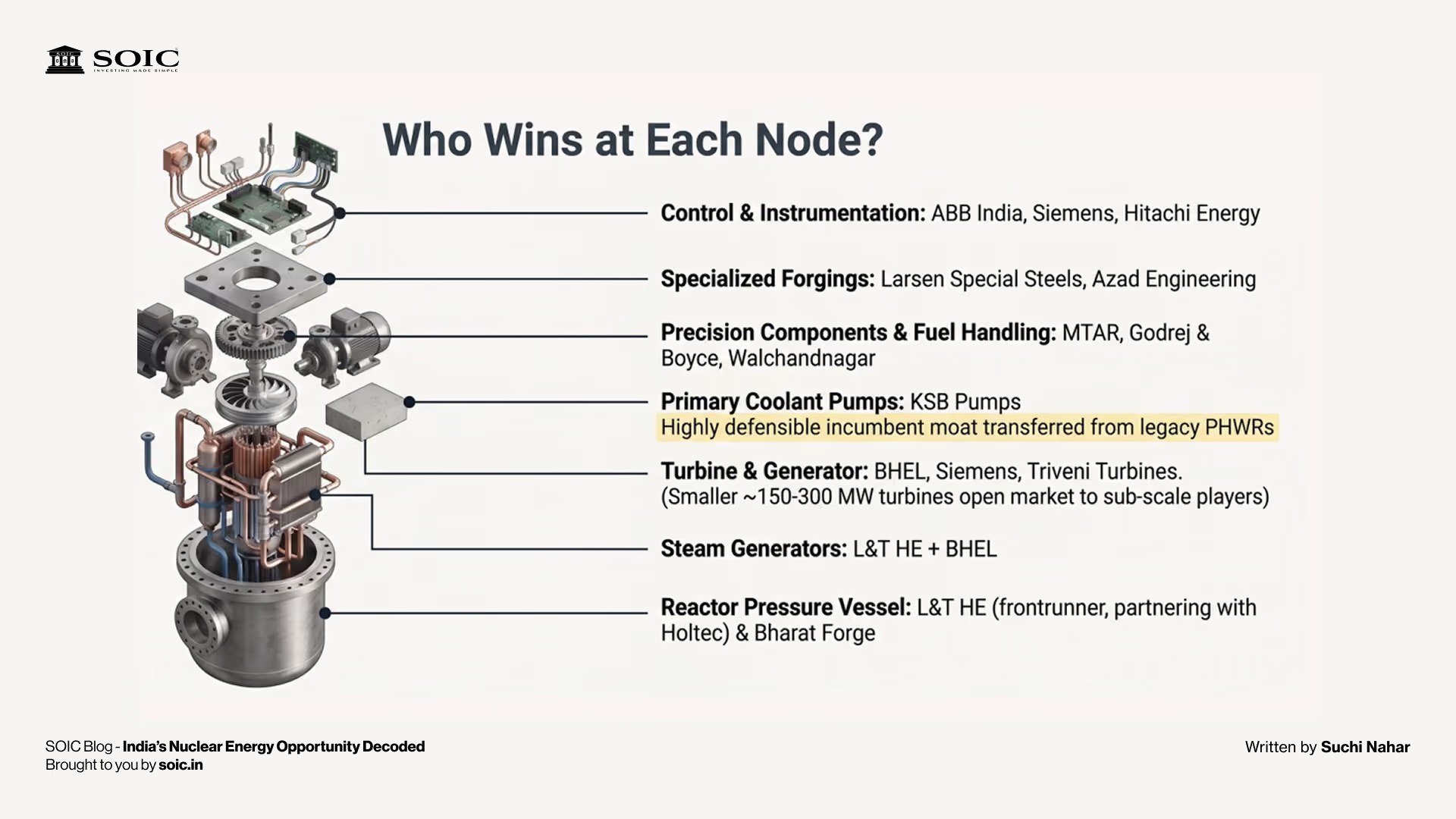

Larsen & Toubro (L&T): L&T is likely to be one of the biggest beneficiaries of India’s nuclear expansion due to its strong capabilities in reactor equipment, heavy forgings, pressure vessels and nuclear EPC execution. Its long-standing relationship with NPCIL and high entry barriers make it a key player in the ecosystem.

Adani Power: As of today, Adani Power has incorporated 3 companies, Namely (i) Adani Atomic Energy Limited (AAEL) their first nuclear subsidiary (ii) Coastal Maha Atomic Energy Ltd, a step down subsidiary targeting SMRs (iii) Rawatbhata Raj Atomic Energy Ltd, a step down subsidiary mainly focused on Rajasthan. Adani Power Limited has also announced that their long term plan is to replace the 18 GW thermal fleet with 30 GW Nuclear

BHEL: BHEL is the sole domestic manufacturer of nuclear steam turbine-generator (TG) sets for Pressurised Heavy Water Reactors (PHWRs). For every 700 MW PHWR, BHEL supplies a turbine-generator set worth approximately INR 800–1,200 crore. With 18– 20 new PHWRs planned under fleet mode + MBRAPP + future NTPC units, BHEL's potential nuclear order pipeline is INR 15,000– 25,000 crore over the next decade.

Nuclear projects carry inherent execution delays due to complex approvals and multi-agency coordination with Nuclear Power Corporation of India Limited and Atomic Energy Regulatory Board. For Bharat Heavy Electricals Limited, any delay in project milestones directly defers revenue recognition, while also stretching working capital cycles and pressuring margins, despite a healthy order book

Kirloskar Brothers (KBL): KBL is the only Indian company, and one of only four globally, capable of manufacturing advanced nuclear-grade sodium pumps for Fast Breeder Reactors. India's Stage 2 nuclear programme is based entirely on Fast Breeder Reactors, converting thorium to fissile material for India's Stage 3 (thorium) programme. KBL's sodium pump expertise gives it a unique, irreplaceable role in India's long-term nuclear future.

MTAR Technologies: MTAR is the most directly nuclear-exposed precision engineering company, with NPCIL as a direct, named customer and revenue already flowing from nuclear contracts. MTAR's components operate inside the active reactor zone where tolerances of 5–10 microns are required and radioactive environments demand special materials and coatings.

Only a handful of global companies can manufacture to these specifications. MTAR received a INR 310 crore order for Kaiga 5 & 6 real, confirmed nuclear revenue, not just positioning. As fleet mode expands to 10+ reactors, MTAR's nuclear order book could 3–5x from current levels.

Walchandnagar Industries: Walchandnagar is India's most specialized nuclear reactor equipment manufacturer among listed companies; it makes the actual core components inside the reactor itself, not peripheral equipment. WIL supplied critical equipment for India's Prototype Fast Breeder Reactor (PFBR) at Kalpakkam, which achieved criticality on 6th April, 2026. Management has explicitly stated "eyeing growth in the nuclear sector after SHANTI Act approval," targeting new orders from MBRAPP, fleet mode reactors, and future NTPC/NPCIL projects.

Hindustan Construction Company (HCC): HCC has built more nuclear power capacity than any other company in India's history — including both private and public entities. HCC has explicitly announced plans to expand from PHWRs into Light Water Reactors (LWRs) — which will be the dominant technology for India's large imported reactor fleet (EDF EPRs, Westinghouse AP-1000s, VVER-1200s).

This is a major strategic expansion of its nuclear addressable market. HCC remains constrained by elevated leverage and working capital intensity, limiting near-term balance sheet improvement despite nuclear inflows. Execution risk is higher with LWR projects, given the added technical complexity and certification needs, increasing the probability of delays or cost overruns. Moreover, growth visibility is contingent on timely contract awards from Nuclear Power Corporation of India Limited and NTPC Limited, making revenues inherently lumpy.

KSB Limited: KSB supplies industrial pumps and valves used in critical cooling and safety systems within nuclear plants, giving it niche exposure to the sector.

NTPC: India's National Nuclear Energy Mission has set a target to scale nuclear power from ~8.8 GW today to 100 GW by 2047, a 10x expansion in roughly 20 years.

NPCIL: NPCIL remains the backbone of India’s nuclear programme and will continue driving reactor development, execution and ecosystem growth.

Azad Engineering: Azad Engineering is India's premier precision component manufacturer for mission-critical applications, supplying high-tolerance rotating and stationary parts for gas, nuclear, and thermal turbines globally. Nuclear turbines (supplied by BHEL, GE Vernova, Siemens) require precision-forged blades and vanes that must survive extreme temperatures, pressures, and radiation environments.

Azad makes these components for global OEMs who then supply nuclear plants worldwide, including India. Azad benefits from nuclear indirectly but significantly, as nuclear plant orders flow to GE Vernova and Siemens Energy, Azad's component orders from these OEMs increase proportionally.

Electronics & Control System Players: Companies involved in instrumentation, automation and digital control systems could also benefit as nuclear plants increasingly become technology-intensive engineering systems.

This is where the story becomes truly interesting from an investing perspective. Most people hear “nuclear theme” and immediately think of utilities. But nuclear power plants are not simple projects.

They are among the most complex engineering systems humanity builds.

A nuclear reactor requires:

And unlike many manufacturing industries, nuclear supply chains operate under extremely strict qualification standards.

Vendor approvals can take years.

Failure tolerance is almost zero.

This naturally creates oligopolies.

Nuclear is not merely an energy business — it is an engineering ecosystem dominated by highly specialized players with deep technological barriers. That changes the quality of opportunity.

Because once a company becomes qualified in such ecosystems, replacement becomes difficult. And difficult-to-replace businesses are often where long-term wealth creation happens.

Markets often underestimate the power of long-duration capex themes.

Railways.

Transmission.

Defence.

Power equipment.

All these themes eventually became larger than initial expectations because they were not one-year stories.

They were decade-long cycles.

Nuclear could evolve similarly.

India’s nuclear buildout opportunity could translate into massive capital expenditure across utilities, EPC players, heavy engineering companies, and specialised manufacturers.

And unlike many cyclical sectors, nuclear projects usually involve:

This combination can create unusually durable order books for capable players.

It is important to remain balanced.

Nuclear energy still carries significant challenges:

Even globally, nuclear projects have often suffered from cost overruns and execution delays.

This is not an easy sector.

And that is precisely why entry barriers remain high.

The opportunity exists because the difficulty exists.

The world may have spent the last twenty years debating whether nuclear energy belongs in the future. But the next twenty years may be spent figuring out how much nuclear energy the future actually needs.

Because beneath all the narratives, the modern economy runs on one invisible force:

Reliable electricity.

And as AI, electrification, industrialisation, and energy security become national priorities, the demand for stable clean power may rise dramatically.

India’s nuclear journey is still at an early stage.

But for the first time in decades, policy support, geopolitical necessity, technology demand and industrial capability appear to be moving in the same direction.

Nuclear energy may or may not become India’s dominant power source.

But one thing is becoming increasingly clear:

But sometimes, the biggest investment themes are born exactly where complexity is the highest and participation is the lowest.

The world’s future economy will need enormous amounts of reliable electricity.

And if India truly moves from 8 GW to 100 GW over the next two decades, this may not remain just an energy story.

It could become one of the biggest industrial, engineering, and manufacturing opportunities of the next generation.

Disclaimer: The information provided is for educational purposes only and should not be considered investment advice. We are SEBI-registered research analysts.

We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

%20(1).avif)

0 Comments